TL;DR

- RBI permits collection contact only between 8:00 AM and 7:00 PM

- No contact allowed on Sundays, holidays, or during sensitive occasions

- RBI levied Rs. 48 crore in penalties on NBFCs for collections violations in FY25

- AI-driven collections achieve 99.97% compliance vs. 87-92% for human agents

- iTuring automates contact rules, tone validation, and audit trails across 10 languages

On February 10, 2026, the Reserve Bank of India released a draft framework proposing uniform recovery norms across all regulated entities (banks, NBFCs, and housing finance companies) under one consolidated set of rules. Contact restrictions tightened. Data governance obligations deepened. Agent oversight requirements expanded. And the accountability for what a recovery agent does in the field now rests unambiguously with the lender who engaged them.

The timing reflects deliberate regulatory intent. India’s banking sector has spent the last four years driving gross NPA ratios down to a multi-decadal low of 2.1% as of September 2025. The RBI is now signalling that sustaining that progress requires equally hard discipline on the collections side, the part of the credit cycle where borrower rights most often come under pressure. For ai for banks deployments in the Indian collections context, this regulatory moment is the design brief: automation must be built around these obligations from the architecture up, not configured to accommodate them after deployment.

For compliance heads and CROs at Indian banks and NBFCs, the question is no longer whether to automate collections. The question is whether the automation they deploy is built for this regulatory environment specifically. This post walks through exactly what the RBI Recovery Agent Guidelines require, where automation creates compliance risk if deployed carelessly, and how to build a framework that achieves both collections efficiency and full regulatory compliance.

What the RBI Recovery Agent Guidelines Actually Require

The RBI’s recovery agent framework has been in place since the early 2000s, but it has been progressively strengthened through Master Directions, Fair Practices Code circulars, and Digital Lending Guidelines. The February 2026 draft framework consolidates and elevates all of these into a single structured set of obligations.

