Key Takeaways

- Prevention costs significantly less than recovery operations per customer

- Behavioral signals predict delinquency 90-120 days before credit bureaus

- Autonomous agents process portfolios at scale automatically

- Reinforcement learning improves prevention effectiveness 5-15% per quarter

- Prevention saves 6-8x versus reactive collections economics

Your collections team recovered 44% more debt this quarter. Congratulations. You also proved your bank failed at prevention.

For Chief Risk Officers this collection paradox reveals fundamental misalignment in how banks measure success. Every dollar spent on collections costs six to eight dollars more than preventing the delinquency in the first place. Yet banks celebrate reactive recovery while ignoring systemic prevention failure.

The economics of a modern banking AI platform are unambiguous. Prevention interventions cost substantially less through automated digital channels. Analysis of large loan portfolios shows recovery operations cost significantly more per customer through phone agents, field visits, and legal proceedings. The cost differential makes prevention economics overwhelming.

Three mechanisms create this advantage. First, behavioral signals predict delinquency 90-120 days before credit bureau data flags risk, opening intervention windows when customer relationships remain intact and recovery probability peaks at 70-80%. Second, autonomous agents orchestrate prevention workflows processing entire portfolios automatically versus thousands of analyst hours required for manual processing. Third, reinforcement learning improves prevention effectiveness 5-15% quarterly without manual retraining, compounding advantages over time.

A housing finance company managing a $21 billion portfolio proved all three. Their behavioral AI identified at-risk customers 120 days before delinquency with 83% accuracy, improved collections efficiency 39-44% across buckets, and reduced operational costs through optimized digital outreach. Prevention-stage interventions through automated channels replaced costly recovery-stage collections operations.

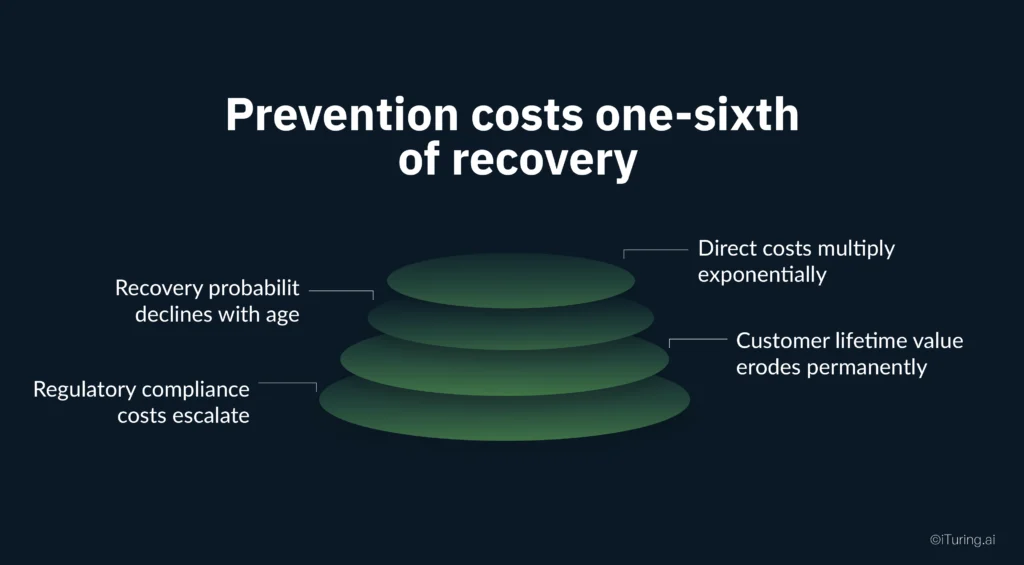

Prevention costs one-sixth of recovery

Four cost categories compound as delinquency ages, creating the 6-8x differential favoring prevention.

