TL;DR

- SARFAESI allows secured NPA enforcement without court intervention

- Section 13(2) gives borrowers 60 days to repay before asset seizure

- SARFAESI recovery rate rose to 31.5% in FY25, up from 25.4% in FY24

- Manual workflows lose 26 to 39 days per case to avoidable delays

- Automation cuts recovery timelines from 18-24 months to 12-16 months

603 days.

That is the average time an Indian bank spends recovering a secured NPA through a contested enforcement process, according to Parliamentary data tabled in the Lok Sabha in December 2025. Six hundred and three days, after excluding the time spent simply waiting for the process to begin.

The Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest (SARFAESI) Act, 2002, was designed specifically to prevent this. It gave Indian banks the right to enforce security interest and recover secured loans without filing a civil suit, without waiting for a court decree, and without the delays that had paralyzed NPA recovery for decades before the law came into effect. It was a genuine breakthrough.

Twenty-three years later, most Indian banks are still managing SARFAESI enforcement through a combination of Word documents, email chains, physical files, and manual escalations. The legal framework carries substantial enforcement power. The operational execution surrounding it has not kept pace. That gap, between what SARFAESI permits and how efficiently banks actually use it, is precisely where underwriting automation and ai for banks deployment deliver their most concrete collections value. The same data infrastructure that classified the secured loan at origination holds everything needed to trigger, document, and track enforcement without manual re-entry at any stage.

This post explains the SARFAESI enforcement process in detail, maps where manual workflows lose the most time, and shows what a fully automated digital enforcement operation looks like in practice.

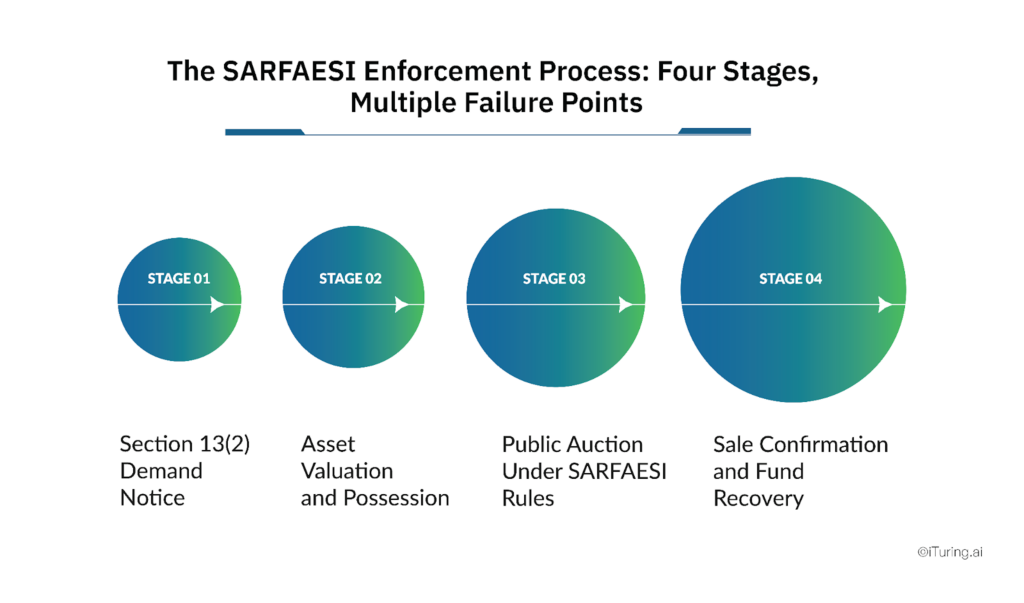

The SARFAESI Enforcement Process: Four Stages, Multiple Failure Points

Before understanding where automation helps, you need to understand what the enforcement process actually involves. There are four sequential stages, each with its own legal requirements, timelines, and documentation obligations.

Stage 1: Section 13(2) Demand Notice

The process begins when a loan account is classified as a Non-Performing Asset, typically after 90 days of default. The credit risk decisioning layer that triggered the NPA classification is also the source of the data that feeds the Section 13(2) notice: outstanding balance, interest calculation, asset description, and borrower identification all flow from the same credit risk scoring record that marked the account as enforcement-eligible. The bank issues a formal demand notice to the borrower under Section 13(2) of the SARFAESI Act, specifying the total outstanding dues and the secured assets against which the bank intends to enforce its interest.

