TL;DR

- NCA Section 129 governs every enforcement notice before collections action

- Debt review status must be checked in real time before every contact attempt

- POPIA requires lawful basis and explainability for every AI data processing activity

- Credit providers bear full accountability for all AI collections actions taken on their behalf

- August 2025 proposed NCA amendments tighten bureau data accuracy obligations

Consider a traffic intersection that was recently upgraded with new signals, new turning restrictions, and new pedestrian priority rules. The cars using it are newer and faster than before. Some have advanced driver assistance systems. But the updated intersection rules apply to the assisted driver with exactly the same force as to the manual one. An automated system that does not know about the new turning restrictions will execute what looks like a smooth, confident manoeuvre directly into a violation.

South Africa’s credit collections landscape is that intersection in 2026. The National Credit Act 34 of 2005 (NCA), the Protection of Personal Information Act (POPIA), the August 2025 proposed amendments to the National Credit Regulations, and the FSCA’s Treating Customers Fairly framework have collectively redefined the rules that every AI collections system must navigate, automatically and correctly, on every contact attempt. The cars are faster. The rules are stricter. And unlike a human driver who can read a new road sign and adjust in real time, an AI platform that was not engineered for the current rule set will continue executing the old logic at scale until someone intervenes.

This blog is a practical guide for South African credit providers evaluating or operating AI collections infrastructure in 2026. It maps the NCA requirements that directly govern collection activity, the POPIA obligations that apply to every data processing event in the collections workflow, the NCR registration framework, and what a genuinely compliant AI collections platform looks like operationally.

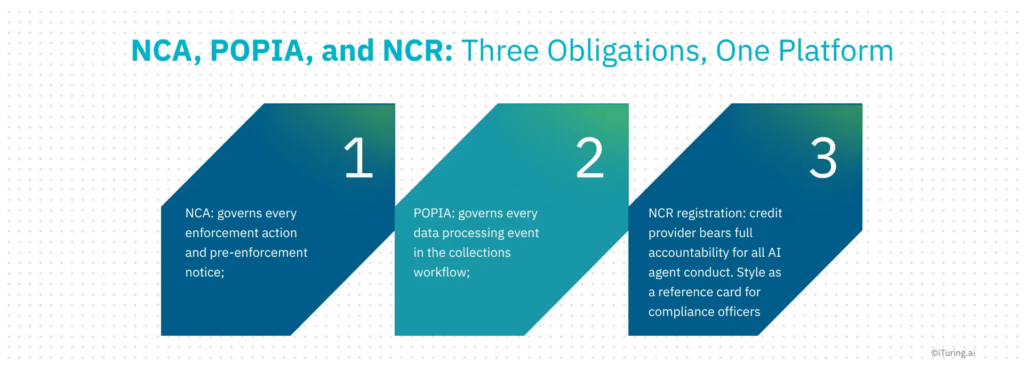

The NCA Framework: What Governs AI Collections

The National Credit Act 34 of 2005 is the primary statute governing all credit and collections activity in South Africa. Its reach extends to every agreement that qualifies as a credit agreement under the Act, covering banks, registered credit providers, retailers offering credit terms, and debt collection firms acting on their behalf.

For AI collections operations, four provisions of the NCA create direct operational obligations.

Section 129(1)(a): The Pre-Enforcement Notice Requirement

Before a credit provider can take enforcement steps on a defaulted credit agreement, it must first send a written notice to the consumer. That notice must inform the consumer of the default, the nature and extent of the outstanding obligation, and the consumer’s rights to approach a debt counsellor, an alternative dispute resolution agent, consumer court, or ombud with jurisdiction before any enforcement action begins.

This is a mandatory pre-enforcement gate. An AI collections system that escalates to enforcement workflows, initiates legal referrals, or triggers external debt collection action without first completing this notice and allowing the prescribed response window to pass is in breach of the NCA regardless of the accuracy of the underlying model.