Direct costs multiply exponentially. Early intervention through automated SMS, email, or app notifications costs $0.50-2.00 per customer including system overhead and message generation. Late-stage recovery requires phone agents at $8-15 per contact or field visits at $250-400 per customer. Legal proceedings add $2,000-5,000 for attorney fees and court costs. The housing finance company demonstrated this arbitrage: automated digital outreach to customers showing payment pattern shifts 90 days before delinquency cost 48% less than traditional collections while preventing 83% of predicted defaults.

Recovery probability declines with age. Customers 30 days past due respond at 70-80% rates. At 90 days, response drops to 40% after they’ve committed available cash elsewhere. Beyond 180 days, recovery probability falls to 20%. Prevention at day zero with 80% success costs $0.50. Recovery at day 90 with 40% success costs $50-100—creating 100-320x worse economics through both lower probability and higher cost.

Customer lifetime value erodes permanently. Collections tactics damage relationships in ways prevention does not. Customers subjected to aggressive collections show 4x higher churn rates. The lifetime value difference reaches $1,200-1,800 per customer. Prevention-stage outreach preserves relationships because customers haven’t missed payments yet and view the bank as supportive, not adversarial.

Regulatory compliance costs escalate. FDCPA requirements add 20-40% overhead to collections through timing restrictions, disclosure mandates, and documentation. Prevention-stage interventions operate outside these frameworks because no debt collection is occurring, reducing compliance overhead 80-90%.

Banks miss the 90-120 day window

Credit bureau data lags behavioral reality by 30-90 days. Behavioral signals appear immediately through transaction patterns, creating intervention windows reactive systems never access.

Three signal categories predict first. Payment pattern drift measures shifts in how customers pay bills. A customer switching from full balance payments to minimums shows financial stress 60-90 days before missed payments. The iTuring Feature Store derives hundreds of payment pattern features from raw transaction data tracking velocity, momentum, and timing shifts. Quantitatively, payment velocity decline of 15% over 60 days correlates with 3.2x higher delinquency probability in the subsequent 90 days.

Engagement decline measures relationship weakening through digital channel usage and product utilization. Balance management changes reveal liquidity stress. A checking account declining from $8,000 to $2,000 over six months while income remains stable signals financial pressure. These metrics predict payment problems before credit scores reflect issues.

Prediction accuracy reaches 78-93%. The iTuring platform processes 25,000+ pre-computed features from transaction data, payment history, engagement metrics, and demographics to achieve high prediction accuracy. Behavioral models capture signals invisible to traditional credit underwriting: application completion patterns, interaction velocity, and digital engagement trends that predict payment behavior.

The housing finance company achieved 83% accuracy predicting which customers would hit delinquency 120 days forward. This enabled focusing prevention efforts on the highest-risk 30% of customers before delinquency occurred.

Early detection multiplies intervention options. At 120 days before delinquency, customers respond to supportive digital outreach at 40-50% rates. Messages offer payment flexibility, financial counseling, or payment plan adjustments. Response rates reach these levels because customers have not missed payments yet and perceive the bank as helpful.

At 60 days before delinquency, digital-only approaches drop to 25-30% effectiveness requiring phone agent follow-up. At delinquency, response rates fall to 20-30% and intervention costs spike substantially. The economic comparison quantifies the window value: preventing one delinquency at 120 days pre-delinquency costs minimal expected cost. Recovering at 90 days past due costs exponentially more in expected cost.

Agents outperform rules through four mechanisms

Rules-based collections systems fail prevention because they cannot handle complexity, adapt to changes, learn from outcomes, or scale economically.

Autonomous orchestration manages 10,000+ variable interactions. Traditional rules handle 10-50 decision variables before becoming unmanageable. Adding customer segments, delinquency buckets, contact history, payment patterns, engagement levels, and seasonal factors creates 10,800+ combinations requiring manual rules. Building rules for this complexity becomes impossible.

The iTuring platform orchestrates 23+ self-learning AI agents handling collections workflows across unlimited variable combinations. Feature agents process 25,000+ features from transaction data, payment history, engagement metrics, and demographics simultaneously. Decision agents classify customers into behavioral segments, score default risk, rank accounts by priority, and generate personalized recommendations. Communication agents craft messages tailored to individual payment psychology analyzing prior response patterns for optimal tone, channel, and timing.

