Key Takeaways

- Banks identifying at-risk accounts 90-120 days before default achieve 39-44% higher collection rates while cutting contact costs 48%

- Four Collections Prevention Pathways exist: Behavioral Guardrails (automated AI), Proactive Partnership (AI + personal outreach), Reactive Alerts (legacy systems), and Crisis Recovery (traditional agencies)

- Deployment timeline compressed from 2-3 months to 2-4 weeks using AI monitoring 25,000+ signals across payment patterns and account activity

- A housing finance company managing a $21 billion portfolio achieved 83% prediction accuracy and 39-44% collection improvements across delinquency buckets

- Implementation requires automated feature engineering processing 1,500 delinquency behaviors and 400 payment patterns from raw transaction data

Most banks wait until accounts hit 30, 60, or 90 days past due before taking action on collections. This reactive approach costs them dearly in both recovery rates and operational efficiency.

There’s a better way. Banks using predictive AI to identify at-risk accounts 90-120 days before they default achieve 39-44% higher collection rates while cutting contact costs by 48%.

After analyzing banking use cases, we’ve identified four distinct approaches to collections optimization. We call them Collections Prevention Pathways. They differ in two key ways: when you identify risk and how you respond. These two factors determine whether banks minimize losses or absorb preventable defaults.

Why Prevention Beats Recovery

Traditional collections follow a simple pattern: wait for the account to go delinquent at 30, 60, or 90 days, then escalate. The problem is that behavioral signals appear weeks earlier. Declining transaction volumes, changing payment patterns, reduced account engagement—these signals predict delinquency with high accuracy when captured systematically.

Waiting to act costs real money. A housing finance company managing a $21 billion loan book with 266,000 customers demonstrated this clearly. When they intervened at accounts 0-30 days past due using behavioral predictions, they improved collection rates by 39%. For accounts in the 60-90 day bucket, they needed 44% more effort to achieve recovery.

The shift is fundamental. Banks are moving from recovery to prevention. Those deploying predictive AI that captures behavioral signals 90-120 days before delinquency reduce operational costs substantially while improving collection outcomes.

The Four Collections Prevention Pathways

Every financial institution operates somewhere on a spectrum defined by two dimensions. The first is prediction horizon when you identify risk. The second is intervention intensity how you respond. Together these create four distinct approaches.

Pathway 1: Behavioral Guardrails

This approach uses AI agents to monitor accounts 90-120 days before delinquency. When risk appears, the system triggers automated, low-cost interventions to prevent default at scale.

This pathway works best for high-volume portfolios: credit card accounts, auto loans, personal lending, digital-first banks. Any situation where you need to monitor thousands or millions of accounts efficiently.

Technical Requirements:

- Real-time Feature Store processing 25,000+ behavioral signals

- Predictive models watching payment patterns, transaction velocity, and account activity trends

- Automated decisioning engine delivering personalized nudges, payment date adjustments, and self-service restructuring options

Case Study: Housing Finance Company

A housing finance company managing a $21 billion portfolio with 266,000 customers implemented this approach across all delinquency stages from 0-90 days. The results were substantial:

- Collection efficiency improved 39% for accounts 0-30 days past due

- Collection efficiency improved 44% for accounts 60-90 days past due

- Customer contact costs dropped 48% through optimized digital outreach

- Overall operational efficiency increased 80% through automation

The platform processed 1,500 delinquency behavior features and 400 payment pattern features from raw payment data. It identified patterns that traditional scoring completely missed. The models achieved 83% accuracy identifying the highest-risk 30% of accounts 120 days before delinquency.

From data integration to production deployment took just 2-4 weeks.

Pathway 2: Proactive Partnership

This pathway combines early predictive risk identification with personalized relationship manager outreach. It makes sense for high-value accounts where relationship preservation matters.

Commercial banking, mortgage portfolios, private banking, and wealth management are natural fits. These relationships have too much value to handle with automated nudges alone.

Technical Requirements:

- Predictive models identifying at-risk accounts with high accuracy

- CRM workflow integration triggering relationship manager alerts

- Behavioral segmentation analyzing payment behavior, intent, and customer preferences

Implementation Example:

The housing finance company used this hybrid approach for their mortgage portfolio. The iTuring platform scored accounts by default probability and payment psychology. The system tracked three delinquency buckets: 0-30, 30-60, and 60-90 days. This enabled customized contact strategies for each segment.

