TL;DR

- NBFC manual collections average Rs. 120-180 per recovery; AI-first deployments reduce this to Rs. 45-74 — a 60-70% cost reduction at the same portfolio

- The ROI case is not just cost per recovery — roll rate improvement prevents Rs. 8-15 crore from entering high-cost NPA stages annually at mid-size portfolio scale

- Agent attrition of 35-45% annually adds Rs. 18,000-24,000 per replacement — AI reduces required headcount and eliminates a significant recurring cost

- Payback period for NBFC collections AI is typically 1-2 quarters — cost reduction at scale exceeds platform costs within the first year

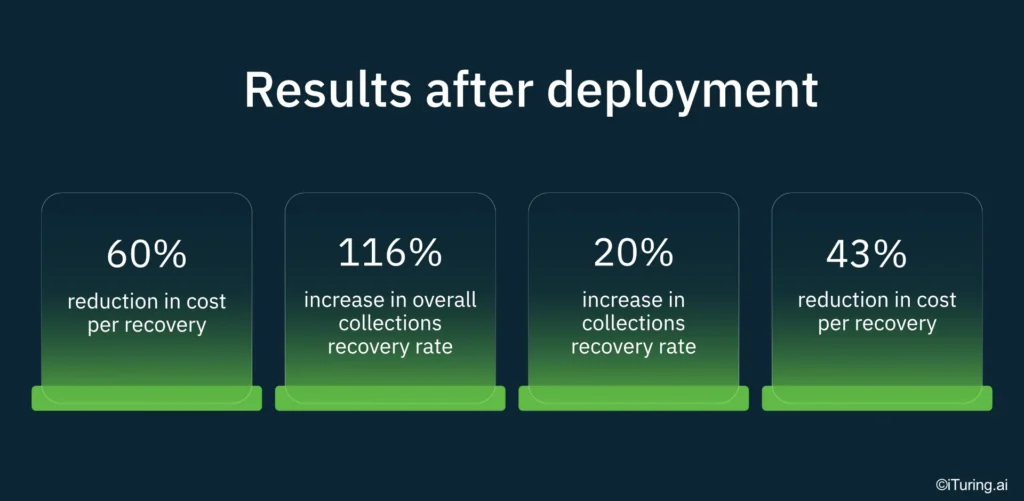

- iTuring’s NBFC deployments show 116% increase in collections recovery rate, 60% cost reduction, and 10x ROI at 12 months

The difference between a profitable collections operation and a loss-making one often comes down to a single number: cost per recovery. For Indian NBFCs managing portfolios of Rs. 500 crore or more, that number determines whether the collections function operates as a cost centre or a margin contributor. Collections cost benchmarking for Indian NBFCs has become a pressing priority as the gap between manual agent economics and AI-first platform economics widens every quarter.

Most Heads of Collections already sense this gap intuitively. They see the attrition, the idle time between calls, the compliance rework, and the growing cost of maintaining large agent teams. What they often lack is a precise, evidence-backed framework to quantify the difference and present it to a CFO. This article provides that framework, grounded in deployment data from 24 NBFCs, with specific metrics on cost per recovery, roll rate impact, and payback timelines.

The credit ecosystem in India is expanding, with NBFCs expected to play a larger role in credit delivery across retail, MSME, and microfinance segments. As portfolios grow, the economics of collections become more consequential. A Rs. 85 difference in cost per recovery, multiplied across hundreds of thousands of accounts, is the difference between margin expansion and margin erosion. The numbers that follow are drawn from real deployments, not projections.