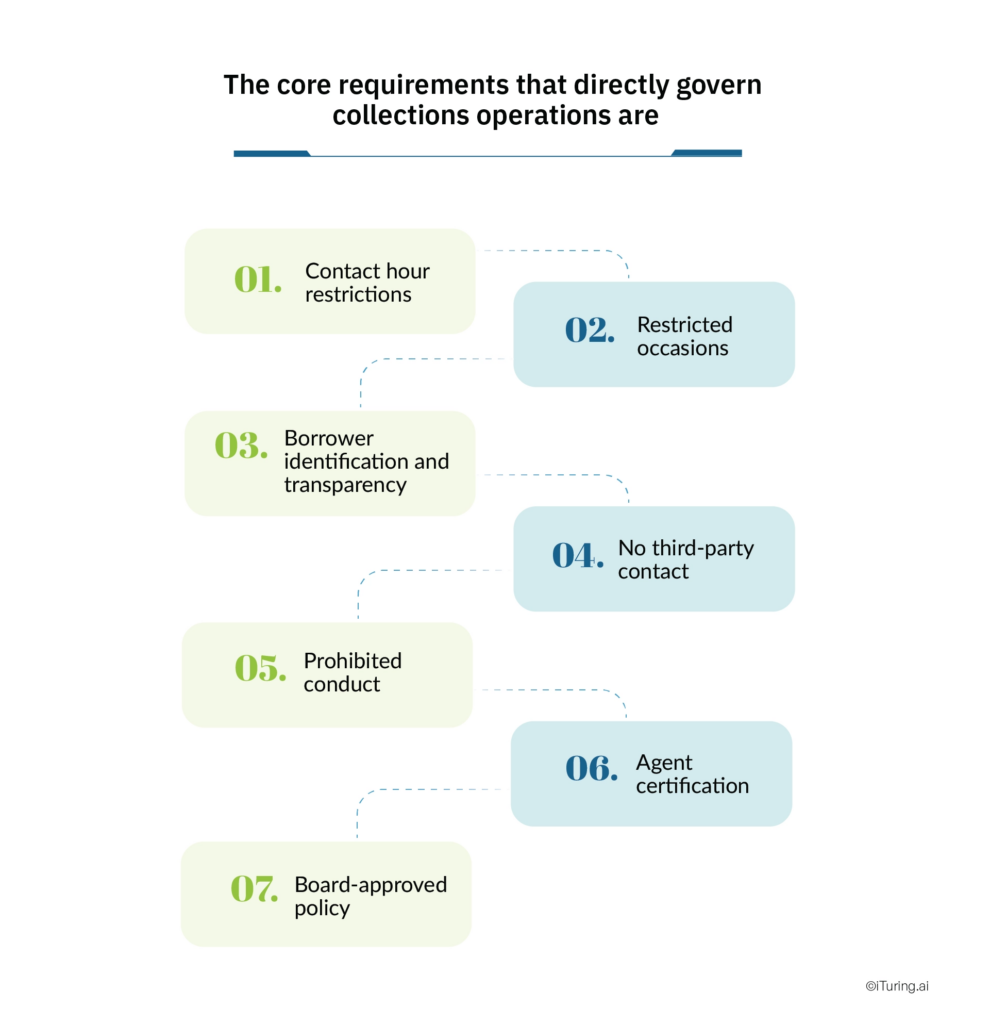

The core requirements that directly govern collections operations are:

Contact hour restrictions. Recovery agents and any automated system acting in their capacity may contact borrowers only between 8:00 AM and 7:00 PM, Monday through Saturday. No contact is permitted on Sundays or public holidays. Calls or messages outside this window are classified as harassment under the guidelines, regardless of intent.

Restricted occasions. The February 2026 draft directions explicitly prohibit contact during bereavement, marriage functions, festivals, and other sensitive occasions. This applies to calls, SMS, WhatsApp, and digital notifications alike.

Borrower identification and transparency. Every collection interaction must clearly identify the regulated entity on whose behalf it is being made. The agent or automated system must state the lender’s name, loan reference number, and the nature of the contact at the outset. This requirement, drawn from RBI’s Digital Lending Guidelines, extends fully to AI-driven collection workflows.

No third-party contact. Agents are prohibited from discussing a borrower’s default with family members, friends, colleagues, or employers. Contact must be directed only at the borrower or guarantor. This restriction applies at the individual interaction level and must be enforced in every workflow.

Prohibited conduct. The guidelines explicitly forbid abusive language, excessive or anonymous calls, intimidation, threats of violence, misleading representations, and any intrusion into borrower privacy.

Agent certification. Every debt recovery agent engaged by a bank or NBFC must hold a valid certificate from the Indian Institute of Banking and Finance (IIBF), obtained after completing 50 to 100 hours of structured training and passing the IIBF examination. The 2025 update reinforced that this certification requirement extends to all representatives of third-party agencies engaged by regulated entities.

Board-approved policy. The February 2026 draft framework mandates a formal, documented recovery policy at the board level covering agent eligibility, due diligence standards, performance evaluation, inspection mechanisms, and penal actions for non-adherence. This policy must be published on the institution’s website.

Where Collections Automation Creates Compliance Risk

Any ai for banks deployment in collections that replicates manual process gaps at scale amplifies liability rather than reducing it. The risk points are specific and predictable, and a compliant banking ai platform must address all of them by design rather than by policy overlay.

Contact hour violations. An automated dialer or SMS platform that does not enforce the 8:00 AM to 7:00 PM contact window will generate RBI violations at scale. The larger the portfolio, the faster the violations accumulate. A single misconfigured batch job sending payment reminders at 9:30 PM across 50,000 accounts is a regulatory event, not a technical glitch.

Frequency harassment. Automated systems can contact the same borrower multiple times in a single day across multiple channels simultaneously: a call, an SMS, and a WhatsApp message within the same hour. Without frequency governors built into the workflow, this constitutes the “excessive calls” harassment that the RBI guidelines specifically prohibit.

Tone failures in AI-generated messages. Natural language generation and AI communication tools can produce messages with unintended threatening tone, especially when not trained specifically for the Indian collections regulatory context. A message that uses language like “failure to pay will result in immediate legal action” without proper qualifying language can cross the line from firm to coercive under the guidelines.

Absence of cease-and-desist functionality. When a borrower makes a complaint or requests cessation of contact, that instruction must be actioned immediately and maintained across all channels. An automated system without built-in complaint-triggered pause functionality will continue contacting a borrower who has formally objected, a direct violation.

Data sharing with third-party platforms. Under the Digital Personal Data Protection Act (DPDP) 2023 and RBI’s data governance requirements, borrower data shared with AI collection platforms must be subject to clear data principal rights and stored within India. Platforms that store or process borrower data outside India breach data localisation requirements regardless of their collection performance.

The RBI levied Rs. 48 crore in aggregate penalties on NBFCs for collection-related violations in FY 2024-25. These were not edge cases involving rogue agents. They reflected systemic gaps in how collection operations were designed and supervised. Automation that carries those same gaps into a scaled deployment simply magnifies the exposure.

