TL;DR

- NCA Section 81 mandates a three-part affordability assessment before any credit agreement

- Reckless credit findings can result in suspension of consumer obligations or forfeiture of interest

- Self-reported income has high error rates; AI bank statement analysis uses actual cash flow data

- AI reduces loan approval turnaround time by 40-70% while improving assessment consistency

- NCA-compliant AI models must be explainable, consistent across similar applicants, and documented

In March 2026, the Webber Wentzel case law tracker published an update on a judgment that clarified a credit provider’s obligations under Section 81 of the National Credit Act to assess whether a consumer can actually afford the credit being offered. The court’s finding was unambiguous. The affordability assessment is a substantive obligation, and a credit provider that processes one without genuinely assessing affordability has satisfied nothing at all.

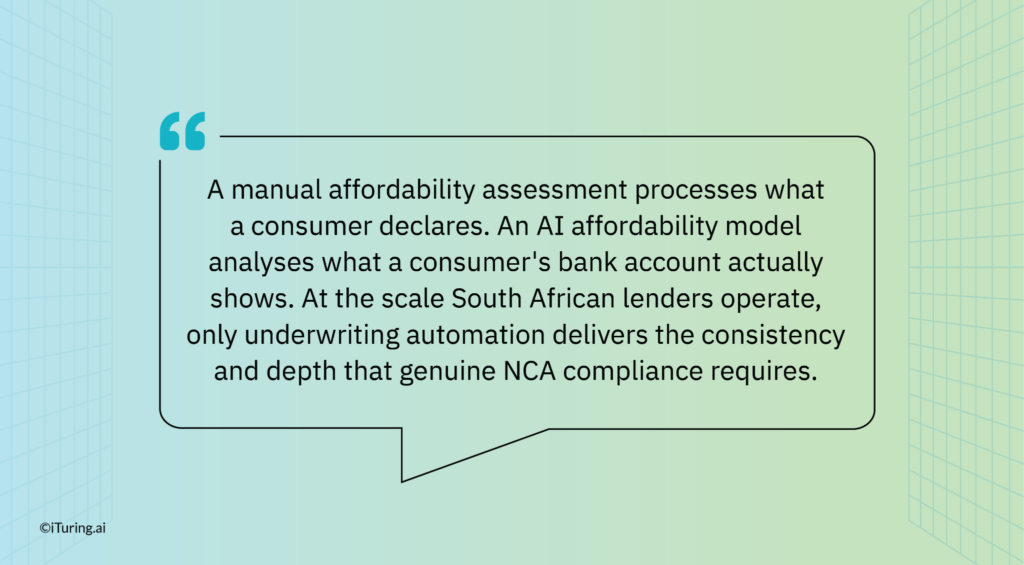

This tension sits at the centre of every AI-powered credit risk decisioning deployment in South Africa. The National Credit Act requires a real assessment: verified income, documented obligations, and a forward-looking discretionary income calculation that determines whether the consumer can genuinely service the proposed commitment. Manual assessments provide procedure without depth, a 30-to-60-minute interview that relies largely on what the consumer self-reports, which is consistently less accurate than what their bank account actually shows. AI-powered credit risk decisioning using machine learning and bank statement analysis can provide genuine depth at scale, but only if the models are built to satisfy what the NCA actually requires, not just to automate the surface steps of a manual process.

This post maps exactly what the NCA requires for affordability assessments, where manual assessments fail, and how AI-powered models satisfy the legal requirements while delivering material improvements in decision quality and processing speed.