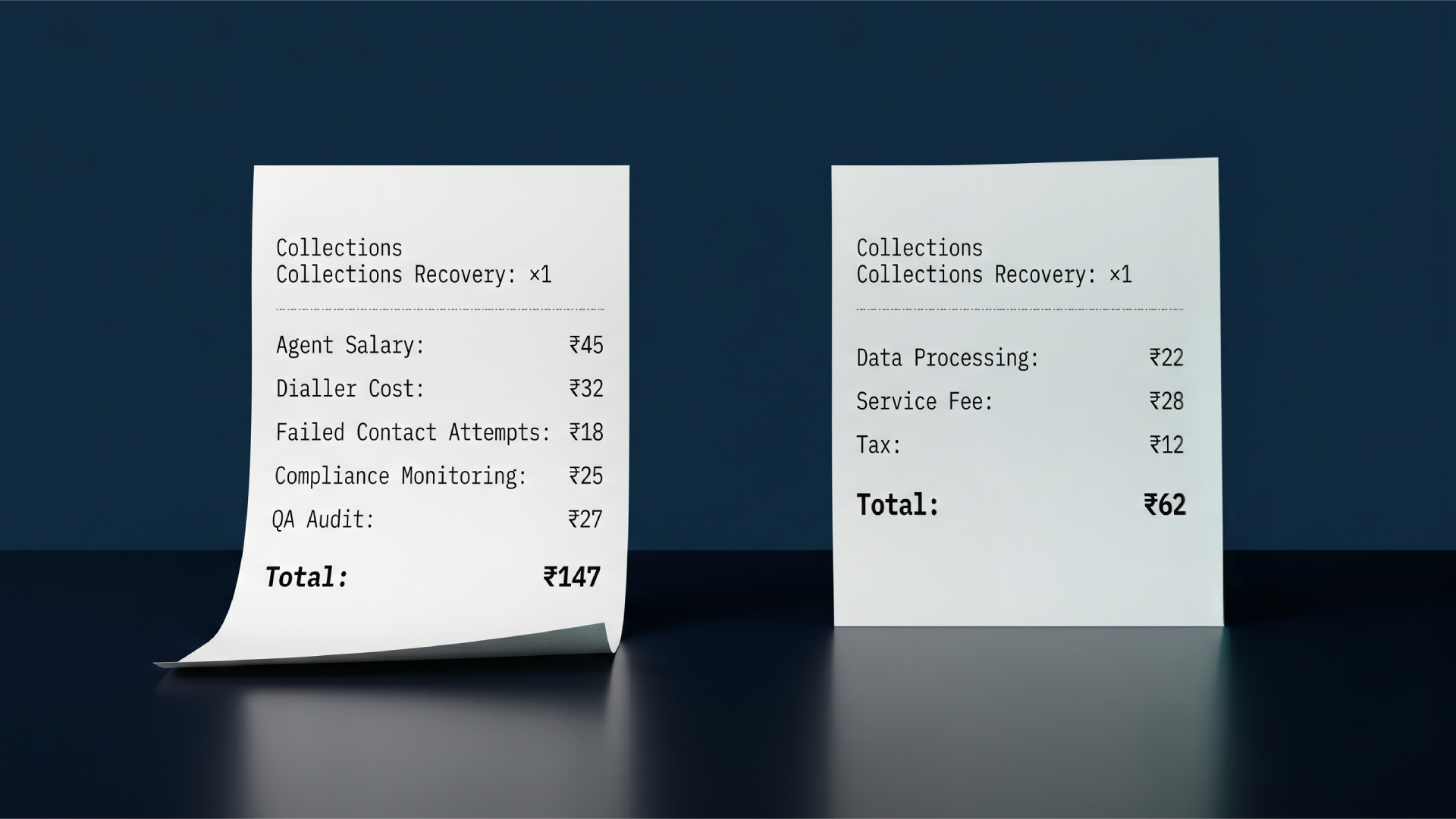

What Rs. 147 Per Recovery Actually Costs an NBFC at Portfolio Scale

The Rs. 147 per recovery figure is not a single line item. It is the fully loaded cost of a manual collections operation: agent salaries, dialler infrastructure, supervisor overhead, compliance monitoring, training, and the hidden cost of failed contacts. For an NBFC running a portfolio of Rs. 800 crore with 40,000 delinquent accounts per month, that Rs. 147 translates to roughly Rs. 59 lakh in monthly collections expenditure before accounting for any recovery outcome. The NBFC AI collections ROI in India for 2025 and 2026 starts with understanding this baseline honestly, because most internal estimates undercount by 20-30% once attrition and ramp costs are included.

This baseline persists because of a structural constraint: manual operations scale linearly. Every additional 1,000 accounts in the queue requires proportional agent headcount. There is no efficiency curve. An NBFC that doubles its delinquent book doubles its collections cost, with no mechanism to absorb volume through better prioritisation or channel selection. The dialler dials. The agent speaks. The cost accrues whether the borrower answers or not.

