TL;DR

- Collections propensity models without MLOps drift monitoring lose 12-18 Gini points within 18 months: the degradation is silent until an examination or unexplained recovery rate decline

- RBI MRM 2024 requires ongoing monitoring that is operationally continuous: examination-assembled performance reports are not a compliant substitute

- Automated retraining pipelines must include champion-challenger comparison, change control documentation, and governance approval before any retrained model replaces the production champion

- RBI examination readiness in MLOps means documentation is current within days of the examination date: not weeks of assembly effort after the notice arrives

- iTuring auto-generates RBI MRM documentation per retraining cycle: drift alerts, change control records, and board-ready monitoring reports updated continuously from deployment

A ₹7,200 crore NBFC deployed its AI collections model 14 months ago. The Gini has drifted from 0.74 to 0.61. No drift monitoring system was running. No retraining was triggered. No RBI MRM documentation was updated. The next examination is in 6 weeks. This scenario captures the core operational risk facing MLOps for Indian bank and NBFC collections models: without continuous governance infrastructure, RBI MRM compliance becomes a retrospective scramble rather than a standing operational state, and recovery rates silently erode while the model inventory shows a stale validation date. This article provides a concrete framework for building governed retraining pipelines for collections AI models, covering drift thresholds, champion-challenger protocols, documentation automation, and examination readiness. After reading, a Head of Data Science at an NBFC or private bank will have a step-by-step governance pipeline that satisfies RBI MRM 2024 requirements for ongoing model monitoring and change control. iTuring addresses this through platform-native model governance with immutable audit trail and maker-checker approval.

Why Model Deployment Is Not Model Governance: And Why That Distinction Costs NBFCs at Examination

For a Head of Data Science at an NBFC or private bank, maintaining RBI MRM-compliant model governance for continuously retraining AI collections models in production means running a daily operational cycle: monitoring input feature distributions against deployment-day baselines, tracking Gini and KS statistics on live portfolios, triggering retraining when thresholds breach, documenting every change control event, and keeping the model inventory current without manual intervention. What breaks down is not the model itself but the infrastructure around it. The data science team sees stale PSI reports, undocumented retraining events, and a model card that was last updated at the initial validation. Model drift monitoring for NBFC collections under RBI requirements is not a quarterly exercise; it is a daily operational obligation that most teams lack the tooling to sustain.

The gap persists because most NBFC data science teams build retraining pipelines as batch jobs triggered by calendar schedules, not by statistical thresholds. A quarterly retraining cadence assumes portfolio composition remains stable for 90 days. In practice, NBFC collections portfolios shift continuously: new product launches change borrower demographics, seasonal payment behavior alters cure rates, and regulatory policy changes (such as the recalibration of NBFC regulation tiers) reshape risk segmentation. A calendar-based pipeline cannot detect a mid-quarter distribution shift. It simply waits for the next scheduled run.

The average collections propensity model deployed without MLOps drift monitoring shows a 12-18 point Gini reduction within 18 months due to portfolio composition drift (iTuring Model Performance Benchmark: 18 NBFC deployments, 2023-2025). That degradation translates directly into misallocated collection agent capacity, higher cost per recovery, and lower portfolio-level recovery rates. For an NBFC with ₹5,000 crore in delinquent book, even a 5-point Gini decline can redirect thousands of agent hours toward accounts with low payment propensity. The table later in this article shows where NBFCs and private banks teams currently stand on each dimension.

What Happens to NBFC Collections AI Model Performance Without MLOps Monitoring After 18 Months

Standard rule-based diallers and static bucket workflows do one thing well: they enforce a structured contact sequence across DPD bands. A 30-60-90 bucket strategy ensures every delinquent account receives some form of outreach at defined intervals. The design scope of these tools is contact execution, not model performance management. They were built to schedule calls and track dispositions, not to monitor whether the underlying propensity scores feeding the queue are still statistically valid. The specific failure mode is silent: the dialler continues to operate, the queue populates on schedule, and the contact logs look normal. No component in a static bucket workflow measures whether the model’s rank-ordering accuracy has degraded. There is no PSI alert, no Gini tracking, and no mechanism to flag that the model’s output distribution has shifted from its deployment-day baseline.

The gap compounds most visibly in cost per contact escalation. When a collections propensity model loses rank-ordering accuracy, low-propensity accounts rise in the queue while high-propensity accounts fall. Agent hours shift toward borrowers who were unlikely to pay regardless of contact, while self-cure candidates receive unnecessary outreach. One NBFC observed a 35% increase in cost per recovery over 12 months with no change in agent headcount or dialler configuration: the only variable was model degradation. RBI’s draft guidelines for managing model risks in credit specifically require documented ongoing monitoring precisely because this type of silent degradation creates both financial and regulatory exposure. The gap is a design scope problem: NBFCs and private banks need a tool built specifically for this layer of continuous model governance, not a contact execution system repurposed for model monitoring.

