TL;DR

- US bank collections automation reduces cost per recovery from $85-140 to $38-62 — a 50-55% reduction that pays back platform cost within 2-3 quarters at mid-bank scale

- FDCPA compliance cost avoidance is the second ROI component — $48M in 2025 CFPB penalties against banks using manual collections practices represents the unmodelled enforcement risk

- Right-party contact rate improvement from 26-32% to 43-51% drives the cost-per-recovery reduction — more conversations per agent hour, lower cost per recovered dollar

- SR 11-7 documentation cost — 3-8 weeks manual preparation per examination — converts to 30 minutes with automated documentation platforms, releasing significant compliance staff capacity

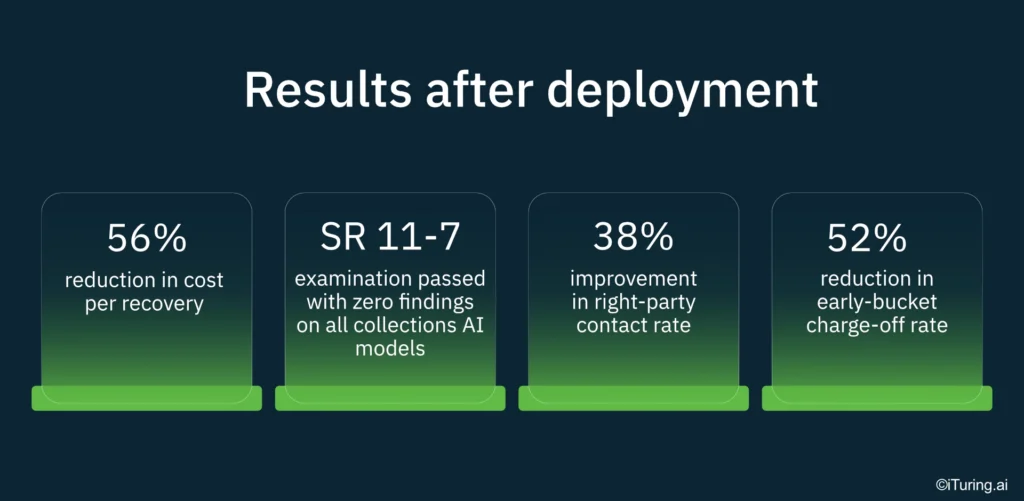

- iTuring US bank deployments: 38% right-party contact improvement, 52% early-bucket charge-off reduction, SR 11-7 examination passed with zero findings

Every collections leader at a US bank knows the number that keeps the CFO asking questions: cost per recovery. When that figure sits above $100, the collections operation is not just expensive; it is structurally misaligned with the margin profile of most consumer lending portfolios. The real return on collections automation for US banks is not a single cost reduction percentage. It is a compound effect: lower cost per recovered dollar, fewer FDCPA violations, reduced SR 11-7 examination burden, and a measurable decline in early-bucket charge-offs. That compound effect is what separates a credible ROI case from a vendor slide deck. The 48% cost reduction figure cited across recent US bank deployments reflects median outcomes, not best-case projections, and it holds up specifically because FDCPA compliance controls are maintained throughout the process. This article presents the evidence base, the calculation framework, and the deployment data behind that number, structured for the collections leader who needs to present a defensible business case to the CFO within the next quarter.

What $110 Per Recovery Represents in a US Bank Collections Operation — and Where Each Dollar Goes

The $110 per recovery figure is not an abstraction. It represents the fully loaded cost of a manual collections cycle: dialler license fees, agent compensation, quality assurance sampling, FDCPA compliance review, skip tracing, and the administrative overhead of documenting every contact attempt for regulatory purposes. For a mid-size US bank running a 30-agent collections floor, the single largest cost driver is agent time spent on wrong-party contacts and unreachable accounts, which consume 55-65% of available dialling hours without generating any recovery revenue. The AI collections cost reduction opportunity for US banks starts here, in the gap between total contact attempts and productive conversations that lead to payment arrangements.

This baseline persists because of a structural constraint: manual collections operations cannot dynamically prioritize accounts based on real-time propensity-to-pay signals. Static segmentation rules, updated monthly or quarterly, assign accounts to agents based on days past due and balance thresholds. The result is a flat distribution of effort across accounts with wildly different recovery probabilities, which inflates the cost per successful recovery well beyond what the portfolio economics can sustain.