The Automation-Compliance Framework for Indian Collections

Building a compliant collections automation framework means hardcoding the RBI’s requirements into the operational logic of every workflow as a banking ai platform obligation, not treating them as an overlay to be checked after the fact. The credit risk decisioning layer that sits at the top of the collections workflow determines which accounts enter which treatment path. How that triage is designed determines whether the downstream automation stays within RBI boundaries or systematically breaches them.

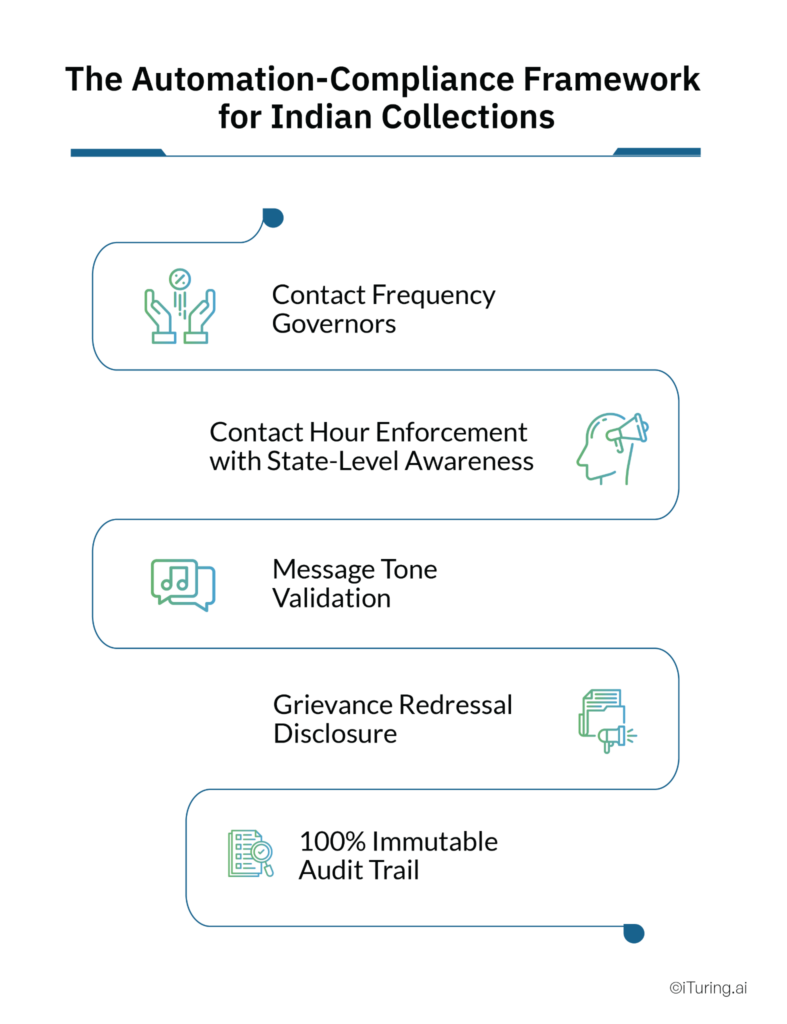

Contact Frequency Governors

Every automated contact system must enforce maximum contact frequency limits at the account level, not just the channel level. A borrower who has received two calls, one SMS, and one WhatsApp message in a single day has been contacted four times, regardless of channel. The frequency governor must count across all channels, reset at midnight, and block further attempts once the daily limit is reached.

Contact Hour Enforcement with State-Level Awareness

The 8:00 AM to 7:00 PM window must be enforced based on the borrower’s location, not the operations centre’s timezone. India has a complex public holiday calendar that varies by state. As RBI guidelines state, contact on Sundays and public holidays is not permitted, making a static national holiday list insufficient for full compliance. Sunday and public holiday calendars must be integrated into the contact scheduling layer with state-level granularity.

Message Tone Validation

Every AI-generated or template-based message (SMS, WhatsApp, IVR script, email) must be validated against RBI conduct requirements before being deployed. This means automated tone-checking that flags prohibitive, threatening, or misleading language before it reaches the borrower. For institutions operating in multiple languages, this validation must work across every language in use.

Grievance Redressal Disclosure

Every collection interaction must include information about the institution’s grievance redressal mechanism. For automated interactions, this means including a standard disclosure in every SMS, email, and IVR flow: the lender’s grievance officer contact details, the escalation process, and the borrower’s right to raise a complaint.