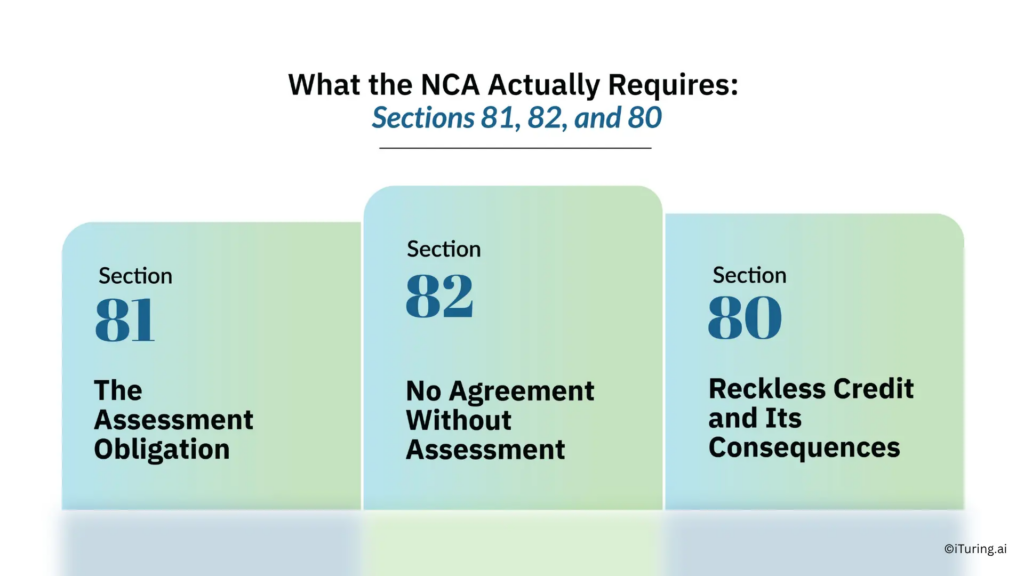

What the NCA Actually Requires: Sections 81, 82, and 80

Understanding what the NCA demands before deploying any affordability model is non-negotiable. The legal framework has three interconnected components.

Section 81: The Assessment Obligation

Section 81 of the NCA imposes a mandatory obligation on every credit provider to take reasonable steps to assess, before entering into a credit agreement:

- The consumer’s general understanding of the risks, costs, and obligations under the proposed credit agreement

- The consumer’s debt repayment history

- The consumer’s existing financial means, prospects, and obligations

Regulation 23A, which operationalizes Section 81, structures this as a three-part assessment. The first leg determines whether the affordability obligation applies to the transaction. The second leg assesses the consumer’s discretionary income, and the credit provider must take practicable steps to determine what the consumer actually earns after fixed commitments. The third leg calculates the consumer’s existing debt obligations drawn from their credit bureau profile.

The NCR expects credit providers to document what was assessed and how the conclusion was reached. A tick-box form without substantive analysis falls short of “reasonable steps”, and the NCR’s examination approach has become progressively more rigorous in testing whether credit providers’ assessment processes produce genuinely fair and objective outcomes.

Section 82: No Agreement Without Assessment

Section 82 reinforces the Section 81 obligation explicitly: a credit provider must not enter into a credit agreement without first completing the required assessment. There is no de minimis exception for small loans. There is no exception for repeat customers. The obligation applies to every credit agreement within the NCA’s scope.

Section 80: Reckless Credit and Its Consequences

Section 80 defines reckless credit as credit granted in three circumstances: where the credit provider failed to conduct an affordability assessment at all, where the assessment was conducted but the consumer did not understand the agreement, or where the assessment showed the consumer could not afford the credit and the lender extended it anyway.

The consequences are severe. Under Section 83 of the NCA, if a court or the National Consumer Tribunal finds that a credit agreement was reckless, it may suspend the consumer’s obligations under the agreement, reduce the outstanding balance, or restructure repayment terms. In the most serious cases, where the credit provider has repeatedly failed its Section 81 obligations or uses models that do not produce fair and objective assessments, the NCR may apply to have the credit provider required to overhaul its entire assessment methodology.

For lenders deploying AI credit risk decisioning models, Section 80(2) makes clear that the question of recklessness is assessed at the time the agreement was made. A lender cannot argue that the consumer’s subsequent financial behaviour was unforeseeable if a properly conducted assessment would have flagged the risk at origination.

