TL;DR

- Propensity models rank NPA accounts by payment likelihood now

- NBFC portfolios need models trained on Indian borrower behaviour

- Self-cure identification reduces unnecessary early-stage contact costs

- RBI model validation requirements apply to AI scoring models

- Treatment routing must map to each score band explicitly

Picture a collections team at an NBFC looking at a bucket of 15,000 personal loan accounts. All of them sit between 30 and 60 days past due. Every account carries the same DPD flag.

But inside that bucket are three very different borrowers. The first missed a payment because salary was delayed by a few days. The funds are sitting in the pipeline. She will pay the moment they clear, with no contact required. The second is managing four active loans across two lenders. He needs a conversation about restructuring before he can commit to a payment schedule. The third has stopped answering calls, stopped opening messages, and is six weeks away from a formal NPA classification.

A DPD flag cannot separate these three accounts. Neither can a balance-ordered queue. So the collections team works through the list in the order the system exported it. The borrower waiting on her salary receives three follow-up calls before the funds even arrive. The borrower who needed a restructuring conversation receives a payment demand that he cannot meet. The account heading toward formal NPA receives the same generic outreach as everyone else.

Propensity modeling is what separates those accounts before any contact is made. It produces a score for each borrower reflecting the probability of a specific outcome, whether payment, response, or self-cure, within a defined window. That score determines what contact happens, when, through which channel, and whether any contact should happen at all.

This blog covers what propensity modeling means for NBFC collections operations, which signals drive accuracy in Indian portfolios, how scoring changes collections economics, and what RBI requires before a propensity model goes into production.

What Propensity Modeling Means for NBFC Collections

A propensity model produces a probability score for each account. The score reflects how likely a specific borrower is to make a payment within a defined window, in response to a defined type of contact, given everything the model knows about that borrower’s behaviour and account state.

Three distinct scores are relevant to NBFC collections:

Propensity to pay estimates the likelihood of payment within a specified number of days following a contact attempt of a defined type. This score determines which accounts should receive active outreach and which treatment type is appropriate given the probability of recovery.

Propensity to respond estimates the likelihood that a borrower will answer a call, reply to a message, or engage with outbound contact. A high pay propensity combined with a low response propensity points to a contact strategy problem rather than a willingness problem. The borrower is likely to pay but unlikely to be reached through the current channel.

Propensity to self-cure estimates the likelihood of payment without any outbound contact. In Indian NBFC portfolios, a meaningful share of early-bucket accounts miss payments due to salary delays or short-term cash flow gaps and pay within days of funds clearing. Identifying these accounts before the contact cycle begins removes unnecessary outreach and frees collections capacity for accounts that genuinely need intervention.

These three scores serve distinct routing decisions and should be maintained separately. Collapsing them into a single composite score discards the specific information each one provides for treatment selection.

NBFCs operating in India need models trained on Indian portfolio data. Indian borrower payment behaviour reflects salary credit cycles, agricultural income seasonality, festival spending patterns, and regional economic conditions. These dynamics are not present in models built on Western consumer credit data. Applying such a model to an Indian NBFC portfolio means scoring borrowers against behaviour patterns that bear no relation to their actual payment environment.

Signals That Drive Propensity in Indian NBFC Portfolios

Model accuracy depends on the quality and relevance of the signals used to train it. Four signal categories are most predictive for Indian NBFC collections, each with India-specific considerations.

