TL;DR

- SHAP explainability for RBI examinations means per-account reasoning on demand

- Not portfolio-level feature importance that cannot answer account-specific questions

- The RBI 2024 MRM framework requires account-level explanations to be available on demand

- Not compiled retrospectively after an examination notice arrives

- 61% of NBFC collections model examination findings in FY2024-25 cited inadequate account-level explainability as a contributing or primary factor

- Post-hoc SHAP layers on black-box models face closer examiner scrutiny than native explainability

- iTuring generates SHAP waterfall charts per account on demand. Full examination export compiles in 30 minutes

An RBI examiner asks for the reasoning behind account 847291’s propensity score during a model validation review. The NBFC’s collections head pulls up the dashboard. It shows a 0.73 score. There is no per-account explanation available, only a portfolio-level feature importance chart. This gap in SHAP explainability for RBI collections model examinations carries a specific operational consequence for NBFCs: the inability to produce account-level reasoning on demand triggers a supervisory observation, which escalates to a formal finding, which then requires board-level remediation with a defined timeline, all while the collections model may face operational restrictions during the remediation window. This article provides a step-by-step framework for building examination-ready, account-level SHAP explanations within NBFC collections AI, equipping Heads of Model Risk to produce per-account reasoning within the same session an examiner requests it. iTuring addresses this through platform-native model governance with immutable audit trail and maker-checker approval.

Why RBI Examiners Ask for Account 847291, Not the Portfolio Gini

For a Head of Model Risk at an NBFC, the inability to explain AI collections decisions at account level on demand is not an abstract compliance concern. It is the moment during an on-site examination when a supervisor selects a specific delinquent account, asks why the model assigned that propensity score, and the collections team can only produce a bar chart showing that “days past due” and “loan balance” are the top two features across the entire portfolio. The examiner does not want to know what matters in general. The examiner wants to know what drove this score for this borrower. Model explainability in an RBI NBFC examination context means answering that specific question, for any account, within the session.

The gap persists because most NBFC collections AI implementations store model outputs (the score) but not the explanation path that produced the score. The propensity model runs in a production pipeline that writes a float value to the collections queue. SHAP values, if computed at all, are generated during model development for validation reports and then discarded. No infrastructure exists to compute, store, and retrieve per-account SHAP decompositions in production. The workflow was designed to serve the collections dialler, not the examination room, and the data pipeline reflects that priority.

This design gap carries measurable cost. Of NBFC AI collections model examination findings in FY2024-25, 61% cited inadequate account-level explainability as a contributing or primary factor (RBI Supervisory Findings Summary FY2024-25). RBI has explicitly asked banks and NBFCs to assess AI risk gaps and draw up action plans, signalling that explainability is no longer a best-practice aspiration but a supervisory expectation with enforcement consequences. The examination cost is not limited to the finding itself: remediation timelines, board risk committee reporting, and potential operational restrictions on the model compound the impact. The table later in this article shows where NBFC teams currently stand on each dimension.

Why Portfolio-Level Model Documentation Fails Account-Level Examination Questions

Standard collections scoring models and legacy rule-based systems were built to rank-order accounts for outbound contact. They do this competently. A static scorecard assigns risk bands, a DPD-bucket workflow determines queue priority, and campaign schedules dictate contact timing. These tools were designed for operational throughput: move accounts through a contact funnel efficiently. They were not designed to produce a per-account audit trail explaining why a specific borrower received a specific treatment. The failure mode is not inaccuracy; it is absence. When an NBFC using static bucket workflows receives an examination request for account-level model reasoning, the system has no explanation to retrieve because it never generated one. The NBFC sector’s growing reliance on AI-driven collections makes this design limitation increasingly visible to supervisors.

The gap compounds at the documentation layer. Without per-account SHAP values stored in production, the model risk team must reconstruct explanations manually: pulling raw feature data, re-running SHAP computations offline, and translating outputs into examiner-readable format. This process takes days, sometimes weeks, for a single account. During an on-site examination, that timeline is unacceptable. The RBI directive requiring institutions to assess AI risk gaps and draw action plans by mid-2026 makes the urgency concrete. The gap is a design scope problem: an NBFC’s inability to explain AI collections decisions to RBI examiners at account level on demand requires a tool built specifically for this layer.