These agents process entire portfolios continuously without human intervention. The system handles portfolios at scale through automated workflows. Manual processing requires 10-15 minutes per customer, consuming thousands of analyst hours for large volumes.

Reinforcement learning eliminates manual tuning. Rules-based systems require 8-12 week update cycles when performance degrades. Analysts investigate root causes, propose changes, develop new rules, test on samples, refine, and deploy updates.

Agentic AI optimizes continuously through reinforcement learning. The iTuring platform designs reward signals aligned with business objectives: payment maintained (high reward), payment modified but maintained (medium reward), payment missed with extended delinquency (negative reward). Self-learning AI agents identify optimal interventions. For example, agents identifying a high-balance customer prevent churn by offering a tenure-based waiver instead of a standard demand.

The platform reduces false positive alerts by 70% through adaptive threshold tuning. Static thresholds trigger alerts when metrics breach fixed levels generating false positives because customer behavior varies by segment. Reinforcement learning adapts thresholds by segment based on actual outcomes. For high-balance customers, the system learns 30% balance decline predicts delinquency while 15% does not. For low-balance customers, 15% decline proves significant.

Closed loops compound improvement. Collection outcomes feed back into predictive models updating risk scores in real-time. Response patterns train the generative layer crafting messages. Recovery results refine agent workflows. The system achieves 5-15% accuracy improvement per quarter. The housing finance company demonstrated continuous improvement through closed-loop learning.

Economic scaling advantages. Rules-based systems scale linearly with portfolio size requiring 10X analyst hours for 10X accounts. Agentic systems scale sublinearly. The iTuring platform handles unlimited concurrent execution with identical infrastructure costs regardless of portfolio size. Marginal cost per additional account approaches zero.

Build this, measure that

Prevention ROI proves itself through phased deployment and controlled measurement.

Begin with the 0-30 day bucket. This segment offers the strongest cost arbitrage ($0.50-2.00 prevention versus $15-100 recovery), highest recovery probability (80% versus 40% at 90 days), and minimal relationship damage. The strategy: build models scoring payment propensity 90-120 days before customers enter the bucket, then deploy automated digital-first interventions for high-risk segments.

Validate through controlled experiments. Divide portfolios into control groups receiving standard treatment and test groups receiving prevention interventions. Measure delinquency rates, collection costs, and customer retention across both cohorts. This approach quantifies true prevention value including direct cost savings, opportunity cost avoidance, customer lifetime value preservation, and compliance burden reduction.

Monitor leading indicators continuously. Track early warning trigger rates, intervention response rates, and payment behavior improvements post-intervention. These metrics signal prevention effectiveness before delinquency rates decline, enabling real-time strategy refinement.

Maintain regulatory readiness. Generate automated documentation showing model development rationale, validation results, explainability, fairness testing, and continuous monitoring. The iTuring platform provides immutable audit trails and one-click documentation satisfying SR 11-7 model risk management requirements. Track 60+ parameters continuously with early warnings 2-4 weeks before failures.

Resolution

The collections paradox resolves when banks recognize that reactive excellence proves prevention failure.

Prevention saves six to eight dollars for every dollar spent on recovery. Behavioral signals predict delinquency 90-120 days before credit bureau data enables intervention when relationships remain intact and costs minimize. Autonomous agents orchestrate prevention at scale processing portfolios automatically versus thousands of analyst hours for manual workflows. Reinforcement learning compounds advantages improving effectiveness 5-15% quarterly.

The housing finance company proved the economics: 39-44% collections efficiency improvements while reducing operational costs through prevention-first operations on a $21 billion portfolio. Their behavioral AI achieved 83% prediction accuracy identifying at-risk customers 120 days before delinquency.

Banks celebrating collections improvements are measuring the wrong outcome. Every recovered dollar proves a prevention failure. Prevention excellence means delinquency never happens, recovery never becomes necessary.