TL;DR

- FSCA enforces TCF through conduct examinations focused on evidence of outcomes, not policies

- FSCA ramped up to over 1,350 enforcement-type actions in its 2024/25 financial year

- Outcomes 1, 3, and 6 are the three most directly applicable to collections operations

- FSCA published its Consumer Vulnerability Statement in March 2024, now embedded in TCF supervision

- AI collections improves TCF outcomes by detecting vulnerable customers earlier and reducing complaint risk

There is a well-known gap in how South African financial institutions handle the TCF framework.

Every regulated bank and insurer has a TCF policy. Most have TCF training programmes. A significant number have TCF committees. What far fewer have is TCF outcome measurement for collections specifically: the operational data, the management information reports, and the documented evidence of outcomes delivered that the FSCA actually examines when it reviews a collections operation.

The distinction matters because the FSCA’s TCF framework is explicitly outcomes-based, not policy-based. Regulated entities are expected to demonstrate that they deliver the six TCF outcomes to their customers throughout the product lifecycle, including collections, which is unambiguously part of that lifecycle. Demonstrating delivery requires evidence. Evidence requires measurement. And measurement requires that someone has defined, in advance, what a TCF-compliant collections operation looks like in metric form. For AI-powered collections, that measurement obligation extends to the models themselves: a responsible ai framework for collections AI must be capable of generating the evidence the FSCA expects, not just producing decisions.

This post maps the three TCF outcomes most directly applicable to collections, defines the measurement framework the FSCA expects to find in place, and shows how AI-powered collections tools improve TCF outcome delivery while simultaneously generating the evidence base that conduct examinations require.

The TCF Framework: An Outcomes-Based Approach

TCF is an outcomes-based regulatory and supervisory approach designed to ensure that regulated financial institutions deliver specific, clearly defined fairness outcomes for financial customers. It was introduced in South Africa by the then-Financial Services Board and has been progressively embedded in the FSCA’s supervisory methodology since it assumed conduct regulation responsibilities under the Financial Sector Regulation Act.

The FSCA’s enforcement posture has strengthened materially. In its 2024/25 financial year, the FSCA took over 1,350 enforcement-type actions, a significant increase from prior years, with institutional governance and corporate culture specifically identified as core interest areas for examination. For collections operations, this translates directly: an FSCA examiner reviewing a collections function is looking for management information that demonstrates TCF outcomes are being achieved, monitored, and acted upon when they are not.

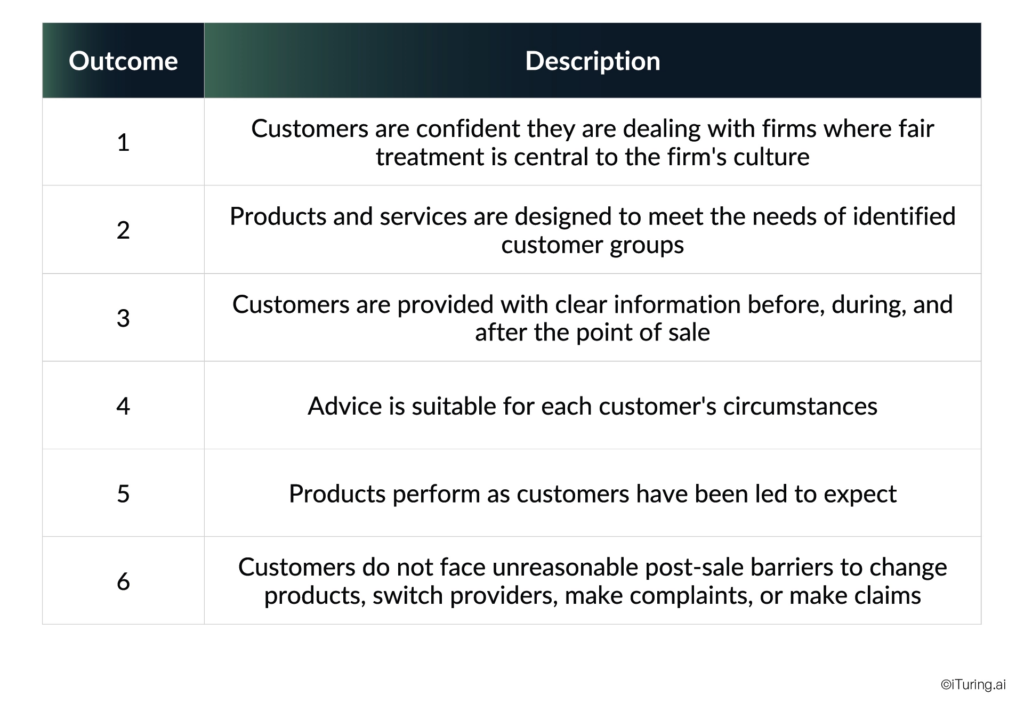

The six TCF outcomes, positioned from the customer’s perspective, are:

Of these six, three apply directly and substantially to collections operations. The others are primarily relevant at product design and distribution stages, important for TCF compliance overall, but outside the primary scope of a collections function’s TCF obligations.

The Three TCF Outcomes That Apply Directly to Collections

Outcome 1: Fair Treatment Is Central to Corporate Culture

Outcome 1 requires that customers be confident they are dealing with firms where fair treatment is genuinely central to the culture. For collections specifically, this is the most fundamental and hardest to evidence outcome. Culture is not a single metric. The FSCA assesses it through a composite of evidence: how complaints are handled and escalated, whether collections staff are trained in fair treatment principles, how management responds when TCF violations are identified, and whether TCF performance is reviewed by the board.

For AI-driven collections, Outcome 1 also requires a responsible ai framework that governs how automated decisions are made and reviewed. A collections AI model that has never been through model validation for disparate impact or fairness cannot demonstrate Outcome 1 compliance, because the institution cannot show that its automated decisions treat similar customers consistently.

For a collections operation, demonstrating Outcome 1 compliance means having:

- Board-level visibility of collections TCF metrics on a quarterly basis

- A named TCF accountability owner for the collections function

- Documented root cause analysis for every TCF-related complaint

- Evidence that TCF training is conducted and that training completion is monitored

- Model validation records showing AI-driven decisions have been tested for fairness before deployment

Outcome 3: Clear Information Before, During, and After the Point of Sale

Outcome 3 is typically discussed in the context of product disclosure at origination. In collections, it applies differently but equally. A borrower in default has the right to clear, accurate information about the amount outstanding, the collections process, their rights and options, and the consequences of non-payment. Collections communications that are ambiguous, misleading, or that obscure the consumer’s options create Outcome 3 exposure.

For AI-driven collections specifically, Outcome 3 requires that automated communications across SMS, WhatsApp, IVR, and email contain accurate information, present options clearly, and do not create a false impression of urgency or legal consequence that the lender has not yet initiated. A collections AI system that sends messages implying imminent legal action before any legal instruction has been given creates an Outcome 3 violation regardless of its technical accuracy in other respects.

Outcome 6: No Unreasonable Post-Sale Barriers

Outcome 6 requires that customers face no unreasonable barriers to resolving their situation after the point of sale. In collections, this translates to a specific set of operational requirements:

- A borrower in default must have a readily accessible path to request a payment arrangement

- Complaint channels must be accessible and functional, not automated-only loops that prevent human resolution

- A consumer who disputes a debt must have a clear, documented process for raising and resolving that dispute

- Payment plan terms must be designed to succeed: a plan that sets instalments the consumer demonstrably cannot afford is itself an Outcome 6 concern

