TL;DR

- Approximately 8.2 million risk policies lapsed in South Africa in the year ending early 2025

- Acquiring a new banking customer costs 5 to 7 times more than retaining an existing one

- AI churn prediction has delivered a 29% reduction in lapse and churn in documented deployments

- The most expensive mistake in South African collections is applying debt collection intensity to a customer who is on the verge of voluntary exit

- TCF Outcomes 3 and 6 both impose positive obligations on how institutions handle at-risk customers

Acquiring a new retail banking customer in South Africa costs between R800 and R2,500 depending on the acquisition channel, product type, and customer segment. Retaining an existing one costs a fraction of that figure, provided the institution knows the customer is at risk before they leave. Churn prediction is the capability that creates that knowledge, converting a retrospective loss event into a prospective intervention window, at a point when the relationship is still recoverable.

Most do not know. The average banking customer retention rate in financial services sits at approximately 75 to 78 percent globally, which means South African banks are losing roughly 1 in 4 customers within a given measurement period. In insurance, the numbers are more severe: approximately 8.2 million risk policies lapsed in South Africa in the year ending early 2025, representing a lapse rate that consumes a material portion of the new business written in the same period.

Behind each of those lapses is a signal that preceded it. The customer’s transactional behaviour changed. Their engagement with the institution’s digital channels dropped. Their premium payment pattern shifted. Their service interaction history showed unresolved friction. In the weeks before a customer left, the data told a story that a well-calibrated AI churn prediction model would have read clearly, and that a manual retention team scanning spreadsheets would have missed entirely. Effective customer churn prediction does not predict that a customer will leave, it predicts it early enough that a well-designed intervention can change the outcome.

This article covers what AI churn prediction actually does for South African banks and insurers, the signals that matter in the South African market specifically, the relationship between churn prediction and collections strategy that most institutions have not yet recognised, and how TCF Outcomes 3 and 6 apply when a customer enters the at-risk zone.

What Churn Prediction Models Actually Predict

The term churn encompasses two meaningfully different customer behaviours in South African financial services, and a well-designed model treats them separately because the signals, timing, and interventions differ.

Voluntary churn is the deliberate decision to leave: a customer closes their current account, cancels their vehicle finance, or phones a broker to move their short-term insurance policy to a competitor. The decision is active, considered, and typically preceded by a comparison period during which the customer has already begun engaging with alternatives. In banking, digital footprints of this comparison period appear weeks before the formal closure request. In insurance, the comparison often happens at renewal, which creates a predictable timing window for intervention.

Passive lapse is the gradual exit: a customer stops paying their premium, misses a debit order, and the policy lapses without an active cancellation. In life and funeral insurance, passive lapse is often driven by household financial stress rather than dissatisfaction with the product. The customer may want to keep the policy but cannot afford the premium in a given month, and the lapse becomes permanent because the institution’s response is a collections contact rather than a restructuring conversation. A churn prediction model that conflates passive lapse with voluntary exit will route financially stressed customers to competitive retention offers that miss the actual problem, and route voluntary exit candidates to payment holiday offers that fail to address their real objection.

The overlap between passive lapse and collections is where South African insurers and banks lose the most recoverable customer value. A customer who lapses because of a one-month affordability crisis is categorically different from a customer who has made a deliberate exit decision. AI churn prediction models that distinguish between the two enable the institution to apply the right intervention: a payment plan offer for the financially stressed customer who wants to stay, and a retention offer addressing price or product fit for the customer who is actively comparing alternatives.