Behavioral segmentation distinguished three customer types:

- Temporary liquidity stress (automated digital nudges)

- Structural payment changes (relationship manager outreach)

- Intentional avoidance (firm collection tactics)

This approach works because personal intervention matters for complex products like mortgages and business loans. It preserves relationship value while AI prioritization ensures efficiency. Traditional approaches contact all delinquent accounts equally, diluting impact.

Pathway 3: Reactive Alerts

This is the status quo for many regional banks running legacy systems. Basic early warning systems trigger at 15-30 days past due with generic automated messaging.

Technical Requirements:

- Rule-based alerting from core banking system

- Generic email and SMS templates

- Minimal AI sophistication

Limitations:

Legacy systems often lack real-time model performance monitoring, capturing only 30-40% of preventable delinquencies because they miss behavioral signals visible 60-90 days earlier. These systems trigger when delinquency occurs rather than predicting it beforehand.

Banks in this pathway experience significantly higher losses than those using Pathways 1-2. The opportunity cost compounds across the portfolio as preventable delinquencies progress to charge-offs.

Pathway 4: Crisis Recovery

This is traditional collections escalation after 90+ days delinquent, often involving third-party agencies or legal action. Every institution uses this as a last resort for charge-off prevention.

Performance Characteristics:

- Recovery rates substantially lower than early intervention

- High cost per account through agency fees and legal expenses

- Most accounts never return to good standing

- Highest compliance risk due to FCRA, ECOA, and CFPB scrutiny

The strategic imperative is clear: minimize the volume flowing to Pathway 4 by maximizing the effectiveness of Pathways 1 and 2.

How to Choose Your Pathway

The right choice depends on your institution type and portfolio characteristics.

Retail banks with $5-50 billion in assets should deploy Pathway 1 for credit card and auto loan portfolios with high account volumes. The iTuring Feature Store processes 8,000 transaction pattern features, 5,000 spend pattern features, and 7,000 bureau-derived signals from raw banking data. This enables real-time risk scoring.

After proving Pathway 1 value, transition mortgage portfolios to Pathway 2, leveraging relationship managers for high-value accounts.

Digital lenders require Pathway 1 for survival. With no branch relationships, automated behavioral interventions are the only prevention mechanism. The system must identify at-risk accounts through transaction patterns, payment behaviors, and engagement metrics before delinquency occurs.

Commercial banks should use Pathway 2 for business lending portfolios. Combine predictive cash flow stress signals with relationship manager outreach 90 days early. The housing finance company demonstrated that behavioral segmentation enables customized interventions matched to customer payment psychology rather than uniform approaches.

Regional banks with less than $5 billion in assets can start with a rules-based version of Pathway 1 for consumer portfolios. Basic behavioral triggers like account activity decline, payment pattern changes, and balance migration capture substantial value at lower complexity.

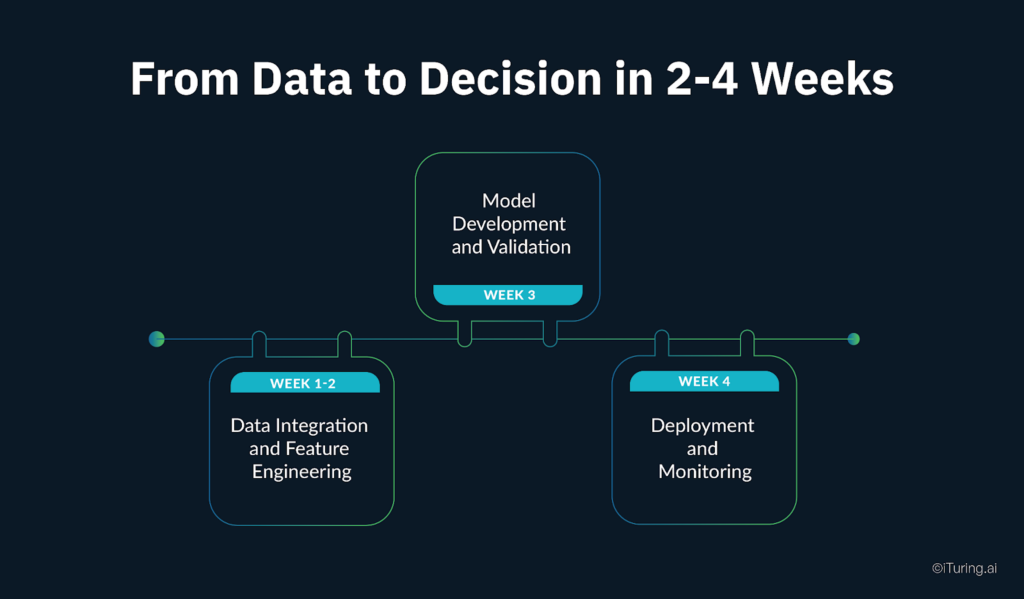

From Data to Decision in 2-4 Weeks

Traditional collections model development requires 2-3 months with multidisciplinary teams of domain experts, data scientists, and DevOps engineers. The iTuring architecture compresses this timeline dramatically.

