TL;DR

- India’s gross NPA ratio hit a multi-decade low of 2.1% in late 2025

- AI-powered NPA recovery software is fundamentally different from a collections CRM

- Four capabilities define fit for the Indian market: propensity scoring, SARFAESI integration, RBI compliance, and vernacular communication

- NBFCs face distinct recovery dynamics under Scale Based Regulation

- The next NPA reduction cycle will require tools the previous one did not

India’s banking sector just achieved something remarkable. The gross NPA ratio of scheduled commercial banks fell to 2.1 percent by end-September 2025, a level not seen in decades. Public sector banks, which have carried the heaviest NPA burden since the 2015-16 stress cycle, reduced their ratio to 2.6 percent in FY25 from 3.5 percent the year before. By any measure, the improvement has been significant.

But here is the challenge that number conceals. The NPA reduction that got India here was driven by a combination of IBC proceedings clearing large corporate accounts, asset reconstruction company activity on legacy wholesale stress, and aggressive write-off programs. The stock of distressed retail and MSME debt that remains is structurally more complex. CRISIL projects gross NPAs will stabilise at 2.3 to 2.5 percent by March 2026 as MSME and microfinance stress builds. The RBI’s Financial Stability Report has flagged that NBFCs’ gross NPA ratio could rise to 5.8 percent under severe stress scenarios.

The tools that drove the first phase of NPA recovery like legal resolution processes, bulk settlement programs, and write-off accounting, will not drive the next one. The next phase requires something different: the ability to recover retail and MSME accounts at scale, earlier in the delinquency cycle, at a cost structure that makes individual account-level intervention economically viable. That is what AI-powered NPA recovery software is built to deliver.

What NPA Recovery Software Actually Does

The term “NPA recovery software” covers a wide range of tools, and the range matters enormously when you are evaluating options for a mid-size bank or NBFC portfolio.

At the basic end, a collections CRM with NPA tagging functionality lets your team track accounts, log contacts, and generate reports. It organises the workflow. It does not change the economics of the workflow.

AI-powered NPA recovery software does something fundamentally different. At its core is a propensity model that predicts which accounts are most likely to self-cure if contacted now, through which channel, with which message, and at what time. It prioritises your agent capacity toward the accounts where contact will have the highest impact. It automates outreach on lower-priority accounts through digital channels that cost a fraction of a phone call. And it learns from every interaction, continuously updating its predictions based on what is actually working in your specific portfolio.

It is also worth distinguishing NPA recovery AI from a churn prediction model. A churn prediction model forecasts voluntary disengagement, a customer closing an account or switching to another provider. NPA recovery software targets an involuntary behaviour: payment failure driven by financial stress. The signals, intervention logic, regulatory obligations, and remediation actions are fundamentally different for each, and a platform designed for one does not transfer to the other.

The practical consequence of this difference is measurable at the P&L level. A traditional collections workflow allocates agent time roughly proportionally across the DPD book: 1 to 30 DPD gets light contact, 31 to 90 gets moderate contact, 90+ gets intensive contact. An AI-driven workflow allocates agent time according to payment propensity, which often means working hardest on accounts that are 7 to 25 DPD with strong self-cure signals, and using automated digital channels for accounts at all stages where the model predicts low responsiveness to agent contact. The result is the same or better recovery at substantially lower cost per rupee collected.