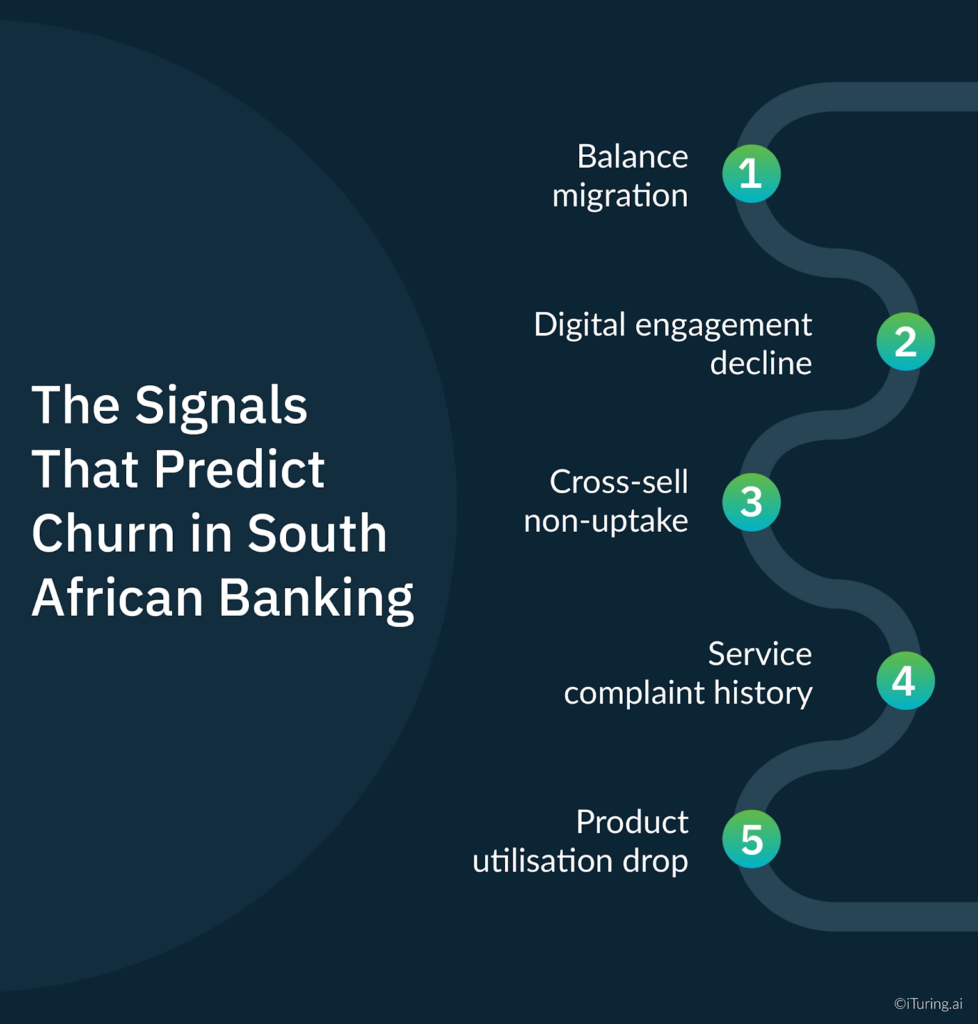

The Signals That Predict Churn in South African Banking

Customer churn prediction in the South African banking context operates on a signal architecture that differs structurally from North American or European equivalents. The South African consumer’s relationship with multiple banking institutions, the prevalence of salary-account-linked credit products, and the specific transactional patterns of the South African credit cycle create a predictive environment requiring models trained and calibrated on South African data.

Balance migration. South African consumers frequently hold accounts at two or more banks simultaneously, using one as a salary account and another for discretionary spending or savings. When a customer begins migrating salary inflows from the primary relationship bank to a secondary bank, this is one of the strongest single-feature predictors of imminent account closure. The signal typically appears 6 to 10 weeks before the formal closure request and has a high predictive Gini coefficient in out-of-time validation samples.

Digital engagement decline. A customer who stops logging into the mobile banking app, stops using the bank’s USSD channel, and stops responding to push notifications is disengaging from the relationship before they disengage from the product. Digital engagement decline as a churn predictor works because it captures the customer’s psychological exit before the administrative exit. In South African mobile banking, where active app users show 40 to 60 percent lower churn rates than passive users, engagement decline has strong signal value.

Cross-sell non-uptake. A customer who has held a cheque account for three years, has a credit profile that would qualify them for a personal loan or vehicle finance, and has declined or ignored multiple cross-sell offers is signalling that the relationship has reached its ceiling from the customer’s perspective. Combined with engagement decline, cross-sell non-uptake is a high-confidence churn signal for customers in the growth segment.

Service complaint history. A customer who has logged a complaint and received either no resolution or a resolution they rated poorly is 3.5 to 4 times more likely to churn within the next 90 days than a customer with no complaint history. The signal is compounded when the complaint was about a product or fee rather than a transactional error: product dissatisfaction complaints have longer decision cycles but higher churn completion rates.

Product utilisation drop. A current account holder who stops using their overdraft facility, a credit card holder whose spend drops below 20 percent of their credit limit, or a home loan customer whose payment pattern shifts from scheduled debit to manual payment is showing reduced product engagement that predicts exit.