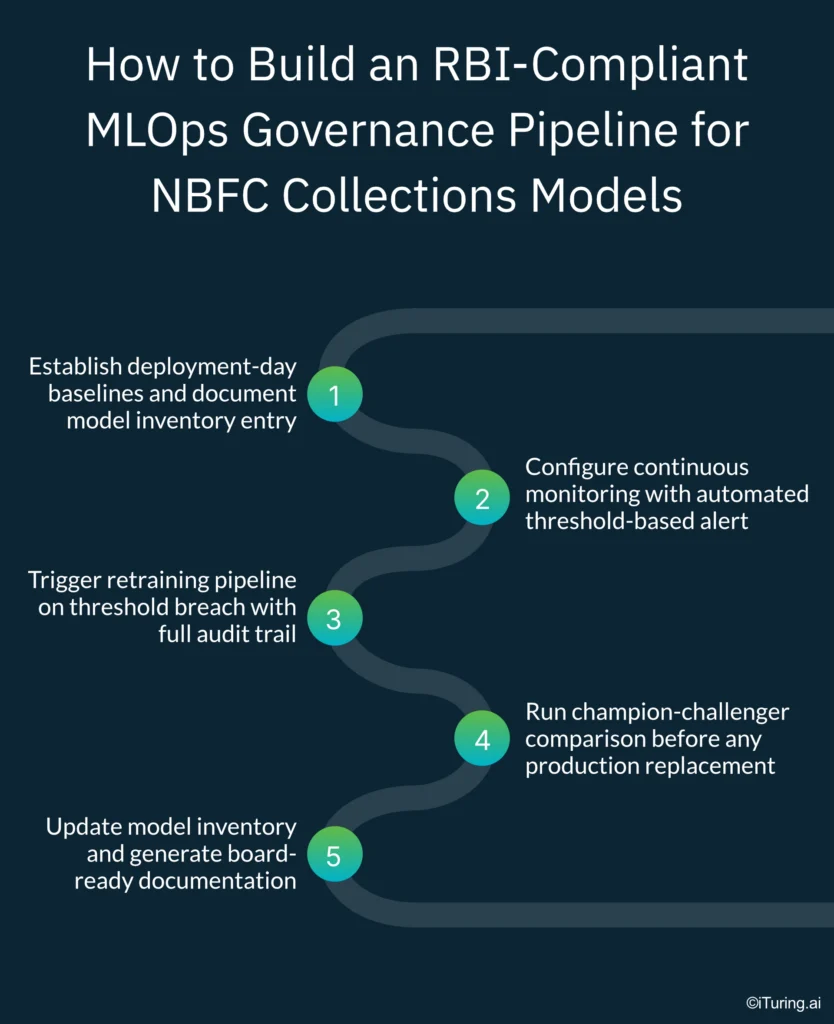

How to Build an RBI-Compliant MLOps Governance Pipeline for NBFC Collections Models

Step 1: Establish deployment-day baselines and document model inventory entry. The iTuring platform captures the production model’s feature distributions, Gini coefficient, KS statistic, and PSI baseline at the moment of deployment. The NBFC data science team configures alert thresholds aligned to their board-approved MRM policy: typically PSI above 0.2 for feature drift and a defined Gini decline percentage. The output is a complete model inventory entry with versioned baseline statistics, forming the foundation of MLOps governance for NBFC collections models under RBI MRM requirements.

Step 2: Configure continuous monitoring with automated threshold-based alert. iTuring runs daily PSI and Gini calculations against the deployment-day baselines on live production data. The collections team receives structured alerts when any monitored metric breaches its configured threshold, with root cause attribution identifying which features or portfolio segments drove the shift. The output is a timestamped drift report that satisfies RBI’s requirement for operationally continuous monitoring, not retrospective quarterly reviews.

Step 3: Trigger retraining pipeline on threshold breach with full audit trail. When a drift alert fires, iTuring’s retraining pipeline initiates automatically: pulling updated training data, engineering features from the 50,000 pre-built financial signals in the Data Accelerator, and training a candidate model. Model drift monitoring for NBFC collections under RBI compliance requires that every retraining trigger be logged with the specific metric breach, timestamp, and root cause analysis. The output is a candidate model with documented provenance.

Step 4: Run champion-challenger comparison before any production replacement. The candidate model runs alongside the incumbent champion on a defined production sample, comparing payment outcome predictions against actual results. iTuring auto-generates the comparison report with pre- and post-Gini statistics, feature importance shifts, and segment-level performance breakdowns. The NBFC governance committee reviews this report before any deployment decision, and the change control record documents the approval with maker-checker sign-off.

Step 5: Update model inventory and generate board-ready documentation. Upon governance approval, iTuring deploys the new champion, updates the model inventory entry with the new baseline statistics, and generates the updated model card, monitoring report, and board-ready evidence pack. The entire retraining event is logged with an immutable audit trail. The point where NBFCs and private banks teams most often expect friction: maintaining RBI MRM-compliant model governance for continuously retraining AI collections models in production: is precisely where this sequence prevents it.

