TL;DR

- 72% of Indian lending startups already use AI-based underwriting

- Alternative data improves predictive power by up to 25% for thin-file borrowers

- RBI’s August 2024 Model Risk Circular classifies AI lending models as high-risk financial instruments

- Algorithmic bias is a real deployment risk in India, not a theoretical concern

- Five RBI requirements are non-negotiable before any AI underwriting deployment

For most Indian bank and NBFC leaders, AI credit underwriting presents itself as a dilemma: expand credit access to underserved borrowers, or maintain rigorous risk management. The instinct is to treat this as a trade-off, that you can do one but doing both simultaneously requires compromise.

This framing is wrong, and the evidence from India’s own credit market is what disproves it.

NBFCs are projected to grow credit at 17 percent annually versus 12 percent for banks, and AI underwriting is a central reason the gap is widening. The institutions gaining ground are not doing so by lowering risk standards. They are doing so by replacing the blunt instrument of traditional credit bureau scoring, which systematically excludes creditworthy thin-file borrowers, with AI models that can assess risk accurately using data that a traditional scorecard cannot process. The borrower who has no formal credit history but has three years of consistent UPI transaction behaviour, GST filing regularity, and a NACH mandate track record is not a high-risk borrower. A traditional scorecard treats them as unassessable. An AI credit model can assess them.

This article covers what AI credit underwriting actually means for Indian institutions, where it reliably delivers, where it does not yet deliver despite vendor claims, what RBI requires before any AI underwriting system goes live, and the questions every CEO and CRO should bring into a vendor conversation.

What AI Credit Underwriting Actually Means

The term “AI credit underwriting” is used to describe a broad range of capabilities, from fully automated instant loan decisioning to AI-assisted scorecard development that still routes decisions through a human underwriter. The distinction matters significantly for Indian institutions evaluating vendor claims.

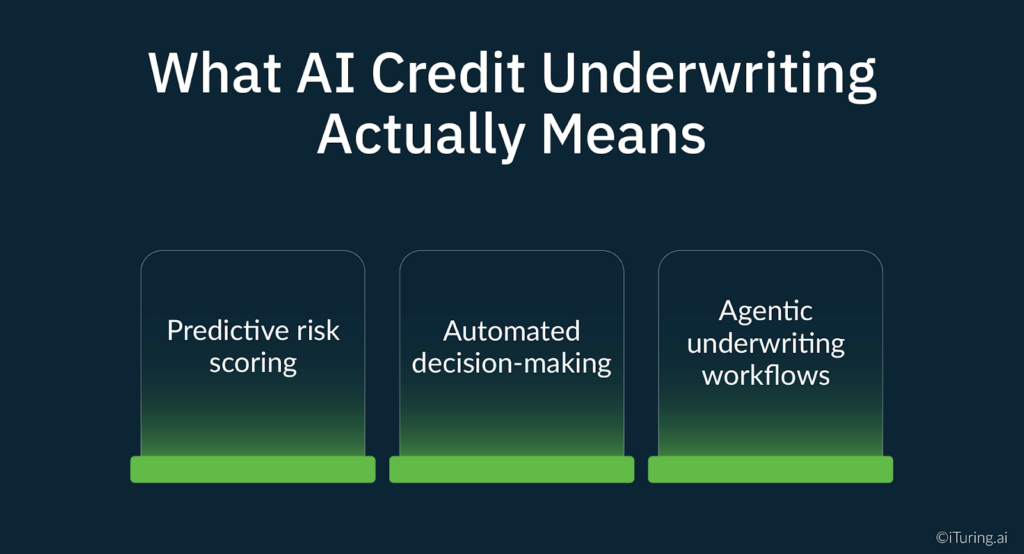

Underwriting automation, the replacement of manual credit assessment steps with AI-driven processes, sits on a spectrum from partial to full, and the right deployment point on that spectrum depends on the loan product, borrower segment, and regulatory context. At its core, AI credit underwriting uses machine learning models to assess borrower risk by analysing a combination of traditional bureau data, financial statement data, and alternative behavioural signals. It is not one system, it is three distinct capabilities each with its own deployment maturity in the Indian market.