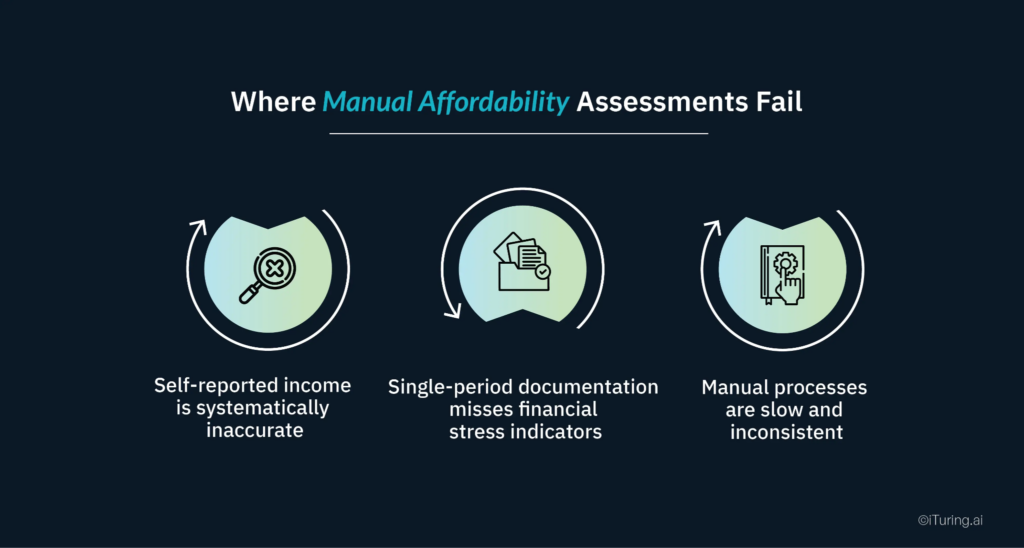

Where Manual Affordability Assessments Fail

A traditional manual affordability assessment at a South African bank or NBFC looks like this: the consumer completes an application form, declares their gross income, lists their known monthly obligations, and submits supporting documents, typically one month of payslips and one month of bank statements. A credit officer reviews the submission, checks it against bureau data, and makes a decision.

This process has three structural weaknesses that AI-powered assessment directly addresses.

Self-reported income is systematically inaccurate. Consumers underreport variable income, forget small recurring obligations, and, not always dishonestly, present their best financial month rather than their typical one. A single payslip does not reflect the reality of a consumer with irregular commission income, gig economy earnings, or informal income supplementing formal employment. An AI bank statement analyser examining six months of transactions sees the actual income pattern, not the declared one.

Single-period documentation misses financial stress indicators. AI bank statement analysis identifies early warning signals that often appear 30 to 60 days before EMI defaults: patterns like declining savings balances, increasing minimum payment behaviour on existing accounts, or cash withdrawal acceleration that suggests the consumer is managing a cash flow problem outside the formal system. A single payslip and a month of bank statements cannot surface these patterns. Six months of transaction-level data analysed by a machine learning model can.

Manual processes are slow and inconsistent. A manual affordability assessment takes 30 to 60 minutes per application when conducted properly. At scale, this creates pressure to abbreviate the process, which is how assessments become tick-box rather than substantive. Two different credit officers reviewing the same application may reach materially different conclusions based on their individual judgment. Underwriting automation reduces turnaround time by 40 to 70% while enforcing consistent credit risk decisioning logic across every application. The NCR’s expectation that similar applicants receive similar treatment is structurally satisfied by a consistent model in a way that a human-led process cannot guarantee.

What AI Affordability Models Actually Predict

There are two distinct predictive problems in affordability assessment, and the NCA’s obligation addresses both differently.