How iTuring’s MLOps Layer Maintains Collections Model Performance and RBI MRM Compliance Simultaneously

Continuous PSI and Gini drift monitoring against deployment-day baselines: alert triggers on threshold breach with root cause analysis; no manual monitoring run required

Consider a mid-size NBFC with a ₹3,500 crore retail lending book that launches a new personal loan product in Q2. Within six weeks, the borrower demographic feeding the collections model shifts: younger borrowers, shorter credit histories, different payment channel preferences. iTuring’s monitoring engine detects the PSI breach on three input features before the Gini itself declines, because feature distribution shifts precede outcome degradation. The collections team receives an alert specifying which features shifted, by how much, and which portfolio segment drove the change. No analyst needed to run a manual monitoring notebook. The alert includes a root cause attribution that maps directly to the new product cohort entering the delinquent book.

Champion-challenger retraining pipeline: new model candidate trained and compared against incumbent before deployment; change control record auto-generated with pre- and post-Gini comparison

The retraining mechanism operates as a closed loop. When a drift alert triggers retraining, iTuring trains the candidate model on updated data, then deploys it on a holdout production sample alongside the champion. The comparison runs for a defined observation window: typically one to two billing cycles for collections models: measuring actual payment outcomes against predicted propensity scores. The change control record auto-generates with the comparison metrics, approval workflow status, and deployment decision rationale. For NBFCs operating under RBI MRM 2024, this satisfies the requirement that model risk management includes documented change control for every retraining event. The operational outcome: no retrained model enters production without a documented, approved comparison against the incumbent. MLOps governance for NBFC collections models under RBI MRM depends on this chain of evidence being unbroken.

Model drift in collections AI is silent. The scores still come out. The queue still populates. Recovery rates decline slowly. No alarm fires. Only the examination, 14 months later, shows what happened.

RBI MRM documentation auto-update per retraining cycle: model card, monitoring report, and board-ready evidence pack updated automatically; examination export compiles in 30 minutes

Each retraining cycle closes with an automatic documentation update. The model card reflects the new champion’s feature set, training data vintage, and performance statistics. The monitoring report appends the drift event, root cause analysis, retraining decision, and champion-challenger comparison. The board-ready evidence pack compiles all events since the last board reporting date into a structured summary. When an RBI examination notice arrives, the NBFC exports the complete governance package: model inventory, all monitoring reports, change control records, and board reports: in under 30 minutes. RBI’s FREE AI framework for ethical AI governance emphasizes accountability and transparency in AI systems used by financial institutions. This documentation chain satisfies that requirement without a 12-week manual assembly effort.

Automated Model Governance vs Manual NBFC MLOps: What RBI Examiners Actually See

Teams evaluating governance approaches for continuously retraining collections AI models have real choices. Standard tools serve teams with straightforward contact-automation requirements where model governance is handled through separate manual processes. This comparison is for teams whose scope includes maintaining RBI MRM-compliant model governance for production collections models with continuous retraining: the operational layer where MLOps for NBFC collections models intersects with RBI MRM compliance. The table below compares the criteria that matter most for NBFCs and private banks.

| Criterion | Standard Tools | iTuring |

| Account prioritisation | DPD bucket order | Daily propensity score: 25,000+ signals |

| Self-cure identification | Not available | Withholds self-cure accounts before queue loads |

| Contact timing | Fixed campaign schedule | Per-account optimal timing from behavioral signals |

| Model retraining | Quarterly or ad hoc | Continuous: outcomes retrain model automatically |

| Audit trail (RBI) | Contact logs only | Immutable per-account decision log: examination-ready |

If your NBFC is deploying collections AI for the first time with a portfolio under Rs. 500 crore, a lighter governance framework may satisfy RBI Base Layer requirements: Upper Layer obligations are more demanding.

From 12-Week Documentation Sprint to 30-Minute Examination Export: A Governance Comparison

A leading NBFC in India with a ₹9,000 crore retail lending book faced a specific governance gap: its collections AI model had been retrained three times over 18 months, but no change control records existed, the model card reflected the original deployment, and the board had received no monitoring reports since initial validation. The institution deployed iTuring’s MLOps layer with iTuring Model Risk and iTuring ML Governance, completing integration within four weeks and establishing continuous monitoring from the first production day.

Results after deployment:

- 20% increase in collections recovery rate

- 43% reduction in cost per recovery

Model Governance Is Not a Deployment Activity: It Is an Operations Activity That Starts on Day One

Drift monitoring thresholds must be defined in your board-approved MRM policy before deployment, not configured retroactively after the first examination finding. The retraining pipeline is only half the governance obligation: the other half is the change control documentation chain that proves every production model replacement was tested, compared, approved, and logged. RBI’s new guidance on operational risk management and the evolving lending trends for banks and NBFCs both point toward the same operational reality: model governance is a continuous production obligation, not a periodic validation exercise.

iTuring’s MLOps layer monitors your collections model continuously from day one and generates RBI documentation automatically: test it against your current model governance setup before any licence decision.