Predictive risk scoring. An AI model replaces or supplements the traditional credit scorecard, generating a risk score from a broader feature set. In the Indian context, this includes CIBIL, Experian, CRIF, and Equifax bureau data alongside bank statement analysis, GST filing behaviour, UPI transaction patterns, and supply chain payment history. At the core of this capability is probability of default estimation: the model does not simply rank borrowers by relative risk, it generates a calibrated probability of default that drives loan pricing, limit setting, and policy rule application. World Bank research shows that combining traditional bureau data with alternative data improves credit risk scoring accuracy by up to 25 percent for thin-file borrowers. This is the most mature AI underwriting capability in India and the one with the most deployment evidence.

Automated decision-making. The AI model’s risk score is connected to a credit risk decisioning policy engine that approves, declines, or routes applications to human review without human involvement in the initial decisioning. The policy engine applies institution-defined rules, loan-to-income thresholds, bureau exclusion criteria, product-specific guardrails, against the AI risk score to produce a fully automated decision. For small-ticket personal loans, pre-approved credit line activation, and MSME supply chain financing, this capability is deployed and working in India. For larger secured loans where collateral assessment and borrower character judgment remain significant, human review remains part of the process.

Agentic underwriting workflows. Multiple AI agents collaborate across the underwriting process: one agent extracts and validates documents, another analyses bank statements, another checks bureau data, another applies the policy engine, and an orchestration layer assembles the output for human review or automated decision. This is the emerging capability frontier in Indian credit underwriting for 2026 and beyond.

What Works Well in the Indian Context

Thin-file and new-to-credit borrower scoring. India has an estimated 160 to 190 million thin-file borrowers, adults with limited or no formal credit history but demonstrable financial behaviour. The self-employed kirana owner, the urban migrant worker, the first-generation MSME entrepreneur: these borrowers are routinely declined by traditional credit risk scoring not because they are bad credit risks, but because the scorecard has no data to assess them. AI models trained on digital transaction behaviour, NACH mandate performance, and GST filing history can generate reliable risk scores and calibrated probability of default estimates for these borrowers, opening a segment that represents one of India’s largest untapped credit opportunities.

Cash flow-based MSME lending. India’s MSME sector contributes over 30 percent of GDP but remains significantly underserved by formal credit. Many small businesses lack collateral, formal income documentation, and credit history. AI-driven cash flow analysis using bank statement data, GST returns, and supply chain transaction records allows lenders to assess MSME creditworthiness from actual financial behaviour rather than documentation proxies. The AI model converts that cash flow data into a calibrated probability of default for each MSME borrower, enabling pricing and limit decisions that reflect true repayment capacity. NBFCs using this capability are deploying it for working capital loans, supply chain financing, and equipment financing at ticket sizes where traditional underwriting is economically unviable.

Pre-approved credit line automation. For existing customers where the bank already holds transaction and repayment history, AI models can generate pre-approved credit line offers continuously and automatically, without a new application or human underwriting involvement. The conversion rates on well-personalised pre-approved offers, calibrated to the borrower’s demonstrated repayment capacity and current financial stress signals, consistently outperform generic credit line offers by 35 to 50 percent.

Small-ticket personal loan decisioning. For loans below Rs. 1 to 2 lakh to salaried borrowers with a bureau history, fully automated AI underwriting is mature, deployed, and delivering lower default rates than manual underwriting in multiple Indian institution deployments. The combination of salary account transaction analysis and bureau data provides sufficient input signal for reliable automated decisions in this segment.