The gap between Rs. 147 per recovery and Rs. 62 per recovery becomes stark at portfolio scale. NBFC manual collections average Rs. 120-180 per recovery versus Rs. 45-74 with AI-first platforms, per benchmark data across 24 NBFC deployments (iTuring NBFC Collections Economics Benchmark 2024-25). On a portfolio generating 30,000 successful recoveries per month, the difference is Rs. 25.5 lakh monthly, or over Rs. 3 crore annually. Agent attrition at NBFC collections centres averages 35-45% annually, and each replacement costs Rs. 18,000-24,000 in recruitment, training, and productivity ramp (FICCI-KPMG NBFC Operations Benchmark 2025). AI-driven platforms that reduce required agent headcount directly eliminate this recurring cost, making NBFC collections agent cost reduction through AI a measurable financial outcome rather than an aspiration.

The Four Variables That Determine Whether Your NBFC Lands at Rs. 62 or Rs. 147

- Account prioritisation determines right-party contact rate, and right-party contact rate determines cost per recovery more than any other single variable. Manual operations typically assign accounts by DPD bucket or outstanding amount. AI-based prioritisation scores accounts by propensity to pay, propensity to self-cure, and optimal contact timing. One mid-size NBFC running a two-wheeler loan portfolio saw its right-party contact rate rise from 28% to 47% within 60 days of deploying propensity-based queue ordering, which directly reduced cost per successful contact by 38%.

- Channel and timing selection affect cost per contact, which is the denominator in any cost-per-recovery calculation. A manual voice call costs Rs. 8-12 per attempt. A WhatsApp message costs Rs. 0.50-1.50. An IVR reminder costs Rs. 0.30-0.80. The question is not whether digital channels are cheaper; it is which channel works for which borrower at which stage of delinquency. AI models that match channel preference to borrower behaviour reduce wasted spend on calls that will not be answered. For an NBFC presenting this to a CFO, the India NBFC collections platform ROI payback becomes visible when channel optimization alone drops cost per contact by 40-55%.

- Self-cure identification removes accounts from the contact queue entirely. Between 15% and 25% of accounts in early delinquency will cure without any intervention. Manual operations cannot reliably identify these accounts, so agents call them anyway, incurring cost with zero marginal recovery. AI models trained on payment patterns, salary credit timing, and historical cure behaviour flag self-cure accounts before the first contact attempt. One consumer lending NBFC removed 22% of its 0-30 DPD queue through self-cure identification, freeing agent capacity for accounts that actually required intervention.

- Compliance cost reduction affects total operations cost in ways that rarely appear on a collections P&L. Manual compliance monitoring requires dedicated QA teams who audit call recordings, check script adherence, and flag potential RBI guideline violations. AI-native platforms embed compliance checks into every interaction: time-of-day restrictions, language guidelines, frequency caps, and disclosure requirements are enforced automatically. One NBFC reduced its compliance QA headcount by 60% after deploying governed AI collections, eliminating Rs. 14 lakh in annual QA salary costs alone.

NBFC Collections Cost Benchmarks: Manual Operations vs AI-First Platform Data

The evidence base for these benchmarks spans 24 NBFC deployments across consumer lending, vehicle finance, microfinance, and MSME segments. NBFCs that achieved the lowest cost per recovery in India shared a common trait: they deployed AI-first platforms with integrated channel orchestration rather than adding AI as a layer on top of existing manual processes. The variable that drove the most significant cost reduction was right-party contact rate improvement, which cascaded into lower cost per contact and higher recovery yield per agent hour. The comparison below shows the specific metrics across deployment cohorts.

| Metric | Before AI | With iTuring |

| Cost per recovery | Rs. 120-180 (manual) | Rs. 45-74 (AI-first) |

| Right-party contact rate | 26-31% | 44-51% |

| 30-60 DPD roll rate | 22-28% | 14-19% |

| Self-cure identification | Not available | Removes 15-25% of queue |

| Model retraining | Quarterly or ad hoc | Continuous — automated |

Results vary by portfolio composition, starting baseline, and data maturity — figures above reflect median outcomes across NBFCs deployments.