Weeks 1-2: Data Integration and Feature Engineering

The platform connects core banking, loan management systems, CRM, and bureau data through pre-built APIs. Automated feature derivation creates:

- 1,500 delinquency behavior features

- 400 payment pattern features

- 7,000 bureau-derived signals

- 8,000 transaction pattern features

The system generates Feature-as-a-Service APIs for real-time scoring with sub-100 millisecond latency.

Week 3: Model Development and Validation

The platform uses 4,000 AI agents to build thousands of models in 2-8 hours. Automated evaluation selects champion and challenger models. Explainable AI ensures regulatory compliance with FCRA, ECOA, and CFPB requirements through SHAP values, LIME explanations, and feature importance rankings.

Week 4: Deployment and Monitoring

Real-time and batch scoring deploy through microservices containers. Early Warning Indicators track 60+ model performance parameters continuously. The self-learning system handles auto-retraining when performance degrades.

The housing finance company completed this entire cycle in 2-4 weeks. When the system detected a 10% accuracy decline in their 0-30 day bucket model, automated monitoring flagged the drift and triggered retraining within hours.

The Real Cost of Waiting

The economics of early intervention versus reactive collections are stark. Consider the housing finance company’s results:

The difference compounds across portfolios. Early behavioral signals appear 90-120 days before delinquency. Each week of delay reduces recovery probability while increasing intervention costs. By the time accounts reach 90+ days past due, most recovery options involve expensive third-party agencies with substantially lower success rates.

Building Regulatory Confidence

Collections AI operates under intense regulatory scrutiny. The Fair Credit Reporting Act, Equal Credit Opportunity Act, and CFPB oversight all apply. The iTuring platform addresses model risk management requirements through several mechanisms:

SR 11-7 Compliance:

- Automated documentation generates immutable audit trails of model development, validation, and deployment with a single click

- Complete model inventory with version control and approval workflows

- Comprehensive governance covering model lifecycle from development through monitoring

Explainable AI:

- SHAP values and LIME explanations provide both global and local model interpretability

- Feature importance rankings show what drives predictions

- Neuro Signal Tracing provides exact explanations for neural network decisions

Continuous Monitoring:

- 60+ parameters tracked in real-time including data drift, feature drift, and algorithm performance

- Early warnings appear 2-4 weeks before model failures

- Automated bias detection across protected classes prevents discriminatory patterns before deployment

A payment bank required model explainability for merchant churn prediction. iTuring delivered 92% accuracy compared to the 80% incumbent model with full interpretability in 40 minutes. This enabled regulatory approval and deployment.

The Strategic Choice

The collections function in banking is splitting into two groups. Proactive institutions use Pathways 1 and 2, identifying risk 90-120 days early and intervening before delinquency occurs. Reactive institutions stick with Pathways 3 and 4, waiting for delinquency to happen then escalating through expensive recovery processes.

The fundamental dimensions of prediction horizon and intervention intensity determine which banks minimize losses. Institutions shifting from Pathways 3-4 to Pathways 1-2 achieve 39-44% better collection outcomes with 48-80% operational cost reductions.

The housing finance company’s results demonstrate the economics clearly:

- $21 billion portfolio with 266,000 customers

- 83% accuracy predicting highest-risk 30% of accounts 120 days before delinquency

- 39% collection improvement for 0-30 day bucket

- 44% improvement for 60-90 day bucket

- 48% reduction in contact costs

- 2-4 week implementation timeline

Collections strategy is not an operational detail. It is a strategic choice determining profitability, customer lifetime value, and competitive positioning.

Start Your Collections Optimization Journey

The iTuring Collections Prevention platform enables Pathway 1 deployment in 2-4 weeks across banking use cases. The system processes 25,000+ behavioral signals through automated feature engineering, builds predictive models achieving 83%+ accuracy using 4,000 competing AI agents, and monitors performance continuously across 60+ parameters.

Documented performance improvements exist for institutions managing portfolios from $5 billion to $21 billion. The platform supports both automated Behavioral Guardrails (Pathway 1) and hybrid Proactive Partnership approaches (Pathway 2), with complete regulatory compliance through SR 11-7 documentation and continuous bias monitoring.