What Does Not Work Yet

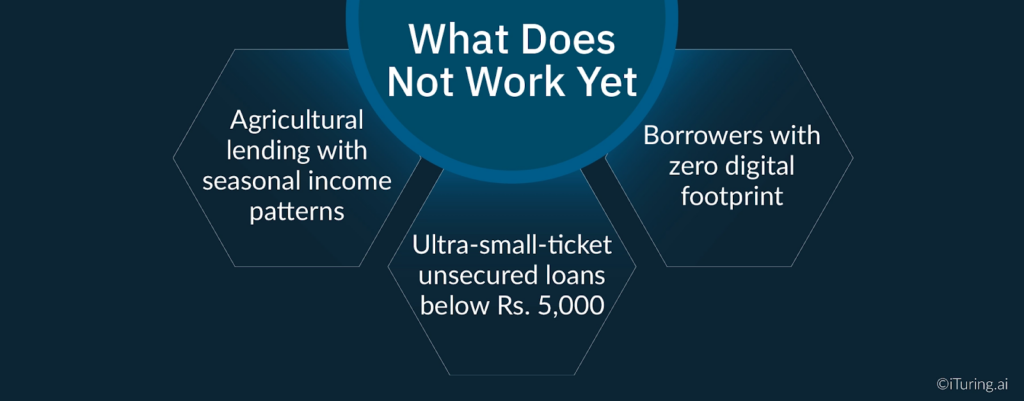

An honest assessment of AI credit underwriting for Indian institutions must include the segments where the capability is not yet reliable, regardless of vendor claims.

Agricultural lending with seasonal income patterns. Agricultural income in India is deeply seasonal and regionally variable, dependent on monsoon performance, crop price volatility, and local mandi dynamics. AI models trained on general credit behaviour do not reliably capture the risk profile of a farmer whose income is structurally lumpy, who may have zero bank account inflows for four months and a large lump sum after harvest. Human underwriting with local market knowledge remains more reliable in this segment.

Ultra-small-ticket unsecured loans below Rs. 5,000. The cost of AI model governance, compliance documentation, and regulatory audit trail for a loan of Rs. 3,000 can approach the economics of the loan itself. Microfinance lending at this ticket size is better served by group lending models and NBFC-MFI frameworks than by individual AI credit decisioning.

Borrowers with zero digital footprint. Approximately 20 to 25 percent of India’s adult population remains outside the digital transaction ecosystem. No UPI history, no GST registration, no formal bank account activity. For this segment, alternative data AI underwriting has no usable signal. Serving these borrowers requires either field-based assessment or waiting for their digital footprint to develop. No AI system should be deployed for this segment with confidence.