The Four Capabilities That Define Fit for Indian Banks and NBFCs

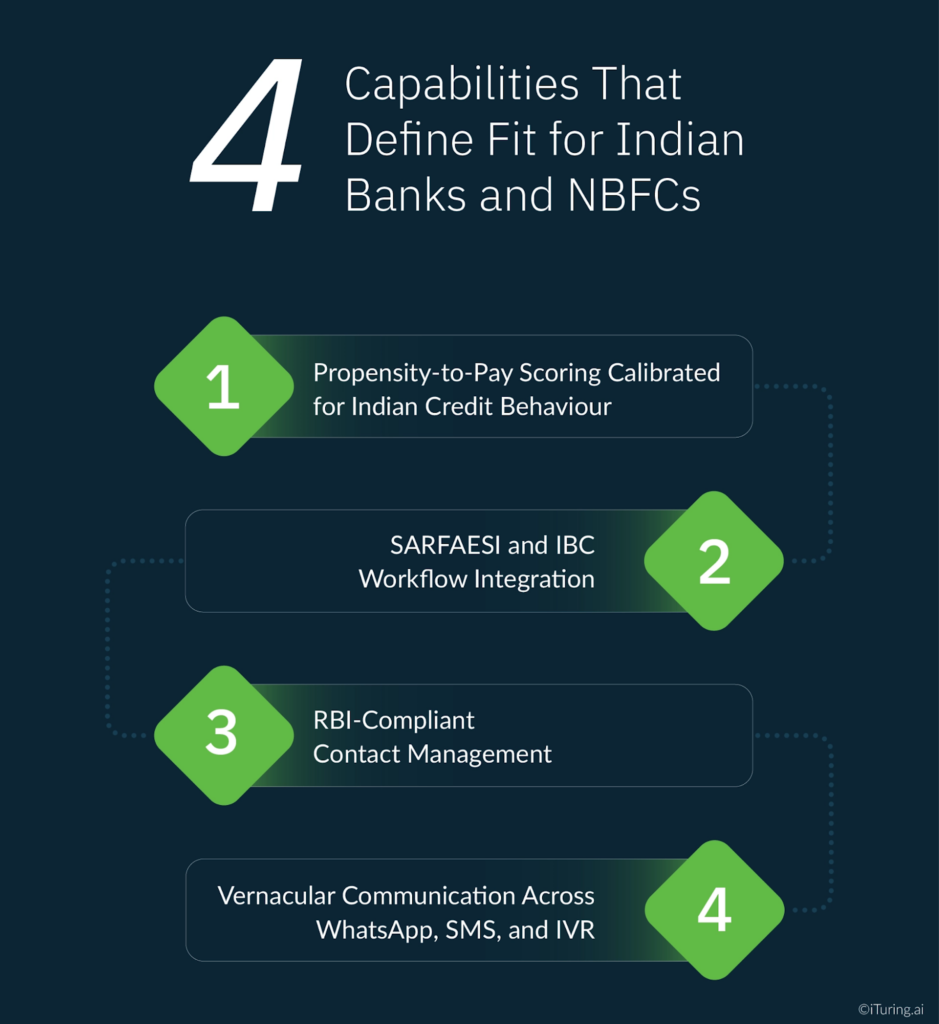

Global collections platforms are built for the regulatory and operational environments of their home markets. A platform designed for US FDCPA compliance and Salesforce Financial Services Cloud integration is not the same as a platform built for India. Four specific capabilities determine whether an NPA recovery platform is genuinely fit for the Indian market.

1. Propensity-to-Pay Scoring Calibrated for Indian Credit Behaviour

A propensity model trained on US or European payment behaviour will not perform reliably on an Indian bank or NBFC portfolio. Indian borrower behaviour has distinct characteristics: the prevalence of NACH mandates and their failure patterns, the significance of informal income flows in MSME lending, the seasonality of agricultural loan repayment, and the relationship between UPI payment behaviour and collection outcomes.

Effective NPA recovery software for Indian portfolios must be trained on Indian credit data, calibrated to RBI DPD bucket definitions (the 90-day NPA classification standard), and capable of incorporating bureau data from CIBIL, Experian, CRIF, and Equifax as standard inputs. Underlying this is a credit risk scoring architecture that combines those bureau attributes with dynamic behavioural signals bureau-only models miss, payment velocity trends, informal income proxies, and UPI transaction patterns specific to Indian portfolios. A platform that cannot demonstrate India-trained models with Indian reference clients is not a fit for this market.

2. SARFAESI and IBC Workflow Integration

The SARFAESI Act is the primary legal tool for secured NPA enforcement in India. Once a loan is classified as NPA, the bank issues a Section 13(2) demand notice requiring repayment within 60 days. On failure, Section 13(4) permits enforcement action including seizure and sale of secured assets without court intervention. For retail and MSME NPAs above the applicable thresholds, SARFAESI is often the most efficient recovery path.

NPA recovery software that integrates SARFAESI workflow management does two things. First, it tracks accounts against SARFAESI eligibility criteria and timelines, ensuring the notice issuance, response period, and enforcement steps are managed to the statutory deadlines. Second, it connects propensity scoring to the SARFAESI decision: accounts with strong voluntary payment signals should receive a contact intervention before SARFAESI initiation, because voluntary cure is always cheaper than legal enforcement. AI-driven sequencing of pre-SARFAESI contact and post-notice engagement is one of the highest-impact capabilities in the Indian collections AI toolkit.

For accounts headed toward IBC proceedings, workflow integration means tracking NCLT timelines, coordinating with resolution professionals, and ensuring documentation requirements for the insolvency process are maintained through the collections system.