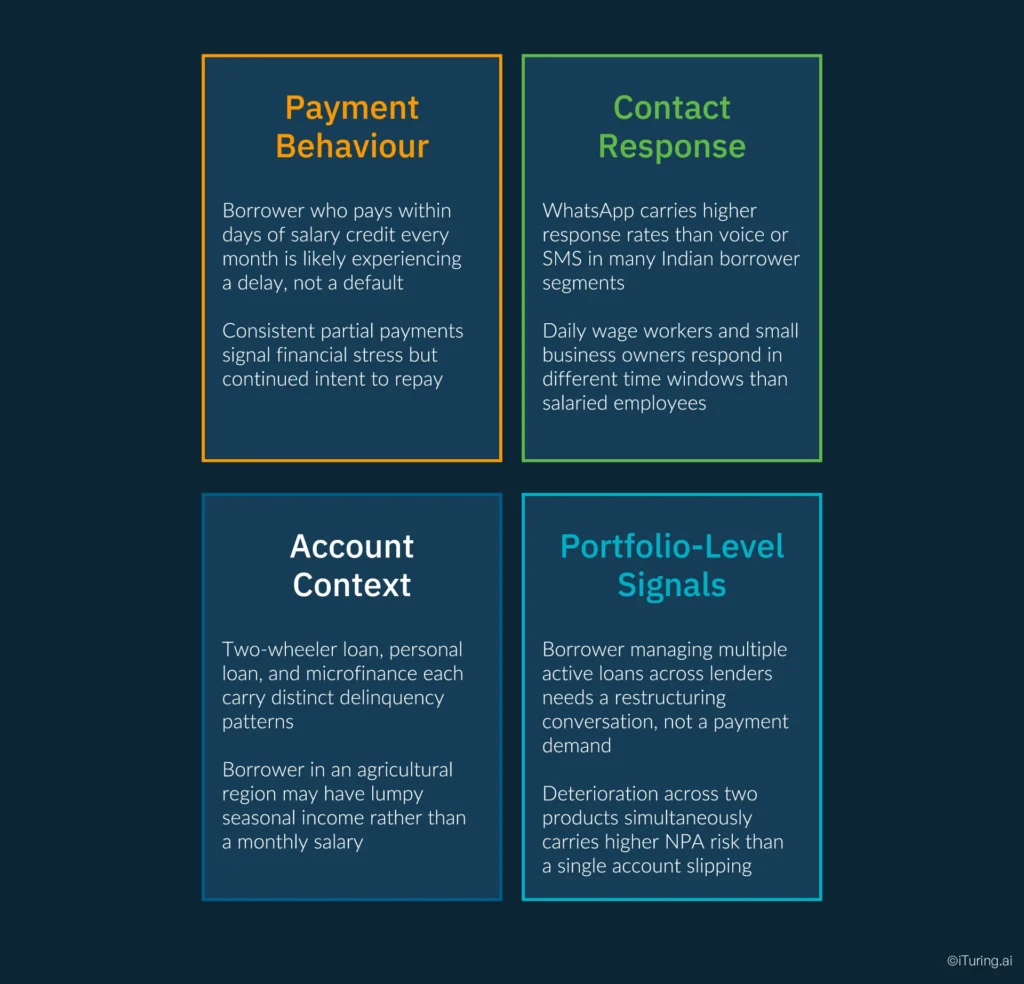

Payment Behaviour Signals

Recency, frequency, and trajectory of payments over the last three to six cycles provide the baseline signal. Within this category, salary credit date alignment is particularly important for Indian personal loan portfolios. Many borrowers pay within 48 to 72 hours of monthly salary credit. A borrower who has paid on the 5th of each month for eleven consecutive months and is now on the 12th with no payment is likely experiencing a salary processing delay, not entering a default trajectory. A model that recognises this pattern scores the account differently from one that treats any missed payment date as an equivalent risk signal.

Self-cure history adds further precision. If a borrower has previously paid three to five days late in two prior cycles without any contact, the probability of self-cure in the current cycle is materially higher than it would be for a borrower with no such history.

Partial payment patterns also carry signal. Consistent partial payments indicate financial stress but continued intent to service the debt. These accounts need a restructuring conversation, not a payment demand.