How to Produce Account-Level SHAP Explanations for an RBI Collections Model Examination

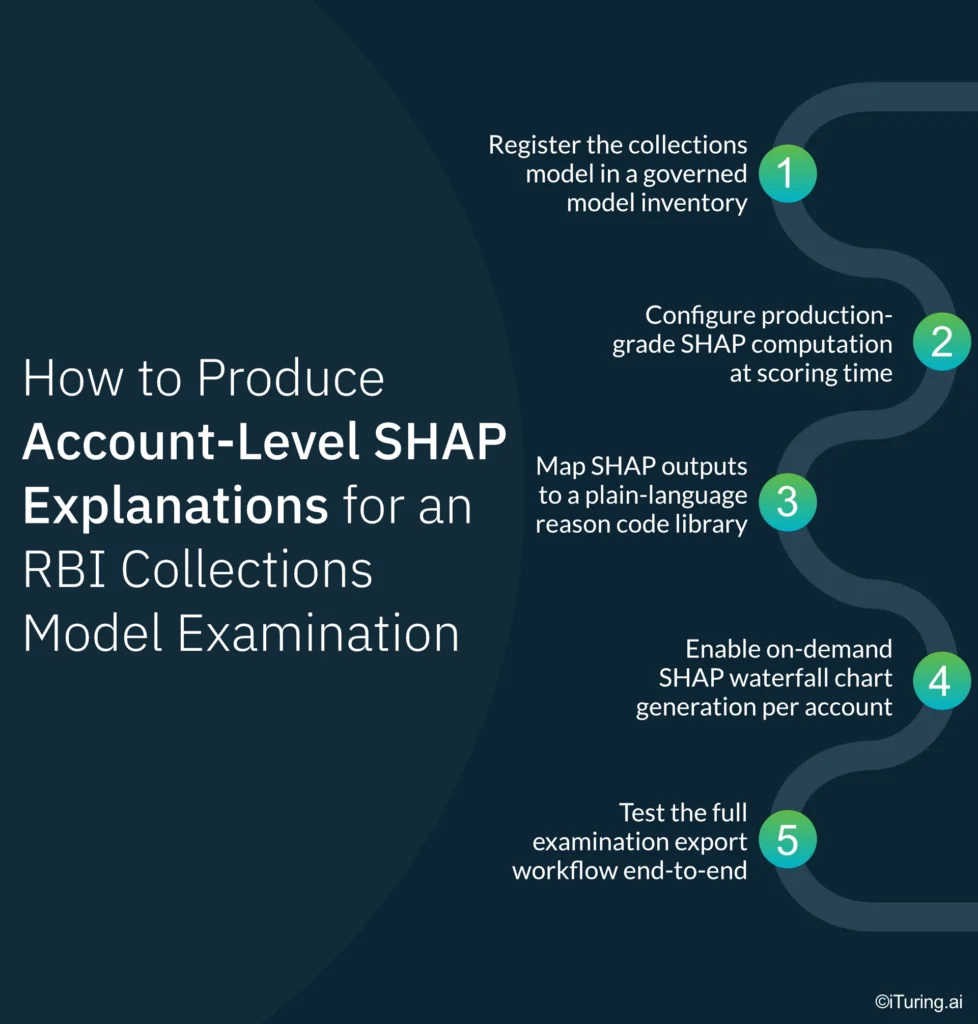

Step 1: Register the collections model in a governed model inventory with SHAP computation enabled

The NBFC’s model risk team registers the collections propensity model within iTuring ML Governance, specifying the model type, feature set, and SHAP computation parameters. SHAP explainability for RBI collections model NBFC examinations requires that the inventory entry links the production model version to its SHAP configuration, ensuring every score generated in production has a corresponding explanation path. The output is a governed model card with version control, approval lineage, and SHAP computation settings locked under maker-checker approval.

Step 2: Configure production-grade SHAP computation at scoring time

iTuring AutoML+ computes SHAP values for every account at the moment of scoring, not as a batch job after the fact. The NBFC team configures the scoring pipeline to write both the propensity score and the full SHAP decomposition to an immutable decision log. The output per account includes the base value, each feature’s SHAP contribution with sign and magnitude, and the final prediction, all timestamped and stored with data lineage.

Step 3: Map SHAP outputs to a plain-language reason code library

The model risk team configures a reason code library that translates raw SHAP feature names into business-language explanations an examiner can verify without data science expertise. For example, “feature_dpd_30_count” maps to “Number of times account exceeded 30 days past due in the last 12 months.” This mapping supports model explainability in RBI NBFC examination settings by ensuring the examiner reads a coherent narrative, not a list of variable names. iTuring’s reason code framework enforces consistency across all accounts and model versions.