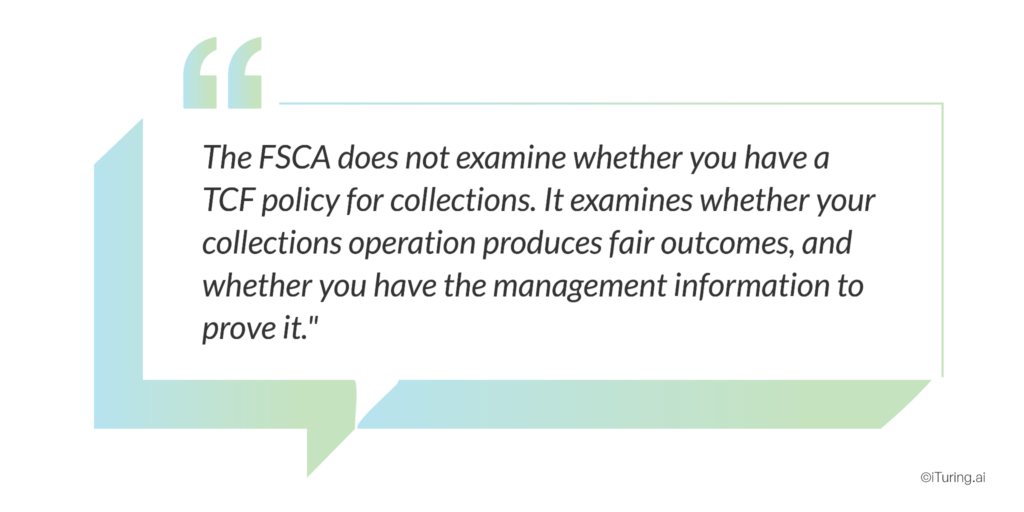

What TCF Outcome Measurement Actually Means

The critical operational distinction is between having a TCF policy and measuring TCF outcomes. FSCA requires evidence of outcomes delivered, not descriptions of processes designed to deliver them. For AI collections specifically, model validation before deployment is the first layer of that evidence: it demonstrates that the models generating decisions have been tested for accuracy, consistency, and fairness before they influenced any customer outcome.

For collections operations, TCF outcome measurement means monthly management information tracking the following metrics:

Complaint rate per 1,000 accounts in collections (target: below 5 per 1,000). A collections complaint rate is the most direct observable signal of whether customers are experiencing unfair treatment. A rising complaint rate is an early warning of a systemic TCF issue, whether in the contact strategy, the communication language, the payment plan terms, or the agent conduct. A stable, low complaint rate is direct evidence of Outcome 1 delivery.

Average complaint resolution time (target: below 14 days). The speed with which complaints are resolved signals how embedded fair treatment actually is. An institution that acknowledges complaints but resolves them slowly, or closes them without substantive investigation, is demonstrating Outcome 1 non-compliance through its behaviour rather than its policies.

Vulnerable customer identification rate (target: 100% of flagged accounts). Every collections operation should have a protocol for identifying customers who may be experiencing financial hardship, mental health challenges, or other vulnerability indicators that require modified treatment. The FSCA now requires a documented identification and handling process for vulnerable customers. An identification rate below 100% means vulnerable customers are passing through the standard collections process without the modifications the FSCA requires.

Payment plan approval rate (target: above 80%). A collections operation that rejects the majority of payment plan requests, or that makes payment plan access difficult through process complexity, creates Outcome 6 exposure. The approval rate for payment plan requests is a measurable proxy for whether the institution is creating unreasonable barriers to resolution.

Repeat default rate on payment plans (target: below 30%). A payment plan that a customer defaults on again within 90 days is evidence that the plan was not adequately designed for that customer’s actual financial capacity. High repeat default rates on payment plans suggest either inadequate affordability assessment at the plan-setting stage or plans structured for the lender’s collection convenience rather than the customer’s ability to pay, both of which create Outcome 1 and Outcome 6 concerns.

The Vulnerable Customer Challenge in Collections

This is the area of TCF compliance that is evolving fastest in 2025 and 2026, and where most South African collections operations have the widest implementation gap.

In March 2024, the FSCA published its Statement on Consumer Vulnerability, formally embedding consumer vulnerability within the TCF framework and setting out a three-phase implementation timeline running through 2028. Phase 1 (2024-2025) focused on stakeholder consultation and awareness. Phase 2 (2025-2027) embeds vulnerability within supervisory practices and issues formal guidance and Conduct Standards. By 2026, the expectation that regulated financial institutions have documented vulnerability identification and handling protocols is transitioning from a best-practice recommendation to a supervisory requirement.

The FSCA’s Vulnerability Statement acknowledges the South African context explicitly. With 49.2% of the adult population living below the upper bound poverty line, high unemployment, and low financial resilience as structural realities, South African collections operations are working with a borrower population where vulnerability is not an edge case. It is a material segment of the portfolio.