Building the Rs. 62 Per Recovery Case for Your NBFC Portfolio

Step 1: Establish the current baseline with precision. The NBFC collections cost per recovery in India for manual operations anchors at Rs. 147 when fully loaded costs are included: agent salaries, dialler fees, supervisor time, QA overhead, attrition replacement, and compliance monitoring. Most internal finance teams report a lower number because they exclude indirect costs. The AI collections cost benchmark for Indian NBFCs in 2025-2026 only holds analytical value if the starting point is accurate.

Step 2: Set the target at Rs. 62 per recovery based on median outcomes from comparable NBFC deployments. This is not a theoretical floor. It reflects actual cost per recovery achieved by NBFCs with similar portfolio sizes and delinquency profiles after 6-9 months of AI-first operations. The gap between Rs. 147 and Rs. 62 is Rs. 85 per recovery, which becomes the unit economics basis for the entire ROI model.

Step 3: Calculate the cost reduction by applying the 60% reduction in cost per recovery to current monthly collections expenditure. If the NBFC currently spends Rs. 44 lakh per month on collections operations, a 60% reduction yields Rs. 26.4 lakh in monthly savings, or Rs. 3.17 crore annually. This number goes directly to the CFO as a cost avoidance figure.

Step 4: Layer in the recovery uplift. A 116% increase in overall collections recovery rate means the NBFC is not just spending less per recovery but recovering more. If current monthly recoveries total Rs. 12 crore, a 116% increase brings that to Rs. 25.9 crore. The combined effect of lower cost and higher recovery creates a compounding margin improvement that justifies the platform investment within the first two quarters.

Step 5: Apply the compliance cost adjustment. NBFCs operating under stricter RBI scrutiny, particularly those with microfinance or consumer lending portfolios, carry higher compliance monitoring costs. AI-native platforms that enforce regulatory guidelines automatically reduce QA headcount and audit preparation time. For some NBFCs, this adjustment adds Rs. 8-15 lakh in annual savings beyond the core cost-per-recovery calculation.

The calculation only works if the baseline is honest: start with Rs. 147 cost per recovery (manual dialler + agent operations) as the anchor, not an aspirational figure.

116% Recovery Rate Increase, 43% Cost Reduction: Numbers From a Live NBFC Deployment

A leading NBFC in India with a diversified retail lending portfolio faced a persistent Rs. 147 per recovery cost structure driven by high agent attrition, low right-party contact rates, and manual compliance monitoring across its collections operation. The institution deployed iTuring Collections Agent with integrated propensity scoring, channel orchestration, and self-cure identification across its 30-90 DPD book, with full production deployment completed within 8 weeks.

The NBFC Collections AI Cost Calculation: Why Payback Is Measured in Quarters, Not Years

The payback arithmetic for collections AI at Indian NBFCs is straightforward: platform costs are fixed and monthly, while savings scale with portfolio volume, meaning larger books reach breakeven faster. Most mid-size NBFCs with delinquent books above Rs. 200 crore recover their full platform investment within 1-2 quarters, and the cost comparison between AI and manual telecalling only widens as agent attrition compounds through the year. A CFO evaluating this investment should model the payback on current delinquent volume alone, without assuming portfolio growth, to arrive at a conservative estimate that still clears any internal hurdle rate.

Where the Rs. 62 Benchmark Goes From Here

The cost-per-recovery gap between manual and AI-first collections operations at Indian NBFCs is not closing. It is widening. As multilingual AI voice capabilities mature and vernacular language coverage expands across Hindi, Tamil, Telugu, Kannada, and Marathi, the addressable borrower base for AI-first contact grows. NBFCs that locked in AI-first economics in 2024-2025 are now operating at Rs. 45-74 per recovery while their manual peers remain at Rs. 120-180. Every quarter of delay compounds the cost disadvantage.

The framework presented here is not theoretical. It is drawn from 24 NBFC deployments with documented outcomes: 60% cost reduction, 116% recovery rate increase, and payback within two quarters. The five-step ROI calculation gives any Head of Collections the structure to present this case to a CFO with confidence, provided the baseline is honest.

iTuring is live at 18 NBFCs with documented cost-per-recovery data: test the ROI model against your NBFC’s own baseline before any licence decision.