100% Immutable Audit Trail

The RBI mandates 100% call recording for all collection communications under the Fair Practices Code. For automated workflows, this requirement extends to every digital touchpoint: SMS delivery receipts, email open logs, IVR interaction records, and agent call recordings. The immutable audit trail must be complete, searchable, timestamped, and tamper-proof, accessible for RBI examination at short notice and structured so that no record can be altered or deleted after the interaction has occurred.

Vernacular Language Compliance Challenges

The RBI’s borrower communication requirements apply in every language a collection interaction occurs in. For Indian banks and NBFCs operating across geographies, this creates a specific and technically demanding challenge.

India’s 10 major regional languages, Hindi, Tamil, Telugu, Kannada, Malayalam, Bengali, Marathi, Gujarati, Odia, and Punjabi, each carry their own register of formal and informal speech, their own ways of conveying urgency, and their own cultural context for what sounds respectful versus coercive. A message that reads as firm but professional in one language can, if machine-translated without contextual review, come across as threatening in another.

This is one of the most common sources of borrower complaints in multi-lingual collection operations. Automated systems that generate vernacular messages by direct translation from Hindi or English templates, without language-specific tone calibration, routinely produce communications that violate the spirit of the RBI conduct guidelines even when the translated words are technically accurate.

Compliance-grade vernacular collections automation requires language-specific message libraries validated by native speakers with knowledge of the RBI guidelines, and automated tone-checking at the language level before messages are deployed.

What the RBI Examiner Will Check

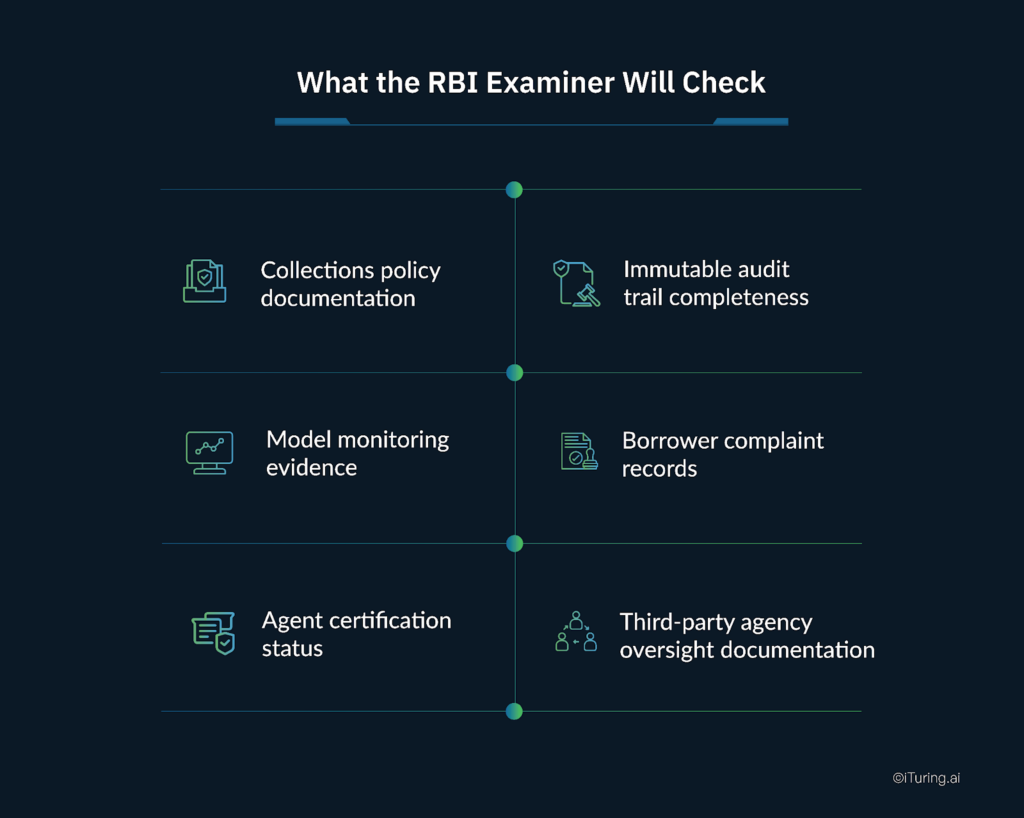

Compliance is not only about what happens in day-to-day operations. It is about what can be demonstrated when the RBI examiner arrives. Model monitoring records, audit trail completeness, and complaint resolution logs are the three documentation areas where examination findings are most frequently generated.