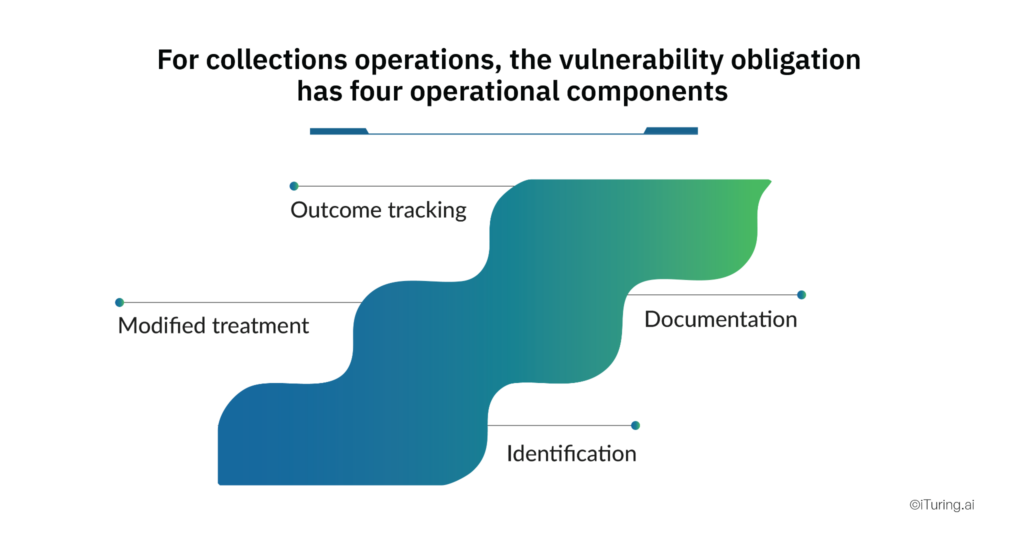

For collections operations, the vulnerability obligation has four operational components:

Identification. Vulnerable customers do not self-identify. Collections operations must use a combination of proactive screening (account data signals), behavioural signals (erratic payment patterns, unusual communication behaviour), and self-disclosure triggers (a customer who mentions job loss, illness, or a bereavement during a collections call should be flagged immediately). An AI collections system with behavioural analysis capability can identify financial stress signals from transaction data 30 to 45 days before they become visible in repayment behaviour, creating an earlier intervention window.

Modified treatment. Once identified as vulnerable, a customer must not be subject to the standard collections contact strategy. Aggressive contact cadences, escalation to legal collections, and automated-only communication channels are not appropriate for a vulnerable customer. Modified treatment typically includes paused escalation, extended payment plan terms, referral to the lender’s financial counselling service, and increased frequency of human agent contact.

Documentation. The FSCA will ask, during a conduct examination, how many vulnerable customers were identified in the most recent quarter, what modified treatment they received, and what outcomes they achieved compared to the standard collections population. Without documented identification and handling records, the institution cannot demonstrate compliance regardless of how well the protocol was designed.

Outcome tracking. The ultimate test of a vulnerable customer protocol is whether vulnerable customers achieve better outcomes: higher payment plan success rates, lower legal escalation rates, and lower complaint rates than they would have received through the standard process. Institutions that have implemented effective vulnerability protocols consistently report that early identification and modified treatment reduces legal escalation costs as well as improving customer outcomes.

What the FSCA Examiner Will Check

The FSCA’s conduct examination approach is data-driven and evidence-focused, with the FSCA having explicitly built data analytics capability to enable proactive supervision across its full regulated population. For collections operations deploying AI, the examination now encompasses both the outcomes the operation produces and the enterprise ai governance structure that ensures those outcomes are governed, monitored, and capable of being evidenced on demand.

The documentation checklist covers:

- TCF outcome measurement framework: A documented framework defining which metrics the institution tracks for each of the relevant TCF outcomes in collections, with defined targets and review frequencies

- Monthly and quarterly management information reports: Actual data showing complaint rates, resolution times, vulnerable customer handling outcomes, and payment plan performance over the examination period

- Board reporting evidence: Minutes or resolutions showing that the board or a board committee has received and reviewed collections TCF metrics on a quarterly basis

- Root cause analysis records: For every period where a TCF metric fell below target, documented root cause analysis and the corrective action taken

- Vulnerable customer handling evidence: Records of customers identified as vulnerable, the modified treatment applied, and the outcomes achieved

- Model validation records: Documentation showing that every AI model influencing collections decisions was validated for accuracy, consistency, and disparate impact before deployment, and that ongoing ai governance monitoring is in place to detect performance changes in production

- Staff training records: Evidence that collections staff are trained in TCF principles, with training completion rates and assessment scores

An institution that can produce this documentation in a structured, examination-ready format at short notice is demonstrating precisely the kind of embedded TCF culture that Outcome 1 requires. An institution that reconstructs documentation from scattered records during the examination is demonstrating the opposite.