Contact Response Signals

Historical answer and response rates by channel reflect how this specific borrower engages with outreach. In many Indian NBFC borrower segments, WhatsApp carries materially higher response rates than voice or SMS. Language preference signals from past interactions affect response probability. Time-of-day patterns vary by occupation type: daily wage workers and small business owners have distinct windows when they can engage with a call that differ from salaried employees.

Promise-to-pay fulfilment history is one of the strongest forward-looking response signals. A borrower with a high PTP fulfilment rate carries a different probability profile than a borrower with repeated unfulfilled commitments.

Account Context Signals

Product type carries its own payment behaviour norms. Personal loans, two-wheeler loans, microfinance products, and small business loans each have distinct delinquency patterns shaped by the purpose of the loan and the borrower’s income structure. Loan tenor and remaining tenor affect the borrower’s relationship with the debt. Loan-to-income ratio at origination provides a proxy for underlying repayment capacity that the payment history alone does not capture.

Geographic location serves as a proxy for regional economic conditions and seasonal income patterns, particularly relevant for portfolios with exposure to agricultural regions where income is lumpy and seasonal rather than monthly.

Portfolio-Level Signals

Where an NBFC holds multiple products for the same borrower, cross-product performance is a stronger NPA prediction signal than single-account behaviour. Deterioration across two products simultaneously carries different risk implications than deterioration on one product while another remains current. Co-borrower or guarantor presence and their payment behaviour add further signal where relevant.

How Propensity Scoring Changes NBFC Collections Economics

Propensity scoring changes collections economics through three mechanisms: contact efficiency, treatment differentiation, and field visit optimisation.

Contact Efficiency

The most direct economic benefit comes from removing high self-cure accounts from the active contact queue. A 20,000-account early bucket portfolio where 12% carry high self-cure propensity represents 2,400 accounts that do not need outbound contact in the current cycle. Removing them from the queue reduces contact costs, removes unnecessary borrower friction, and directs collections capacity toward accounts where intervention produces a return.

In NBFC operations with digital contact infrastructure, removing these accounts from the queue also reduces AI voice and messaging consumption costs. In operations relying on manual calling, it reduces agent time spent on calls that would have resulted in payment regardless.

Treatment Differentiation

Propensity scores allow the collections policy to assign specific treatment types to specific score bands rather than applying a uniform contact approach across a mixed portfolio.

High propensity accounts receive a digital or voice reminder with a payment link. The cost per contact is low and the likelihood of completion without further intervention is high. Mid propensity accounts receive structured outreach with an explicit payment arrangement offer, a voice contact with an agent trained to negotiate a schedule. Low propensity accounts are referred to a specialist team or scheduled for a field visit, the highest-cost intervention directed at the accounts where it produces maximum recovery value.

This routing prevents high-cost interventions being applied uniformly across a portfolio where most of the recovery would have occurred with a low-cost digital contact.

Field Visit Optimisation

Field visits carry the highest cost per contact in the NBFC cost-to-collect stack, particularly for Tier 2 and Tier 3 market portfolios where digital contact rates are lower and physical presence is required for a meaningful share of accounts.

Propensity scoring applied to field visit planning reduces cost in two ways. First, it removes accounts with high self-cure or high digital-response propensity from the field queue, reducing the total number of visits required. Second, for accounts that do require field visits, geographic clustering of high-propensity accounts allows field agents to maximise the recovery value generated per day. A field agent visiting five high-value accounts within a two-kilometre radius generates more recovery per working day than the same agent visiting five accounts spread across 20 kilometres with mixed propensity profiles.

Field visits carry the highest cost per contact in the NBFC cost-to-collect stack. Propensity scoring ensures that cost is directed at accounts where a physical visit changes the outcome.

RBI Model Validation Requirements

A propensity model used to prioritise collections accounts and determine treatment strategies is a model under RBI’s supervisory framework. The relevant requirements flow from RBI’s model risk management guidelines, reinforced through the Digital Lending Directions and the Scale-Based Regulation framework for upper and middle-layer NBFCs.