3. RBI-Compliant Contact Management

The RBI’s Master Direction on Fair Practices Code for Lenders, updated in 2024 and 2025, imposes specific requirements on collections contact conduct. Recovery agents can contact borrowers only between 8 AM and 7 PM. Banks must maintain a board-approved recovery agent engagement policy, published on the bank’s website. The 2025 update introduced mandatory agent training and certification requirements, with specific emphasis on handling distressed borrowers with appropriate sensitivity.

For AI-driven contact systems, RBI compliance means the platform must enforce contact hour restrictions automatically, maintain a complete audit trail of every AI-generated communication, and ensure that AI-driven contact cadence does not generate complaint volumes that invite RBI supervisory attention. A platform without built-in compliance guardrails places the compliance burden on the operations team, which is both operationally fragile and regulatory risk exposure.

4. Vernacular Communication Across WhatsApp, SMS, and IVR

India has over 500 million WhatsApp users. A borrower in Tier 2 Lucknow or Tier 3 Coimbatore is far more likely to open and respond to a WhatsApp message in their own language than to an English-language SMS or a call from an agent reading a script.

The data on this is decisive. WhatsApp messages achieve a 98 percent open rate compared to 8 to 12 percent for SMS. Dual-channel collections using WhatsApp followed by an AI-calling interaction recover 40 percent more than voice-only strategies, at 55 percent lower cost per recovery. Sending a WhatsApp message 2 to 4 hours before an AI voice call increases call answer rates by 35 to 40 percent: the borrower sees the message, registers the intent to discuss, and is primed to answer when the call arrives.

For this to work in the Indian market, the platform must support at minimum Hindi, Tamil, Telugu, Kannada, Marathi, Bengali, and Malayalam, with dynamic language detection that can shift to the borrower’s registered language without agent intervention. Platforms that offer English and Hindi only are not adequate for a national bank or NBFC with geographic distribution.

The NBFC-Specific Challenge

NBFCs and scheduled commercial banks operate within the same broad credit environment, but they face meaningfully different NPA recovery dynamics. Understanding these differences is critical when evaluating NPA recovery software for an NBFC.

The most significant structural difference is SARFAESI eligibility. Since the 2020 notification reduced asset thresholds, NBFCs with total assets of Rs. 100 crore or more can invoke SARFAESI for loans above Rs. 50 lakh. The 2025 notification extended the framework further, bringing RBI-recognised NBFCs under the qualified buyer framework for ARC asset acquisition. However, NBFCs below the Rs. 100 crore asset threshold still cannot use SARFAESI, leaving them reliant on civil recovery suits, Lok Adalats, and arbitration for secured enforcement. This creates a two-speed recovery environment within the NBFC sector.

RBI’s Scale Based Regulation, introduced in 2022, adds another layer of complexity. The framework classifies NBFCs into four layers: Base Layer (NBFC-BL), Middle Layer (NBFC-ML), Upper Layer (NBFC-UL), and Top Layer (reserved for systemic risk cases). Upper Layer NBFCs face bank-equivalent capital and governance requirements, including stricter NPA provisioning norms and closer supervisory engagement with RBI. For NBFC-UL entities, NPA recovery program quality is a direct input into the supervisory assessment. A well-governed, technology-enabled recovery program is not a competitive advantage for an Upper Layer NBFC, it is a regulatory expectation.

Base and Middle Layer NBFCs face a different challenge. They cannot rely on SARFAESI for smaller secured loans, their recovery toolkits lean more heavily on One Time Settlement (OTS), loan restructuring, and negotiated resolution, and their data science capacity is often insufficient to build internal propensity models. For these institutions, a vendor-provided NPA recovery platform is the most practical path to AI-enabled collections, and the evaluation criteria should weight RBI compliance certification, India-specific model training, and low implementation overhead heavily.

Evaluation Criteria: Five Questions That Separate Good Platforms from Generic Ones

1. Can the platform demonstrate RBI compliance certifications and an India-specific audit trail?

The audit trail for every AI-generated communication must be retrievable for RBI examination. If the vendor cannot demonstrate this specifically for Indian regulatory requirements, not generic GDPR or PCI-DSS compliance, the platform presents compliance exposure.

2. Does the platform support your core banking system?

Integration with Finacle, Temenos T24, Nucleus FinnOne, and Flexcube is non-negotiable for a bank or large NBFC. Beyond system connectivity, the integration must support real-time credit risk decisioning so that propensity scores, contact channel selections, and SARFAESI eligibility flags all update dynamically as new payment or bureau data arrives. A platform that requires a bespoke integration project of more than four weeks is carrying hidden implementation cost that the headline licensing fee does not reflect.