Step 4: Enable on-demand SHAP waterfall chart generation per account

The NBFC team activates iTuring’s examination export module, which generates a SHAP waterfall chart for any individual account on demand. The chart displays each feature’s contribution to the propensity score in descending order of magnitude, with positive contributions (increasing the score) and negative contributions (decreasing it) clearly distinguished. The output is a PDF or interactive visual that the collections head can pull up during an examination session without requiring a data scientist in the room.

Step 5: Test the full examination export workflow end-to-end

Before any examination cycle, the model risk team runs a simulated examination drill: select 10-15 accounts at random, request SHAP waterfall charts, verify reason code accuracy, and confirm the full export compiles within 30 minutes. iTuring’s examination export packages the waterfall chart, the reason code narrative, the decision log entry, and the model card into a single document per account. The drill validates that the infrastructure works under examination conditions, not just in development.

The point where NBFC teams most often expect friction, the inability to explain AI collections decisions to RBI examiners at account level on demand, is precisely where this sequence prevents it.

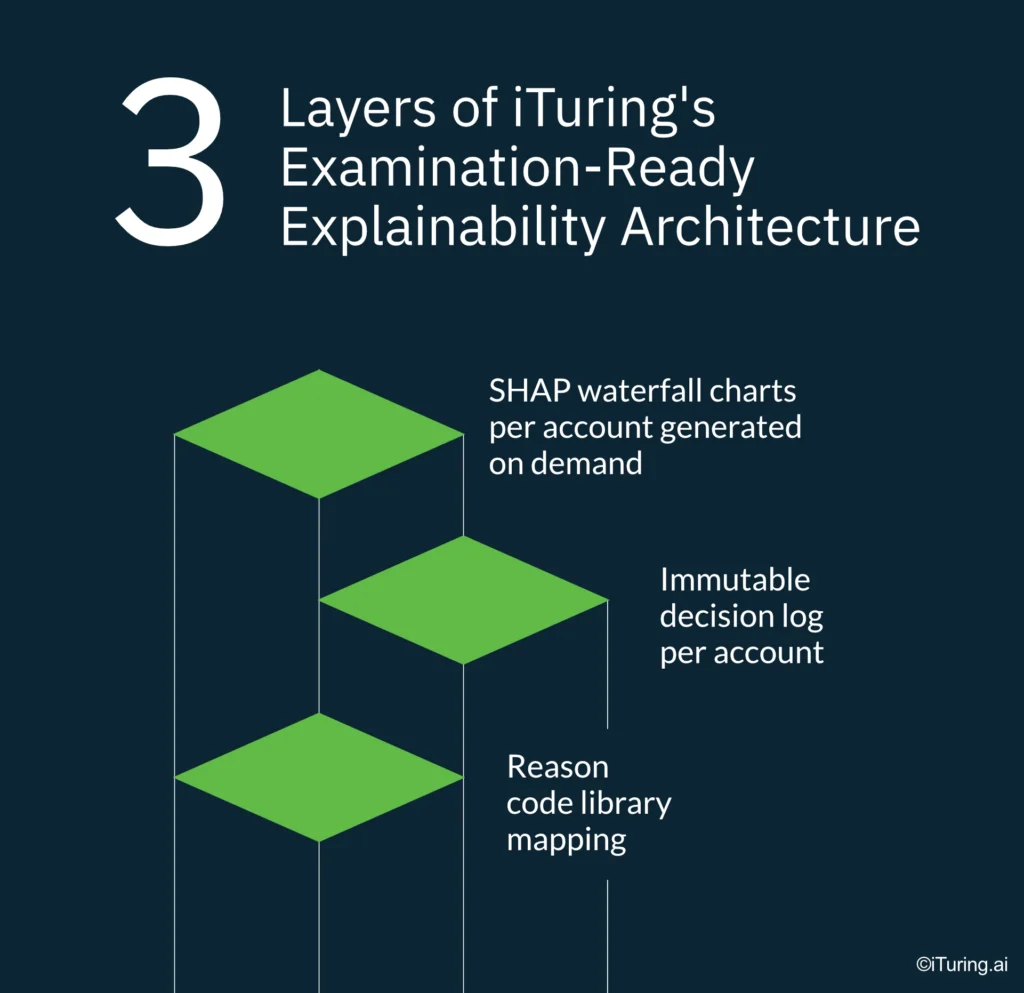

The Three Layers of iTuring’s Examination-Ready Explainability Architecture

SHAP waterfall charts per account generated on demand

Consider account 847291, a microfinance borrower with a 0.73 propensity score. The examiner requests the reasoning. The collections head opens the account in iTuring and generates the SHAP waterfall chart. The chart shows that three consecutive missed payment dates contributed +0.18 to the score, a recent partial payment contributed -0.09, the borrower’s geographic risk cluster contributed +0.07, and the remaining 14 features each contributed smaller increments. The chart renders in under 10 seconds. The full examination export, including the waterfall chart, reason codes, and decision log, compiles in under 30 minutes for any number of accounts requested during the session.