What RBI Requires Before Any AI Underwriting Goes Live

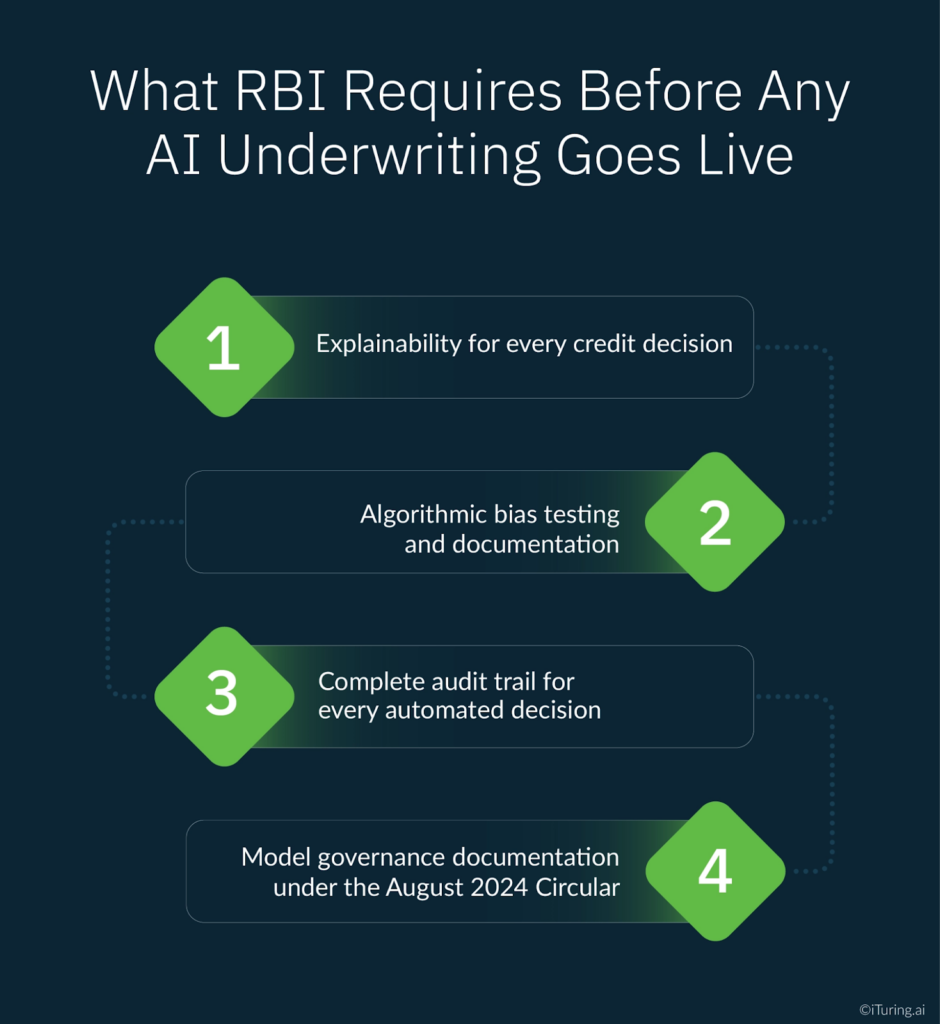

The RBI’s August 2024 Draft Circular on Model Risk Management marked a regulatory turning point: AI models in lending are now classified as high-risk financial instruments requiring specific model risk management treatment. Institutions that deploy AI credit underwriting without satisfying these five requirements are not compliant with the current RBI framework.

Explainability for every credit decision. The RBI and MeitY have both specified that AI-based credit models must disclose why a loan was approved or rejected. A borrower who receives an adverse credit decision has the right to a reason. The model must be capable of generating an account-level explanation for every decision it makes, in a format that is both legally defensible and comprehensible to the borrower. SHAP-based explanations are the current standard for satisfying this requirement.

Algorithmic bias testing and documentation. The Atlantis Press analysis of automated credit decisioning under DPDP Act and RBI guidelines identifies that AI credit models may inadvertently discriminate against women, rural borrowers, informal workers, and individuals from specific geographies due to proxy variables in the training data. RBI examination is beginning to require documented evidence of bias testing across protected characteristics before AI underwriting models are approved for production. Pre-deployment bias testing and ongoing monitoring for disparate impact are now operational requirements, not good practices.

Complete audit trail for every automated decision. Every AI-generated credit decision must produce a complete, retrievable audit trail: input data used, model version applied, score generated, policy rule triggered, and decision output. The audit trail must be stored in India-region data centres in compliance with DPDP Act localisation requirements and must be retrievable for RBI examination on request.

Model governance documentation under the August 2024 Circular. AI credit models must be inventoried, validated before deployment, monitored continuously after deployment, and governed through a documented change management process. The CRO and CTO are expected to sign model validation certificates. The board audit committee is expected to receive periodic reporting on AI model performance and governance.

DPDP Act compliance for data used in credit decisioning. Every data source feeding an AI credit model must have valid borrower consent for use in credit decisioning. Bank statement data accessed through Account Aggregator requires specific consent for credit assessment use. GST data, UPI transaction data, and social signal data each have distinct consent requirements under the DPDP Act 2023. A model that generates accurate credit scores from data obtained without proper consent is a regulatory liability regardless of its predictive performance.