The borrower has 60 days from the date of the notice to repay the outstanding dues in full. Within this period, the borrower may submit representations or objections under Section 13(3A), and the bank is legally required to respond in writing within 15 days, either justifying the action or modifying the notice.

The notice must be served via registered post or email. Its language must comply with the SARFAESI Act’s format requirements. An incorrectly drafted or improperly served notice can be challenged before the Debt Recovery Tribunal and, if upheld, invalidates the entire enforcement action, forcing the bank to restart the process from Stage 1.

Stage 2: Asset Valuation and Possession

If the borrower does not repay within the 60-day notice period, the bank may proceed under Section 13(4) to take possession of the secured asset, appoint a manager to manage the asset, or require third parties owing money to the borrower to pay directly to the bank.

Before possession, the bank must obtain an independent valuation of the secured asset from a registered valuer. This valuation determines the reserve price for the subsequent auction. The bank must also serve a possession notice, which must be affixed to the property and published in two newspapers, one in English and one in the regional language of the area where the property is located.

Stage 3: Public Auction Under SARFAESI Rules

The auction must be publicly announced with a minimum 30-day notice period after the possession notice. Indian banks use the IBAPI (Indian Banks Auctions Mortgaged Properties Information) portal, an initiative of the Indian Banks Association, as the common platform for listing and conducting e-auctions of mortgaged properties. Bidders register on IBAPI, and the auction proceeds through MSTC’s e-auction platform with digital signature verification and a real-time live bidding process.

Stage 4: Sale Confirmation and Fund Recovery

Once the auction is complete and the highest bid accepted, the bank issues a sale certificate. The proceeds are applied first to the outstanding loan balance, then to interest and costs. If the sale proceeds are insufficient to cover the full dues, the bank may apply to the Debt Recovery Tribunal for recovery of the balance amount.

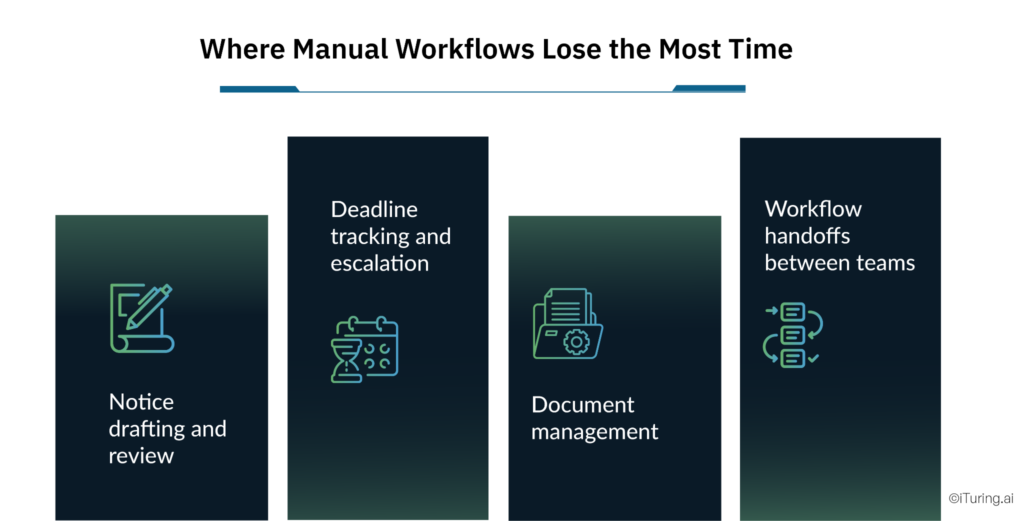

Where Manual Workflows Lose the Most Time

Every stage of the SARFAESI process has a defined legal timeline. The problem is the operational execution that surrounds it. In a manual workflow environment, time bleeds out at predictable points.

Notice drafting and review. A Section 13(2) notice is a legal document. Every instance requires the correct borrower details, outstanding balance, interest calculation, asset description, and statutory language to be assembled accurately. In a manual workflow, a legal or collections officer drafts this using a template, checks it against the loan file, gets it reviewed, obtains approval, and dispatches it. This process takes 5 to 7 working days per case on average. Across a portfolio of 500 active SARFAESI cases, that is 2,500 to 3,500 working days consumed by a single, automatable step.