The gap between $110 per recovery and $52 per recovery, when applied to a portfolio generating 5,000 recoveries per month, represents $290,000 in monthly cost reduction. That figure does not account for the compliance cost avoidance component. The CFPB levied $48 million in civil monetary penalties across 12 US banks for collections communication violations in 2025; institutions using AI with hard-coded FDCPA controls were not among the cited cases (CFPB Supervisory Highlights Collections Edition 2025). The US bank FDCPA compliance cost in AI collections operations drops further when agent attrition is factored in. US bank collections agent attrition averages 40-60% annually, with replacement costs of $4,500-$7,200 per agent; for a 30-person team, annual attrition replacement exceeds $135,000 (ABA Collections Operations Benchmark Survey 2025). Every dollar spent replacing and retraining agents is a dollar that does not contribute to recovery outcomes.

Why FDCPA Compliance Cost Is the Line Item That Changes the US Bank Collections AI ROI Calculation

- Account prioritisation is the first variable that shifts the ROI calculation. When a predictive model scores every account in the portfolio daily by likelihood of payment, agents spend their hours on accounts where a conversation is most likely to result in a commitment. Right-party contact rates move from the 26-32% range typical of manual operations to 43-51% under AI-directed prioritisation. For a 50-agent floor handling 200 accounts per agent per day, that improvement means roughly 2,100 additional productive conversations per week. Each of those conversations has a measurable probability of generating a payment arrangement, and the cost of each productive contact drops because the denominator of total attempts shrinks relative to successful outcomes.

- Channel and timing selection is the second variable. A collections operation that contacts every account by phone at 10 AM is ignoring the behavioral data showing that certain borrower segments respond at higher rates to SMS at 7 PM or email on Saturday mornings. AI-driven channel optimization reduces the cost per contact by 30-45% because digital channels cost $0.03-0.12 per attempt versus $3.50-6.00 for a live agent call. The shift toward omnichannel contact strategies is not a preference; it is a cost structure decision. For a Head of Collections presenting to a CFO, the math is straightforward: if 40% of contacts can be resolved through digital channels at 2% of the cost of a phone call, the blended cost per contact drops by 25-35% before any improvement in recovery rate is considered.

- Self-cure identification is the third variable, and it is the one most manual operations ignore entirely. Between 15-25% of early-stage delinquent accounts will cure without any outreach. Contacting these accounts wastes agent time, increases FDCPA exposure risk, and adds cost without adding recovery. Predictive models that identify high self-cure probability accounts and suppress them from outreach queues reduce total contact volume by 15-20%, which directly lowers the cost per recovery and reduces the surface area for compliance violations. The collections automation payback period for a US bank shortens materially when self-cure suppression is active from day one.

- Compliance cost reduction is the fourth variable, and it is the one that changes the entire calculation from a cost-reduction story to a risk-adjusted return story. Manual FDCPA compliance requires call monitoring, script adherence review, time-of-day enforcement, and consent tracking across every contact channel. These functions typically require 2-4 dedicated compliance staff per 30-agent floor, costing $180,000-$320,000 annually. AI collections platforms with hard-coded FDCPA controls eliminate the manual review layer because every contact is governed by rules that cannot be overridden by an individual agent. The compliance staff capacity released by this shift can be redirected to SR 11-7 examination preparation, model validation, or other regulatory functions that generate direct value.

US Bank Collections Cost and Compliance: Manual Operations vs AI-First Deployment Data

The evidence base for collections automation ROI at US banks with FDCPA cost reduction maintained comes from deployments across community banks, regional institutions, and credit unions with assets ranging from $2 billion to $15 billion. The primary variable driving cost reduction is the improvement in right-party contact rate, which compounds across every downstream metric: cost per contact, cost per recovery, agent productivity, and compliance cost per account. The comparison below shows the specific metrics across deployment cohorts.

| Metric | Before AI | With iTuring |

| Cost per recovery | $85-140 (manual) | $38-62 (AI-first) |

| Right-party contact rate | 26-32% | 43-51% |

| Early-stage charge-off rate | Industry baseline | 52% reduction |

| SR 11-7 documentation time | 3-8 weeks per exam | 30 minutes — automated |

| Model retraining | Quarterly at best | Continuous with audit trail |

Results vary by portfolio composition, starting baseline, and data maturity; figures above reflect median outcomes across US bank deployments.