Questions Every CEO and CRO Should Ask Before Signing

Can you demonstrate a live account-level credit decision explanation? Not a sample output. Not a slide. A live SHAP explanation for a recent actual credit decision made by the model, showing which features drove the approval or rejection. If the vendor cannot demonstrate this, the model is not explainable at the standard RBI now requires.

What is your documented approach to algorithmic bias testing? Ask for the bias testing methodology, the protected characteristics tested, the frequency of bias monitoring after deployment, and the remediation process when bias is detected. A vendor without a documented bias testing protocol is not ready for the Indian regulatory environment as it stands in 2026.

How does your model handle thin-file borrowers, specifically what alternative data sources are integrated and how is consent managed for each? The answer must be specific about data sources and consent architecture, not generic about “alternative data.” Each data source has its own consent requirements under the DPDP Act, and the vendor must demonstrate they have mapped and managed them.

Who are your Indian bank and NBFC reference clients, and what segment are they deploying in? A vendor with Indian reference clients only in the fintech or payments space is not validated for a scheduled commercial bank or upper-layer NBFC deployment. Reference clients must be directly comparable in institutional type and regulatory context.

What is your model retraining governance process, and who owns validation after retraining? Under the August 2024 Circular, every material model change requires documented model risk management governance before the updated credit risk decisioning model returns to production. The vendor must describe who approves retraining, how material changes are defined, and how the validation documentation is produced.

How iTuring Addresses This

iTuring’s AI credit underwriting platform is designed specifically for the Indian regulatory environment as defined by the August 2024 Model Risk Circular and the DPDP Act 2023. The platform covers the full underwriting automation spectrum, from predictive credit risk scoring for thin-file borrowers to fully automated credit risk decisioning for small-ticket loans, with model risk management governance built in at every stage.

The platform’s underwriting models are trained on Indian credit data with validated performance on thin-file borrower segments, including UPI transaction behaviour, Account Aggregator bank statement data, and GST filing analysis as core alternative data sources. Probability of default estimates are generated at the account level and connected directly to the institution’s pricing and limit-setting policy engine. SHAP-based account-level explanations are generated automatically for every credit decision, in the borrower’s registered language, satisfying both RBI explainability requirements and DPDP Act right-to-explanation obligations.

Pre-deployment bias testing across gender, geography, income tier, and employment type is part of every model validation cycle, with ongoing monitoring for disparate impact built into the post-deployment governance module. All data used in credit decisioning is managed under a consent architecture that maps each alternative data source to its specific DPDP Act consent requirement.

Model governance documentation, including validation certificates, audit trail exports, and board reporting packs, are generated in the format required by the August 2024 Circular and structured for RBI examination review.

Regulatory Disclaimer

This article is for informational purposes only and does not constitute legal or compliance advice. RBI guidelines on AI model risk management, Digital Lending Master Direction requirements, and DPDP Act obligations are subject to change. The August 2024 Draft Circular on Model Risk Management is subject to finalisation. Information presented reflects publicly available RBI guidance and industry data as of the publication date. Consult qualified legal and compliance professionals for guidance specific to your institution.

Sources: Sahi: Banks vs NBFCs AI Credit Race India 2026 | LinkedIn: NBFCs Set to Eclipse Banks by 2035 | Credable: AI Credit Underwriting Guide 2026 | EngineerBabu: AI in Credit Scoring 2026 Guide | OPL Innovate: India’s Lending Infrastructure AI Models | BillCut: Responsible AI in Lending India 2025 | IRJWEB: Algorithmic Bias in AI Credit Scoring India | Godrej Capital: AI Credit Scoring MSME India 2026 | Atlantis Press: Automated Decisioning DPDP Act RBI | Saarathi.ai: Algorithmic Bias Loan Approvals India | Think360: Digital Lending India 2025 Lessons | LinkedIn: AI Lending RBI Guidelines Black Box to Glass Box