Deadline tracking and escalation. The 60-day notice period. The 15-day objection response window. The 30-day auction notice period. The DRT’s statutory 60-day disposal target, confirmed by a Supreme Court ruling in October 2025 as a binding obligation. Each of these deadlines requires active monitoring. In a spreadsheet-based tracking system, missed deadlines are a question of when, not whether. The average manual operation loses 10 to 15 days per case to deadline slippage, missed escalations, delayed responses, and approvals that sat in someone’s inbox over a long weekend.

Document management. Every SARFAESI case generates a significant volume of documents: the loan agreement, mortgage deed, demand notice, borrower objections, bank response, possession notice, newspaper publication receipts, valuation report, auction advertisement, bidder communications, and sale certificate. In a physical or semi-digital filing system, locating a specific document for an audit request or DRT hearing takes 3 to 5 days. In a DRT proceeding where the hearing date is fixed and documents must be filed by a specific date, this is a substantive legal risk.

Workflow handoffs between teams. A SARFAESI case passes through the collections team, legal team, valuation team, auction team, and finance team at different stages. Each handoff in a manual workflow requires a briefing, a document transfer, and a fresh review of case history. The average inter-team handoff adds 8 to 12 days of calendar time per case, not because any individual is slow, but because parallel priorities, incomplete handoff notes, and fragmented information create re-work at every transition.

What SARFAESI Workflow Automation Actually Means

Automation in the SARFAESI context means something specific. The objective is removing the manual administrative burden that surrounds legal judgment, so that recovery teams spend their time on decisions rather than on documentation, tracking, and coordination. Underwriting automation extends into this enforcement layer: the credit data assembled at origination and maintained through the loan’s life becomes the source material for automated enforcement workflows without requiring manual extraction or re-entry at any stage.

A fully automated SARFAESI workflow has five functional layers.

Automated case initiation. When a loan account crosses the NPA classification threshold in the core banking system (whether Finacle, Oracle Flexcube, or TCS BaNCS, the three dominant platforms in Indian banking), the credit risk decisioning integration layer triggers the SARFAESI workflow automatically. The case is created with all account data pre-populated from the credit risk scoring record: borrower details, outstanding balance, interest calculations, secured asset description, and enforcement eligibility status. No manual data entry. No transcription errors.

Automated notice generation. Section 13(2) notices are generated from legally validated templates that pull borrower details, outstanding balance, interest calculations, and asset descriptions directly from the core banking system. The notice is assembled, reviewed for completeness by the system, and routed for legal sign-off in a single workflow step. What took 5 to 7 days takes hours.

Deadline tracking with automated escalation. Every legal deadline in the SARFAESI timeline is tracked at the case level. When a deadline approaches, the system escalates automatically: first to the assigned officer, then to the team lead, then to the recovery head if no action is taken. No case misses its window because it sat in a queue that no one reviewed.

Centralised document repository. Every document generated or received in the SARFAESI process is stored in a structured, searchable repository linked to the case ID. When a DRT hearing date is confirmed, the legal team can pull every document for that case in minutes, not days.

IBAPI and auction platform integration. Property details are pushed directly from the case management system to the IBAPI portal for e-auction listing. Bidder communications, auction results, and sale confirmation documents are pulled back into the case record automatically. The auction team no longer manually re-enters data between systems.

The 35% Recovery Timeline Reduction: The Arithmetic

The 35% reduction in recovery timelines comes from compounding the time savings across each automated step. Earlier identification of enforcement-eligible accounts through accurate credit risk scoring at the NPA classification stage contributes additional days at the front of the timeline, before any manual process has even begun.

| Manual Step | Time Lost (Manual) | Time With Automation | Saving Per Case |

| Notice drafting and dispatch | 5-7 days | Same day | 5-7 days |

| Deadline tracking and escalation | 10-15 days | 0 days | 10-15 days |

| Document retrieval for audits / DRT | 3-5 days | Same day | 3-5 days |

| Inter-team workflow handoffs | 8-12 days | 1 day | 7-11 days |

| Total per case | 26-39 days | 1-2 days | 24-37 days |

Against a baseline recovery timeline of 18 to 24 months (540 to 720 calendar days), saving 24 to 37 working days per case (roughly 30 to 50 calendar days) produces a 12 to 16 month recovery timeline. That is a 33 to 35% reduction, and it compounds further as the quality of documentation improves and DRT challenges become less frequent.