AI Collections and TCF: The Opportunity

The operational synergy between AI-powered collections and TCF compliance is direct and significant. An AI collections deployment built on a model governance foundation generates the evidence TCF examinations require as a by-product of normal operations, without additional manual reporting effort.

Vulnerable customer detection. An AI system analysing transaction data can identify financial stress indicators: declining balances, accelerating minimum payments, irregular income patterns, weeks before they manifest as a missed payment. This earlier identification window allows the institution to move a customer to modified treatment before their vulnerability becomes acute. Earlier intervention consistently produces better outcomes for both the customer and the lender.

Contact strategy optimisation reduces complaint risk. A significant proportion of Outcome 1 complaints in collections originate from contact frequency: customers who feel over-contacted, contacted at inappropriate times, or contacted through channels they find intrusive. An AI contact strategy engine that optimises contact timing, frequency, and channel based on individual response behaviour reduces complaint risk systematically, for each customer individually rather than just on average.

Payment plan optimisation. AI-powered payment plan tools can model what instalment amount a customer can realistically sustain based on their cash flow profile, rather than offering a standard plan based on the lender’s recovery preference. Plans calibrated to the customer’s actual capacity have materially lower repeat default rates, directly improving the TCF metric that most directly measures whether post-sale barriers are unreasonable.

Model governance and model validation as TCF evidence. A model governance framework that enforces model validation before every production deployment provides the FSCA examiner with direct evidence that AI-driven decisions were tested for fairness, consistency, and accuracy before they affected any customer. Combined with ongoing ai governance monitoring that tracks model performance in production, this framework closes the loop between pre-deployment governance and live outcome measurement.

Automated TCF reporting. Every interaction, decision, and outcome in an AI collections system is logged automatically. The management information reports that an FSCA examiner expects can be generated directly from the platform’s data: complaint rates, resolution times, vulnerable customer identification rates, and payment plan outcomes, without manual compilation that introduces delay and error.

How iTuring Addresses This

iTuring’s collections platform is built with TCF outcome measurement as a core operational component, supported by model governance, model validation, ai governance monitoring, and enterprise ai governance as integrated platform capabilities rather than separate processes.

The platform’s management information dashboard tracks all five core collections TCF metrics in real time: complaint rate, resolution time, vulnerable customer identification rate, payment plan approval rate, and repeat default rate, with configurable target thresholds and automatic alerts when metrics move outside acceptable ranges. That is the ai governance monitoring layer that makes TCF evidence continuous rather than point-in-time.

Model validation runs automatically before every model version goes into production, covering accuracy, disparate impact, and stability checks. The model governance framework records every validation outcome, model version, and change approval against the model inventory, giving examiners a complete audit trail from model development through to customer outcome.

The responsible ai framework embedded in the platform governs which automated decisions require human review, how explanation requests are handled, and how the outcomes of those reviews are recorded, aligning with both TCF Outcome 1 (fair culture) and TCF Outcome 6 (no unreasonable barriers). Enterprise ai governance reporting aggregates model governance records, ai governance monitoring alerts, and TCF outcome data into a single quarterly board pack in the format FSCA examination expectations require.

For compliance heads preparing for their next conduct examination, iTuring offers a TCF outcome measurement audit that benchmarks your current collections data against the FSCA’s examination documentation requirements and identifies the gaps.

Regulatory Disclaimer

The information in this blog is provided for general informational purposes only and does not constitute legal, compliance, or regulatory advice. TCF obligations for South African financial institutions are governed by the Financial Sector Regulation Act 9 of 2017, the FSCA’s TCF framework and guidance, the Conduct Standard for Banks issued under the Financial Sector Laws Amendment Act, the FSCA’s Statement on Consumer Vulnerability (March 2024), and applicable Conduct Standards. The FSCA’s TCF supervisory approach continues to evolve, including through Phase 2 of the Consumer Vulnerability implementation (2025-2027). South African financial institutions should monitor FSCA publications and consult qualified legal and compliance counsel to ensure current TCF compliance. iTuring’s stated capabilities and performance metrics are based on platform design and client implementations; results may vary depending on institutional configuration and data environment.