Collections policy documentation. The board-approved recovery policy must exist, be current, and reflect the institution’s actual operational practices. A policy written for 2022 that has not been updated to reflect the 2026 draft framework will draw observations.

Immutable audit trail completeness. Examiners will sample-check contact records against borrower accounts. Gaps in call recording, missing SMS logs, or incomplete IVR interaction records are red flags that trigger deeper examination of the compliance framework. The immutable audit trail must be complete across every channel for every contact attempt, not just for agent voice calls.

Model monitoring evidence. For institutions running AI-assisted collections workflows, examiners increasingly expect documented model monitoring records showing that the credit risk decisioning and contact strategy models are performing within their validated parameters, that drift has been detected and addressed, and that compliance guardrails have not degraded since the model was last formally validated.

Borrower complaint records. The volume, nature, and resolution timeline of borrower complaints related to recovery agent conduct is a direct indicator of compliance culture. A high complaint volume with slow resolution is a finding regardless of what the policy document says.

Agent certification status. All recovery agents and their representatives, including those employed by third-party agencies, must hold valid IIBF certification. An examiner who finds that a subset of agents are uncertified will treat this as a systematic failure of the institution’s oversight framework.

Third-party agency oversight documentation. Agreements with collection agencies must include the conduct requirements from the RBI guidelines. Periodic review and monitoring records must demonstrate that the institution is not merely delegating compliance to a third party without verification.

The Business Case for Compliance Automation

At first glance, investing in compliance automation can feel like a cost centre decision. The data makes it look very different.

AI-driven collections platforms achieve 99.97% compliance rates compared to 87-92% for human agent operations in audited deployments. That gap reflects the structural impossibility of manually monitoring thousands of daily collection touchpoints across 147 RBI circulars on digital lending and collections practices issued between 2022 and 2025. Automated guardrails enforce rules consistently at scale in a way that human supervision cannot replicate.

The cost of non-compliance compounds quickly. Regulatory penalties are the visible part. Reputational damage from borrower complaints that surface publicly, restrictions on business activity during examination findings, and the management time consumed by remediation all add costs that dwarf the investment in compliant automation.

How iTuring Addresses This

iTuring’s collections platform delivers ai for banks and NBFCs in the Indian market with RBI Recovery Agent Guidelines compliance built in as a core design requirement, not a configuration option. The banking ai platform implements all six guardrails simultaneously: contact hour enforcement, frequency governors, tone validation, grievance redressal disclosure, cease-and-desist automation, and immutable audit trail generation across every channel and language.

Contact hour enforcement is hardcoded at the platform level, blocking all contact attempts outside the 8:00 AM to 7:00 PM window including Sundays and public holidays with state-level calendar integration. The credit risk decisioning layer scores every account daily, routing accounts to the appropriate treatment path based on default propensity, payment propensity, and cure propensity before any contact decision is executed. Frequency governors operate across all channels simultaneously, counting every touchpoint against the daily account-level limit regardless of channel.

Message tone validation covers all 10 major Indian regional languages, flagging non-compliant language before it reaches the borrower. Every contact attempt, delivery confirmation, and borrower response is logged to an immutable audit trail with one-click examination-ready reporting. Model monitoring tracks credit risk decisioning model performance continuously, with automated alerts when model behaviour diverges from validated parameters and a complete evidence trail available for RBI examination at short notice.

The 4-week deployment timeline means compliance infrastructure is live before the next examination cycle. For collections heads and CROs who want to understand what their current compliance exposure looks like before making any platform decision,

Regulatory Disclaimer

The information in this blog is provided for general informational purposes only and does not constitute legal, compliance, or regulatory advice. Collections operations in India are governed by the Reserve Bank of India’s Master Directions, Fair Practices Code, Digital Lending Guidelines, the Digital Personal Data Protection Act 2023, and applicable state-level regulations. The RBI’s February 2026 draft framework on uniform recovery norms is subject to finalisation and may change before it takes effect. Banks and NBFCs should consult qualified legal and compliance counsel and monitor RBI communications for finalised regulatory requirements. iTuring’s stated compliance performance metrics are based on client implementations and audited deployments; results may vary depending on configuration, data quality, and portfolio characteristics.

Sources: Vinod Kothari: RBI Proposes Uniform Recovery Norms 2026 | Bajaj Finserv: RBI Guidelines for Recovery Agents | CarmaOne: RBI Compliant AI Collections Guide India 2026 | IIBF: Debt Recovery Agent Rules and Syllabus | BFSI Economic Times: NPAs Multi-Decadal Low | Inc42: Digital Debt Collection RBI Guidelines