The improvement in asset realization follows naturally. SARFAESI recovery rates rose to 31.5% in FY 2024-25 from 25.4% in FY 2023-24, according to RBI data, a 24% year-on-year improvement driven in part by better process execution. Faster auctions reduce asset deterioration between possession and sale. Better documentation reduces successful DRT challenges that force realization at distressed prices. Both factors improve the eventual recovery percentage.

Compliance and Legal Defensibility

Every SARFAESI enforcement action must survive scrutiny at the Debt Recovery Tribunal if the borrower exercises their right to challenge under Section 17 of the SARFAESI Act. The DRT must dispose of the application within 60 days, extendable to 4 months. A bank whose documentation is incomplete, whose timelines are inconsistent, or whose notice does not meet the statutory format requirements faces a real risk of the enforcement action being stayed or set aside.

Automated workflows build legal defensibility into every step. Every notice is generated from a legally validated template. Every action is timestamped. Every document is stored with an unbroken chain of custody. When the bank’s legal team walks into a DRT hearing, the case file is complete, accurate, and structured in the format the tribunal requires.

For ai for banks deployments that incorporate AI-assisted account classification and enforcement eligibility scoring, the compliance obligation extends to the model layer. RBI examiners reviewing NPA recovery operations increasingly ask for model monitoring records demonstrating that the credit risk decisioning models driving NPA classification and SARFAESI eligibility assessments have remained within their validated parameters throughout the period under review. A complete model monitoring evidence trail alongside the process audit trail answers those questions immediately and constitutes the full governance record that both RBI inspection teams and DRT proceedings require.

How iTuring Addresses This

iTuring’s platform provides end-to-end SARFAESI workflow automation, combining underwriting automation data flows with collections enforcement execution in a single integrated architecture. The platform integrates directly with Finacle, Oracle Flexcube, and TCS BaNCS to initiate cases automatically at NPA classification, drawing on the credit risk decisioning and credit risk scoring records already held in the core banking system to pre-populate every enforcement workflow without manual re-entry.

Legally validated Section 13(2) notice templates generate with a single approval step. All deadlines are tracked and escalated automatically across the full statutory timeline. Documents are stored in a centralised repository with full search capability. IBAPI integration handles e-auction listing and result capture without manual re-entry. Model monitoring records covering the credit risk decisioning models that feed the enforcement eligibility layer are maintained continuously and compiled alongside the process audit trail in a one-click examination-ready format for both RBI inspections and DRT proceedings.

This is ai for banks built for the Indian secured NPA enforcement environment specifically: not a generic workflow tool configured for collections, but an enforcement automation platform designed around SARFAESI’s statutory structure from the architecture up.

For NPA recovery heads looking to understand where their current SARFAESI process is losing the most time,

Regulatory Disclaimer

The information in this blog is provided for general informational purposes only and does not constitute legal, regulatory, or compliance advice. SARFAESI Act enforcement in India is governed by the Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002, the Security Interest (Enforcement) Rules, 2002, RBI’s NPA classification guidelines, and applicable judicial precedents. Recovery timelines and realization rates are subject to case-specific factors including borrower cooperation, asset type, jurisdictional DRT capacity, and legal challenges. Banks and NBFCs should consult qualified legal counsel for advice on SARFAESI enforcement in specific cases. iTuring’s stated performance metrics are based on client implementations and may vary depending on portfolio composition, data quality, and deployment configuration.

Sources: Lok Sabha: Parliamentary Data on NPA Recovery Timelines December 2025 | The Legal School: Section 13 SARFAESI Act | Bajaj Finserv: Understanding Section 13(2) of SARFAESI Act | GK Today: Notice of Demand Section 13(2) SARFAESI | IBAPI: Indian Banks Auctions Mortgaged Properties Portal | Reed Law: Supreme Court DRTs SARFAESI Applications | BFSI Economic Times: Indian Banks Recovery Rates FY25