Probability of default asks: will this consumer miss a payment within the next 12 months? This is a credit risk scoring exercise grounded in backward-looking repayment behaviour. A consumer can have a very low probability of default, because they have never missed a payment in their life, and still be unaffordable for a specific new credit agreement if the new obligation would cause financial distress. Probability of default is a necessary input into credit risk scoring, but alone it does not answer the NCA’s Section 81 question.

Affordability stress asks: will this consumer experience material financial distress if this credit agreement is entered into? This is the NCA’s actual question. It is forward-looking, drawing on current income, existing obligations, and the incremental commitment the proposed credit would add. A consumer’s probability of default and credit risk scoring profile are inputs into this prediction, but the primary driver is whether their verified discretionary income can absorb the new obligation without pushing them into financial distress.

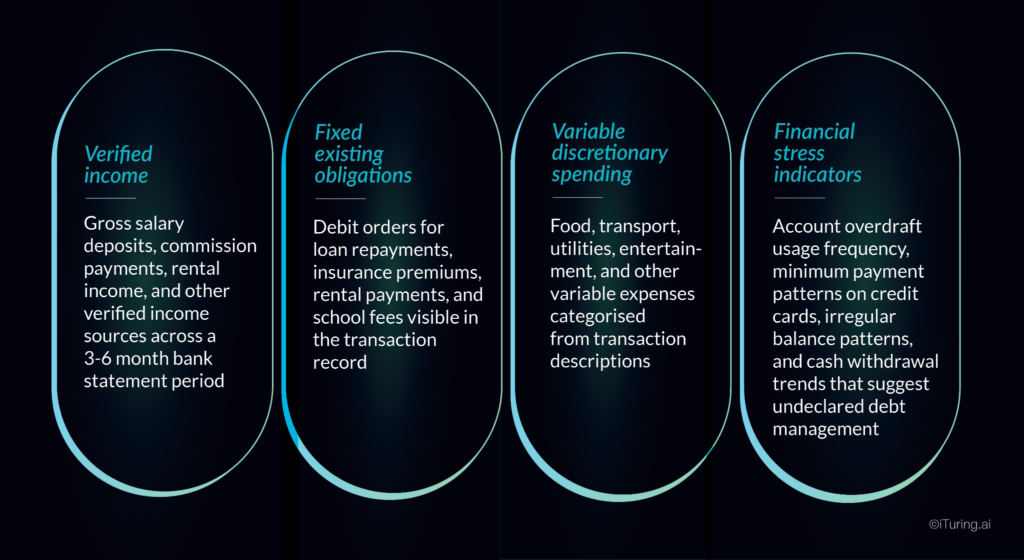

A NCA-compliant AI credit risk decisioning model must address the affordability stress question directly. The input signals that matter most are:

The model’s output must be calibrated conservatively. Given the consequences of a reckless lending finding under Section 80, an AI model calibrated to approve borderline cases, prioritising approval rates over credit quality, creates precisely the systemic risk that the NCA’s reckless credit provisions were designed to prevent.

NCR Compliance Requirements for AI Affordability Models

Deploying an AI affordability model creates specific compliance obligations beyond the substantive assessment requirements.

Explainability for declined applications. When a credit application is declined, the consumer has a right under the NCA to know why. For an AI credit risk decisioning model, this means the model must generate a plain-language explanation for every declined decision: the application was declined because the assessed discretionary income of R3,400 per month is insufficient to service the proposed monthly instalment of R2,100 given existing documented obligations of R4,800 per month. A black-box model that produces a decline without a traceable explanation does not satisfy NCA requirements.

Consistency across similar applicants. The NCR has made clear that credit providers’ assessment models must not produce discriminatory outcomes. An AI model must be tested for disparate impact, whether it produces materially different approval rates for applicants of similar financial profiles across demographic groups. If the NCT finds a credit provider customarily uses models that do not result in fair and objective assessments, it can require a complete methodology overhaul on application by the NCR. Disparate impact testing is a core component of model validation for any AI affordability deployment: it is the mechanism by which a lender demonstrates the “fair and objective assessment” the NCA requires.