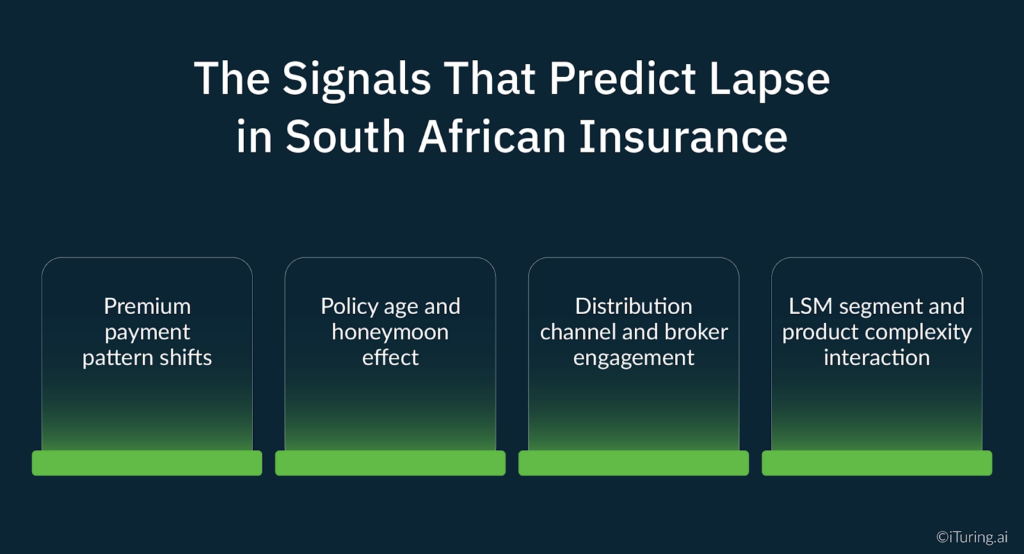

The Signals That Predict Lapse in South African Insurance

Insurance lapse prediction in South Africa operates on a signal set shaped by the country’s specific distribution architecture, product mix, and consumer financial behaviour. Four signals are particularly predictive in the South African insurance context.

Premium payment pattern shifts. A policyholder who consistently pays their premium on debit order on the first of the month but begins missing the first debit and paying late in the grace period is showing a cash flow constraint signal. If the late payment pattern persists for two consecutive months, the lapse probability rises sharply. The Kearney analysis of African insurance in 2025 identifies premium affordability pressure as the primary driver of lapse across the continent’s emerging market segments.

Policy age and honeymoon effect. Lapse probability is highest in the first 12 to 18 months of a policy’s life, a pattern well-documented in South African life insurance actuarial data. The KPMG South African Insurance Industry Survey 2025 identifies acquisition cost recovery as a critical profitability challenge precisely because policies that lapse in the first year typically generate negative economic value for the insurer. AI lapse prediction models that identify at-risk policies in the first 6 months of life allow targeted retention interventions before the acquisition cost is lost entirely.

Distribution channel and broker engagement. South Africa’s short-term and life insurance markets are heavily intermediated through independent brokers and tied agents. When a broker relationship deteriorates, whether through advisor churn, portfolio consolidation, or competitive pressure from a rival insurer offering better commission structures, the policies placed through that broker become systematically more lapse-prone. AI models that include broker engagement signals as input features can identify portfolios at structural risk before individual policy-level signals appear.

LSM segment and product complexity interaction. The lapse dynamics of a funeral policy held by a consumer in the lower Living Standards Measure segments differ from those of a comprehensive life cover policy held in the middle market. Lower LSM segments show higher premium shock sensitivity: a 10 to 15 percent premium increase at renewal is sufficient to trigger lapse consideration in a household where the premium represents a meaningful share of monthly discretionary income. Customer segmentation models calibrated for specific LSM segments, rather than a uniform portfolio model, produce significantly better lapse prediction accuracy by capturing the distinct affordability thresholds, product relationships, and intervention responsiveness that vary materially across South Africa’s income distribution. AI lapse models that draw on these customer segmentation models as their structural foundation outperform segment-agnostic approaches in both predictive Gini and out-of-time validation performance.

The Churn-Collections Overlap: The Most Expensive Mistake in SA Financial Services

The relationship between churn prediction and collections strategy is the most commercially consequential and least discussed aspect of AI retention in South African banking and insurance. Deploying these capabilities in separate organisational silos, without predictive analytics software that connects the two models at the account level, is what produces the most avoidable customer losses in the South African market.

When a customer enters financial stress, two things happen simultaneously. Their payment behaviour begins to show the signals that a collections AI model reads as early-stage delinquency risk. And their satisfaction with the institution begins to decline in a way that a churn model reads as early-stage exit risk. The customer is simultaneously becoming a collections case and a churn risk.

If the institution’s response is determined solely by the collections model, the customer receives escalating contact intensity, automated reminders, and a recovery-framed communication sequence. For a customer who is experiencing temporary financial stress but has no intention of defaulting permanently, this response is relationship-damaging. Customers subjected to aggressive collections contact during temporary financial stress show churn rates 4 times higher than customers who received a supportive intervention during the same stress event.