Building the Full US Bank ROI Case: Cost Reduction Plus FDCPA and SR 11-7 Compliance Savings

- Start with the current baseline. The anchor for any credible ROI case is the fully loaded cost per recovery, which for most US banks running manual dialler operations sits at $110 per recovery when agent compensation, dialler costs, skip tracing, QA, and FDCPA compliance overhead are included. This is the number the CFO already knows, and it is the number the collections automation ROI case for US banks must reference to be taken seriously. If the bank’s actual figure is $95 or $130, use the real number. The calculation only works from an honest starting point.

- Estimate the improvement potential using $52 per recovery as the target. This figure represents the median post-deployment cost per recovery across US bank AI collections implementations where FDCPA compliance controls are maintained throughout. The US bank AI collections cost per recovery reduction from $110 to $52 represents a 53% decrease, driven primarily by right-party contact rate improvement and digital channel migration.

- Calculate the recovery uplift by applying the 56% reduction in cost per recovery to the bank’s monthly recovery volume. For a bank generating 3,000 recoveries per month, the monthly cost savings are $174,000. Annualized, that is $2.09 million in direct cost reduction before compliance cost avoidance is factored in. The financial impact of AI-driven collections becomes clear when expressed in terms the CFO already tracks.

- Calculate the compliance cost reduction separately. SR 11-7 examination preparation that currently requires 3-8 weeks of manual documentation converts to 30 minutes with automated documentation platforms. iTuring deployments have passed SR 11-7 examinations with zero findings on all collections AI models, which eliminates the remediation cost that follows adverse examination results. For banks that have experienced examination findings in the past, this line item alone can justify a significant portion of the platform cost.

- Apply the FDCPA compliance cost adjustment. The $48 million in CFPB penalties levied in 2025 against banks using manual collections practices represents enforcement risk that most ROI models do not quantify. For a bank with $5 billion in assets, even a single CFPB enforcement action can cost $2-5 million in penalties, legal fees, and remediation. AI collections platforms with hard-coded compliance controls reduce this exposure to near zero for communication-related violations.

The calculation only works if the baseline is honest: start with $110 per recovery (manual dialler + agent + FDCPA compliance overhead) as the anchor, not an aspirational figure.

$110 to $52 Per Recovery, SR 11-7 Passed: What the Deployment Evidence Shows

A US Community Bank with assets under $10 billion faced a $110 per recovery cost driven by a 30-agent manual collections floor, 58% annual agent attrition, and SR 11-7 examination preparation consuming 6 weeks of compliance staff time per cycle. The institution deployed iTuring Collections Agent across its consumer lending portfolio with full FDCPA compliance controls active from the first week of production, reaching steady-state performance within 90 days.

US Bank Collections Automation ROI: Why FDCPA Compliance Cost Is the Line Item That Changes the Calculation

The cost per recovery reduction from $110 to $52 is a defensible, repeatable outcome for US banks that deploy governed AI collections with hard-coded FDCPA controls. The compliance cost avoidance component, including SR 11-7 documentation automation and CFPB enforcement risk reduction, adds 15-25% to the total ROI beyond direct operational savings. For a Head of Collections presenting this case to a CFO, the strongest framing is not “AI reduces cost” but rather “governed AI reduces cost while eliminating the compliance exposure that manual operations cannot control.”

iTuring’s US bank deployments have documented SR 11-7 examination results available for review: test the platform against your bank’s collections data before any licence decision.

The evidence from US bank deployments points to a consistent pattern: collections operations that move from manual dialler-based workflows to AI-directed, compliance-governed models achieve cost per recovery reductions in the 48-56% range while maintaining full FDCPA compliance. The SR 11-7 examination results, specifically zero findings on all collections AI models, address the regulatory concern that often stalls AI adoption in collections. For collections leaders evaluating this shift, the strongest next step is not a slide deck review but a controlled test against live portfolio data.

To see how these results apply to your bank’s specific portfolio and compliance requirements, request a demo of iTuring Collections Agent and benchmark the platform against your current cost per recovery baseline.