SARFAESI Workflow Automation: How Indian Banks Digitize Secured NPA Enforcement and Reduce Recovery Time by 35%

TL;DR 603 days. That is the average time an Indian bank spends recovering a secured NPA through a contested enforcement process, according to Parliamentary data tabled in the Lok Sabha in December 2025. Six hundred and three days, after excluding the time spent simply waiting for the process to begin. The Securitisation and Reconstruction of […]

Explainable AI in Banking: Meeting OCC Requirements for AI Model Transparency in Collections and Underwriting

TL;DR Model risk executives at US banks face a new ai governance requirement in 2026. OCC examiners are rejecting black-box AI models during SR 11-7 validation even when those models outperform traditional logistic regression scorecards on every performance metric. The Comptroller’s Handbook on Model Risk Management now explicitly addresses AI use cases including credit underwriting, […]

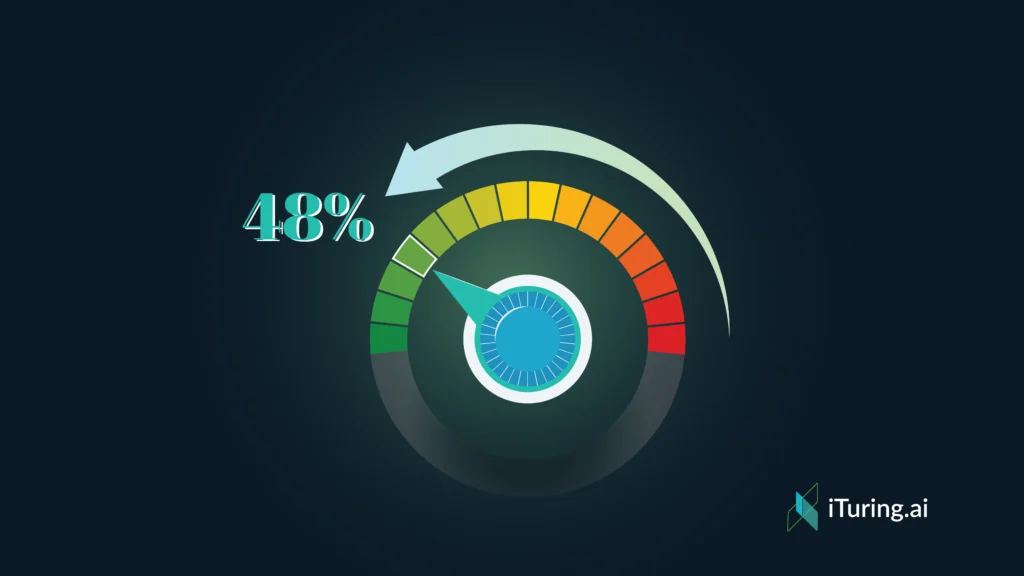

Collections Automation in Banking: Reducing Cost-Per-Recovery by 48% While Staying FDCPA Compliant

TL;DR US bank collections leaders face two pressures simultaneously. Collections operating expense is rising as agent attrition hits 40-60% annually and wage inflation compounds the cost of replacement training. At the same time, FDCPA enforcement is intensifying: the CFPB’s 2025 supervisory highlights identified collections as a priority area, with $48 million in civil monetary penalties […]

Predictive Analytics for Collections: How US Banks Use AI to Predict Payment Behavior 120 Days Before Delinquency

TL;DR Picture a Monday morning at a mid-size US bank. The collections team opens their queue. Thousands of accounts stare back at them, every one of them already 15 to 30 days past due. Some are at 60 days. A few have crossed into serious delinquency. The team puts on their headsets and starts making […]

Model Governance for AI Collections: Building a Framework That Passes OCC and Federal Reserve Examination

TL;DR Who owns your AI collections propensity model? Who approved the last parameter update, and where is that approval documented? When the model retrains next month, who decides whether that constitutes a material change requiring full revalidation or a routine update that can proceed under expedited review? If your collections AI includes agents hosted by […]

Credit Risk Models for South African Banks: Building TCF-Compliant Underwriting AI Under Basel III

TL;DR A South African bank CRO building or reviewing an AI credit risk scoring model in 2026 faces three regulatory demands simultaneously, each from a different supervisory body, each with its own documentation requirements, and each carrying its own examination consequences. The Prudential Authority requires that IRB credit risk scoring models are validated to Basel […]

AI Governance Monitoring for Collections: What South African Banks and Insurers Need Under FSCA

TL;DR In November 2025, the Prudential Authority and the FSCA published their joint report on AI adoption across South Africa’s financial sector. The finding on ai governance monitoring was precise: governance frameworks for AI are still developing across the sector and vary widely in maturity, with many institutions relying on existing risk-management structures rather than […]

Model Governance for AI Collections in South Africa: Meeting FSCA Validation Standards and Basel III Requirements

TL;DR The KPMG South Africa Ten Key Regulatory Challenges for 2025 places AI model validation and continuous monitoring at the centre of the financial services governance agenda, identifying these as the most critical technical requirements that South African banks must address for AI systems: rigorous testing and validation before deployment, continuous monitoring after deployment, and […]

Churn Prediction for South African Banks and Insurers: Using AI to Prevent Customer Loss Before It Happens

TL;DR Acquiring a new retail banking customer in South Africa costs between R800 and R2,500 depending on the acquisition channel, product type, and customer segment. Retaining an existing one costs a fraction of that figure, provided the institution knows the customer is at risk before they leave. Churn prediction is the capability that creates that […]

AI Credit Underwriting for Indian Banks and NBFCs: How to Expand Credit Access While Managing Risk

TL;DR For most Indian bank and NBFC leaders, AI credit underwriting presents itself as a dilemma: expand credit access to underserved borrowers, or maintain rigorous risk management. The instinct is to treat this as a trade-off, that you can do one but doing both simultaneously requires compromise. This framing is wrong, and the evidence from […]