Model validation and the audit trail obligation. Every affordability assessment must be documented: the inputs used, the model version that produced the output, and the decision reached. If the NCR or a court reviews a specific credit agreement for potential recklessness, the lender must reconstruct exactly what assessment was conducted at the time the agreement was made. Model validation must be completed before any new model version goes into production, and version control records must be retained for NCR examination. This makes model validation a regulatory compliance requirement, not a data science best practice.

Data accuracy: the source verification obligation. The accuracy obligation under both Section 81 and POPIA’s information quality condition requires that data inputs to the affordability model are verified where possible, not merely accepted on consumer declaration. Bank statement analysis provides that verification: it replaces what the consumer says they earn with what their account demonstrates they receive.

Implementation Reality for South African Lenders

Deploying an NCA-compliant AI affordability model involves three integration layers, and underwriting automation only delivers its full compliance and efficiency benefit when all three are connected.

Bank statement API connectivity. South Africa’s open finance infrastructure is progressively enabling lender access to consumer bank data with appropriate consent. For lenders not yet connected to bank statement APIs, PDF bank statement upload with AI-powered data extraction provides an interim solution that is sufficient for the model’s analytical requirements.

Credit bureau integration. The three-leg Regulation 23A assessment requires bureau data for existing obligation verification. Integration with TransUnion, Experian, or Compuscan (now Credifin) is a baseline requirement for any NCA-compliant affordability model.

Loan origination system integration. The credit risk decisioning model must sit inside the credit origination workflow, receiving data from the origination system, returning a decision with an explanation, and writing a complete audit record back to the origination system’s case file. A standalone model that produces a score without workflow integration does not satisfy the documentation requirement.

Deployment timeline. For lenders implementing an AI affordability model on an existing platform, deployment typically takes 2 to 4 weeks for a pre-built, NCA-calibrated model. Custom model development, trained on the lender’s own historical portfolio data, takes 8 to 12 weeks from data extraction to production deployment and typically produces meaningfully better predictive performance because it is calibrated to the specific borrower population the lender serves.

How iTuring Addresses This

iTuring’s NCA affordability assessment module integrates bank statement analysis, bureau data, and machine learning-based discretionary income calculation into a single credit risk decisioning workflow. Every decision carries a plain-language explanation satisfying the NCA’s decline explanation requirement. Model validation runs automatically against every model version, including disparate impact checks across demographic groups, before any version goes into production. The full assessment audit trail covering inputs, model version, output, and explanation is stored against every application for NCR examination.

Probability of default and credit risk scoring outputs are available as supplementary signals within the same decisioning workflow, giving credit teams a complete view of both backward-looking repayment risk and forward-looking affordability stress in a single decision record. The model is calibrated conservatively by default, prioritising the lender’s protection from reckless lending findings over approval rate optimisation. Custom calibration is available for lenders who have validated their risk appetite against their portfolio data.

For Chief Risk Officers evaluating AI affordability assessment for the first time,

Regulatory Disclaimer

The information in this blog is provided for general informational purposes only and does not constitute legal, compliance, or regulatory advice. Affordability assessment in South Africa is governed by the National Credit Act 34 of 2005, Regulation 23A of the National Credit Regulations, and related NCR guidance including the NCR’s Guidelines for Affordability Assessment. The consequences of reckless credit granting are determined under Sections 80 to 84 of the NCA. AI affordability models are subject to the NCA’s fair and objective assessment requirement, POPIA’s data processing conditions, and the FSCA’s TCF framework. Regulatory requirements evolve, and recent case law continues to develop the interpretation of Section 81 obligations. South African credit providers should consult qualified legal counsel before deploying AI affordability assessment models. iTuring’s stated capabilities and performance metrics are based on platform design and client implementations; results may vary depending on lender-specific data environments and portfolio characteristics.