The AI-enabled alternative requires that the churn model and the collections model are connected at the account level. When an account simultaneously shows early payment stress signals and high churn propensity, the routing logic must prioritise the retention pathway: a proactive outreach offering a payment holiday, a restructured payment plan, or a reduced cover option, before the account enters the standard collections workflow. The commercial outcome is a customer retained and a default prevented, both with a single intervention that costs a fraction of what a full collections cycle and a new customer acquisition would together require.

South African banks and insurers that have integrated churn prediction with collections routing have documented the effect in their retention metrics. The 29 percent reduction in lapse and churn achieved in AI-driven deployments reflects precisely this integration: accounts that would have lapsed through passive exit or been lost through post-collections attrition are identified before the bifurcation point and routed to the appropriate intervention.

TCF and Churn Prediction: The Regulatory Dimension

Two TCF outcomes directly govern how South African institutions must handle customers in the at-risk zone.

TCF Outcome 3 requires that customers are provided with clear information and kept appropriately informed before, during, and after the point of sale. For a customer who is approaching lapse because of premium affordability pressure, TCF Outcome 3 creates a positive obligation to communicate about available options proactively. A customer who lapses because they were not informed that a reduced premium option or a payment holiday existed has been failed under TCF Outcome 3 regardless of whether they technically had the right to request those options.

TCF Outcome 6 requires that customers do not face unreasonable post-sale barriers to changing products, switching providers, submitting a claim, or making a complaint. The ENSAfrica analysis of the Conduct Standard for Banks interprets this outcome as creating a proactive obligation: banks must disclose the implications of maintaining a dormant financial product as opposed to closing or terminating it, and must assist customers in doing what they request. For insurance, an equivalent obligation applies to policyholders who are in the grace period: the institution must ensure the customer understands their options, and a collections-framed communication sequence does not satisfy that obligation.

AI churn prediction enables TCF compliance in both dimensions. A model that identifies customers approaching voluntary exit before they leave creates the opportunity for proactive, TCF-compliant information provision. A model that identifies passive lapse risk creates the opportunity for a payment options conversation before the grace period expires. The CGAP analysis of customer outcomes measurement in South African TCF implementation identifies proactive at-risk customer intervention as one of the most effective mechanisms for demonstrating measurable TCF outcomes to the FSCA.

How iTuring Addresses This

iTuring’s growth and retention module is purpose-built predictive analytics software for the specific churn and lapse dynamics of South African banking and insurance, not a generic retention platform adapted for the South African market.

The churn prediction model ingests transactional engagement, payment behaviour, product utilisation, complaint history, and broker engagement signals, calibrated for the South African credit market and LSM segment distribution. Separate model components address voluntary churn and passive lapse, with different intervention routing logic for each: competitive retention interventions for voluntary exit risk, and payment restructuring workflows for lapse risk driven by financial stress. Customer segmentation models structured around South African LSM tiers and product segments underpin the lapse prediction architecture, ensuring that intervention thresholds, communication content, and escalation logic reflect the actual affordability and behaviour patterns of each segment rather than a uniform portfolio assumption.

The churn-collections integration layer connects the retention module with the collections AI workflow at the account level. When an account simultaneously shows early payment stress and high churn propensity, the routing logic prioritises the retention pathway before the collections workflow escalates. The 29 percent reduction in lapse and churn documented in iTuring deployments reflects this integration operating across the full portfolio.

TCF Outcome 3 and Outcome 6 compliance documentation is maintained automatically: the system records every at-risk customer identification event, the intervention offered, the communication content, and the outcome, creating an examination-ready evidence trail for FSCA review.

Regulatory Disclaimer

This article is for informational purposes only and does not constitute legal or compliance advice. FSCA TCF Outcomes, the Conduct Standard for Banks, and related regulatory obligations are subject to change and ongoing supervisory development, including through the COFI Bill once enacted. Lapse and churn statistics cited reflect industry data and iTuring deployment results as of the publication date and may not reflect current market conditions. Consult qualified South African legal and compliance professionals for guidance specific to your institution.

Sources: MoneyMarketing: State of African Insurance 2025 | KPMG: South African Insurance Industry Survey 2025 | Kearney: State of African Insurance 2025 | CustomerGauge: Average Churn Rate by Industry 2025 | Shopify: Average Customer Retention Rates 2025 | InsurNest: Churn Prediction AI Agent Insurance | Insurance Transformation Africa: SA Insurance Challenges 2025 | ENSAfrica: Conduct Standard for Banks and TCF | CGAP: Customer Outcomes TCF South Africa | National Treasury: TCF Market Conduct Policy Framework SA