3. What are the reference clients, and are they comparable to your portfolio?

A platform with five reference clients who are all large PSBs is not validated for a mid-size NBFC with an MSME-heavy book. Ask specifically for reference clients with similar portfolio composition, asset size, and DPD distribution.

4. Does the platform explain its predictions?

For RBI supervisory purposes, a black-box model that cannot produce account-level explanations for its prioritisation decisions is a governance liability. Propensity scores must be explainable to both internal audit and RBI examiners. SHAP-based explanations at the account level are the current standard.

5. What is the implementation timeline, and what does it include?

A genuine four-to-six week implementation means data integration, model training on your portfolio, compliance testing, and team onboarding are all included. A vendor who quotes four weeks and then separately scopes the integration project is not quoting the real timeline.

Results Indian Banks and NBFCs Can Realistically Expect

AI-powered NPA recovery deployments in the Indian market consistently show improvement across three measurable dimensions.

Collections efficiency across DPD buckets. Propensity-driven prioritisation typically delivers a 39 to 44 percent improvement in collections efficiency across the full DPD book, measured as rupees recovered per agent contact hour. The gains are largest in the 1 to 30 DPD early-stage bucket, where pre-delinquency intervention on high-propensity accounts prevents escalation.

Contact cost reduction. Shifting from agent-led phone contact to AI-orchestrated omnichannel outreach (WhatsApp, AI voice, SMS, in that priority sequence for digital-first borrowers) reduces cost per contact by 55 to 60 percent. For a mid-size bank running 100,000 contacts per month, this represents a material cost reduction that compounds across the recovery cycle.

Pre-delinquency prediction accuracy. Well-trained propensity models on Indian credit portfolios can predict accounts likely to default with 83 percent accuracy at 120 days pre-delinquency. This early warning window is what transforms collections from a reactive process into a genuinely preventive one. And it is the capability that has the most direct impact on preventing NPA formation rather than just managing NPAs after they occur.

How iTuring Addresses This

iTuring’s collections AI platform is built specifically for the Indian bank and NBFC operating environment, not adapted from a global platform.

The platform deploys dual propensity models, default propensity for early intervention and payment propensity for in-delinquency contact strategy, trained on Indian credit data and calibrated to RBI DPD bucket definitions. SARFAESI workflow management is integrated into the collections decisioning engine, so pre-SARFAESI contact interventions are sequenced automatically based on account payment propensity before legal enforcement is triggered.

RBI compliance guardrails are built into every AI-generated contact decision: contact hour enforcement, audit trail generation, and escalation logging are automated. Vernacular communication is supported across ten Indian languages through WhatsApp, AI voice, SMS, and IVR channels, with dynamic language selection based on the borrower’s registered language preference.

For NBFCs, iTuring’s platform is available at implementation timelines calibrated to Base Layer and Middle Layer institution capacity, with no requirement for an internal data science team to manage model governance.

Are you evaluating NPA recovery software for your bank or NBFC? iTuring’s team can walk through a working session on how the platform performs against your specific portfolio composition, DPD distribution, and RBI compliance requirements.

Regulatory Disclaimer

This article is for informational purposes only and does not constitute legal or compliance advice. NPA classification norms, SARFAESI eligibility criteria, and RBI guidelines for recovery agents are subject to change. Information presented reflects publicly available RBI guidance and industry data as of the publication date. Consult qualified legal and compliance professionals for guidance specific to your institution’s circumstances.

Sources: CNBC TV18: RBI Banking Sector FY25, NPA Multi-Decade Low | Moneycontrol: Banks Asset Quality FY25 | Business Standard: CRISIL NPA Projection | Facebook/Business Standard: NBFC GNPA Stress Scenario | Subodh Bajpai: SARFAESI Act Explained | Airtel: NPA Recovery Process in Indian Banking | LinkedIn: RBI Guidelines for Debt Recovery 2025 | CredSettle: RBI Rules for Recovery Agents 2025 | CarmaOne: WhatsApp + AI Calling Dual-Channel Collections India | CarmaOne: Omnichannel Collections India 2026 | Edesy: AI Debt Collection India 2026 | GenZCFO: Managing NPAs in NBFCs | KSA&DK: NBFCs and SARFAESI 2025 | Enterslice: RBI Scale Based Regulation | INFORMS: Propensity Modeling to Minimize Collections Churn | ClearTouch: AI in Debt Collection India