Immutable decision log per account

Every propensity score, treatment decision, and approval event logged with lineage and timestamp for full examination traceability

Every time the collections model scores an account, iTuring writes the score, the SHAP decomposition, the treatment decision (which contact strategy was assigned), and the approval event to an append-only log. No entry can be modified or deleted after creation. Each log entry carries a timestamp, the model version that produced it, and the data lineage tracing which features were computed from which source tables. For NBFCs, this means the examiner can trace any account’s score backward through the entire decision chain: from the contact strategy the borrower experienced, to the treatment assignment, to the SHAP explanation, to the raw feature values. SHAP explainability for RBI collections model NBFC audits depends on this traceability being continuous and tamper-proof.

A propensity model that explains its population-level drivers but cannot tell an examiner why account 847291 was scored 0.73 is not meeting the RBI 2024 MRM standard, regardless of its Gini coefficient.

Reason code library mapping

SHAP outputs to plain-language explanations verifiable by a non-technical examiner without data science expertise

The reason code library creates a governance feedback loop: when the model is retrained and new features enter the scoring pipeline, the library flags any unmapped features before the model version can be promoted to production. This prevents a scenario where a model scores accounts using features the code library cannot explain, a gap that would surface immediately during an examination. For NBFCs, the operational benefit is that every model version in production is guaranteed to produce examiner-readable explanations for every feature, with no manual reconciliation required after retraining cycles.

What an RBI Examiner Sees: Per-Account Reasoning vs Standard Collections AI Output

NBFC teams evaluating how to close the account-level explainability gap have real options. Standard tools serve teams whose primary requirement is contact automation and campaign management. For teams whose scope includes producing per-account SHAP reasoning on demand during RBI examinations, the comparison criteria shift toward explainability infrastructure, audit trail depth, and retraining governance. The table below compares the criteria that matter most for NBFCs.

| Criterion | Standard Tools | iTuring |

| Account prioritisation | DPD bucket order | Daily propensity score – 25,000+ signals |

| Self-cure identification | Not available | Withholds self-cure accounts before queue loads |

| Contact timing | Fixed campaign schedule | Per-account optimal timing from behavioral signals |

| Model retraining | Quarterly or ad hoc | Continuous – outcomes retrain model automatically |

| Audit trail (RBI) | Contact logs only | Immutable per-account decision log – examination-ready |

If your NBFC’s examination requirement is aggregate model documentation only and not per-account reasoning, standard MRM audit tools may cover your scope.

Examination-Ready in 30 Minutes: What the Evidence Pack Contains

A leading NBFC in India operating across consumer lending and microfinance portfolios faced a specific gap: its collections AI model produced accurate propensity scores but could not generate per-account SHAP explanations within the timeframe expected during an RBI on-site review. The institution deployed iTuring Collections Agent with iTuring ML Governance, completing integration within four weeks of contract execution.

Results after deployment:

- 20% increase in collections recovery rate

- 43% reduction in cost per recovery

When the Examiner Asks for Account 847291 – What Your Collections AI Must Produce in That Meeting

The RBI 2024 MRM framework treats account-level explainability as a production requirement, not a documentation exercise: your collections AI must store SHAP decompositions at scoring time, not reconstruct them after an examination notice arrives. Post-hoc SHAP layers on black-box models satisfy the technical requirement but carry a documentation burden that native explainability avoids: examiners will ask whether the explanation layer was part of the original model design or added retroactively, and the answer SHAPes the finding. The 30-minute examination export standard is not aspirational; it reflects the practical reality of on-site reviews where supervisors expect same-session responses for any account they select.

iTuring generates account-level SHAP explanations on deployment day – test it against your own NBFC portfolio before any licence decision.

If your model risk team is preparing for an upcoming RBI examination cycle and needs to validate whether your collections AI can produce per-account reasoning on demand, request a demo to run iTuring against your own portfolio data and see the examination export workflow firsthand.