Model Inventory

Every model in production must be documented in a model inventory. The entry should record the model’s purpose, the data inputs used, the owner within the organisation, the validation status, and the date of the last review. A propensity scoring model deployed across a material collections portfolio requires an inventory entry before it goes live.

Pre-Deployment Validation

Validation must be conducted on the NBFC’s own portfolio data, not solely on the model vendor’s benchmark dataset. Backtesting on a holdout sample drawn from the NBFC’s historical accounts tests whether the model’s rank ordering of accounts by payment probability holds on the specific population being scored. A model that performs well on a vendor benchmark but poorly on the NBFC’s actual borrower population should not be deployed.

Ongoing Monitoring

Deployed models require continuous monitoring for score distribution stability, rank-order accuracy, and feature drift. Score distribution stability checks whether the proportion of accounts falling into each score band is shifting over time. Rank-order stability checks whether high-scoring accounts continue to outperform low-scoring accounts in actual payment outcomes. Feature drift monitors whether the input signals feeding the model are changing in ways that reduce its predictive accuracy.

Each of these monitoring checks should have a documented threshold that triggers a model review and, if necessary, retraining.

Model Risk Committee Oversight

Material models require oversight from the NBFC’s model risk committee or equivalent governance body. A propensity model deployed across the collections portfolio of an upper-layer NBFC will typically meet the materiality threshold. The committee should review pre-deployment validation findings, approve deployment, review ongoing monitoring reports at defined intervals, and sign off on any material changes to the model.

Vendor Models and Validation Responsibility

RBI places validation responsibility on the NBFC, not the model vendor. An NBFC using a third-party propensity model cannot rely on the vendor’s own validation documentation to satisfy its regulatory obligations. The NBFC must conduct its own validation on its own portfolio data and retain that documentation for supervisory review.

Fair Practices Testing

RBI’s fair practices code and consumer protection guidelines require that AI-driven collections treatment does not systematically disadvantage borrowers based on protected characteristics. A propensity model trained on historical portfolio data may encode patterns that produce different treatment outcomes by geography, language, occupation, or other characteristics correlated with protected attributes. Pre-deployment testing for differential outcomes across borrower segments is required before the model goes into production.

The Queue Order Is a Collections Strategy. Make It a Deliberate One.

Every collections operation works a queue. The question is what determines the order. DPD rank, balance rank, and system export order are all queue strategies. They are also strategies that apply no information about the borrower’s actual likelihood of paying, responding, or self-curing.

Propensity scoring replaces an implicit queue strategy with an explicit one: accounts are ordered by the probability of a defined outcome, and treatments are assigned based on where each account falls in that distribution. The decision about who to contact, when, through which channel, and at what cost becomes deliberate rather than default.

For Indian NBFCs managing personal loan portfolios across diverse borrower segments, the gain from making that decision deliberately is material. A model that reflects Indian salary cycles, regional seasonality, product-type norms, and channel response patterns will consistently outperform a model that does not, in the specific population where the decisions are being made.

Five markers of a well-designed propensity scoring programme for Indian NBFCs:

- Separate scores maintained for pay, respond, and self-cure propensity, each serving a distinct routing decision

- Training data drawn from Indian NBFC portfolio behaviour, including salary cycle patterns, regional income seasonality, and product-type norms relevant to the NBFC’s specific lending profile

- Treatment routing is explicit and documented in collections policy: each score band maps to a defined treatment type

- Score distribution stability, rank-order accuracy, and feature drift monitored continuously, with a documented retraining trigger when drift exceeds a defined threshold

- Full RBI governance compliance: model inventory entry, pre-deployment validation on NBFC-specific data, ongoing monitoring documentation, model risk committee oversight for material models, and pre-deployment fair practices testing

iTuring’s AI collections platform deploys separate propensity scores for pay, respond, and self-cure behaviour, trained on Indian NBFC portfolio data, with native RBI model governance documentation built into the deployment framework.