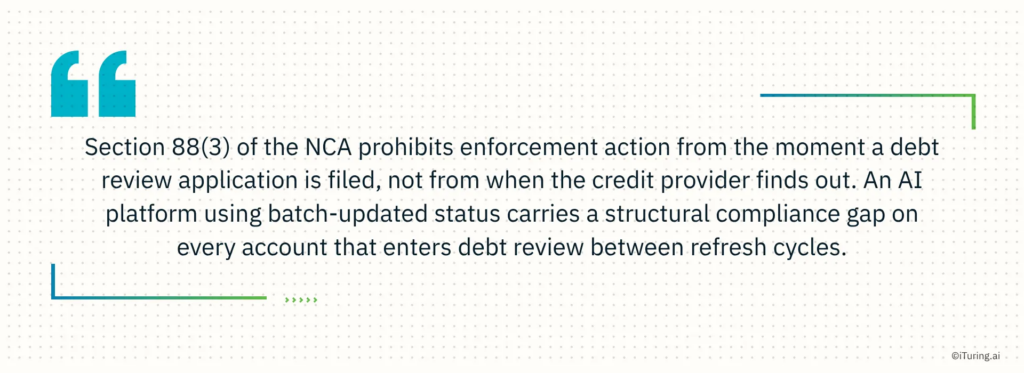

Section 86: Debt Review and the Section 88(3) Prohibition

Section 86 of the NCA allows over-indebted consumers to apply for debt review through a registered debt counsellor. Once an application has been filed, Section 88(3) prohibits credit providers from taking enforcement action on the affected obligations. The prohibition begins at the moment the application is made, not at the moment the credit provider becomes aware of it.

This is the most operationally demanding NCA compliance requirement for AI collections systems, precisely because of the timing gap. A consumer who files for debt review at 8 AM is protected from that moment forward. An AI platform that runs its debt review registry check as a nightly batch job at midnight will have no record of this consumer’s protected status when it initiates outreach at 9 AM. Every contact attempt made in that window is a Section 88(3) violation. The only technically sound response to this requirement is a live API connection to the NCR’s debt review registry, queried before every individual contact attempt.

Section 80: Reckless Credit and Collections Exposure

Section 80 defines reckless credit as credit granted without a proper affordability assessment, credit granted to a consumer who did not understand the agreement, or credit extended despite the assessment showing the consumer could not afford it. For AI collections teams, the relevance of Section 80 is downstream: if a consumer or their debt counsellor raises a reckless credit challenge on an account in collections, the credit provider must be able to produce the original affordability assessment record. AI collections models that are scoring accounts without flagging potential reckless credit exposure are missing a governance signal that may affect recovery strategy on those accounts.

August 2025 Proposed NCA Regulation Amendments

In August 2025, the Department of Trade, Industry and Competition published proposed amendments to the National Credit Regulations. The amendments tighten data accuracy obligations for bureau reporting, expand the scope of information credit providers must submit to registered credit bureaus, and strengthen affordability assessment documentation standards.

For AI collections models that use bureau data as input features, the practical implication is clear: the accuracy of those inputs must be monitored against the updated standards. A model receiving bureau data that does not meet the revised accuracy thresholds is generating predictions from inputs the NCA may no longer consider reliable.

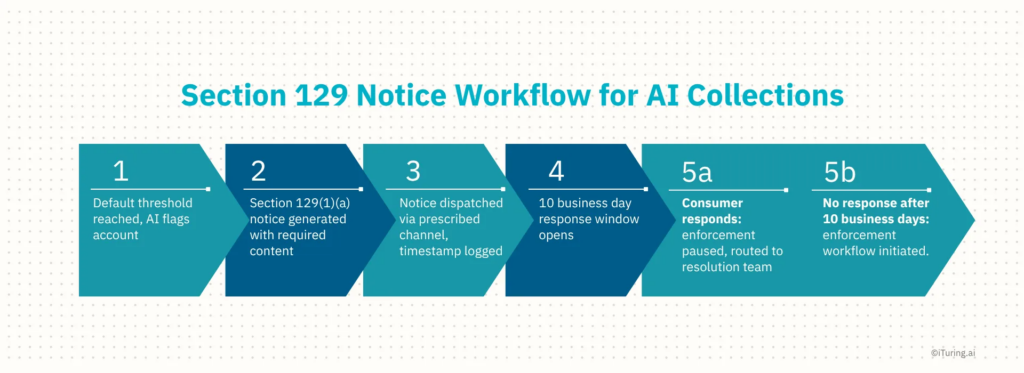

The Section 129 Notice Workflow in AI Collections

The Section 129(1)(a) notice requirement is the single most important pre-enforcement gate in the NCA for AI collections operations. Getting it right demands precise workflow automation, not a general policy statement that notices are sent before enforcement.

A compliant Section 129 notice must contain: the name of the credit provider, the nature of the credit agreement, the consumer’s account reference, the total amount outstanding, the nature and duration of the default, a statement of the consumer’s rights to refer the matter to a debt counsellor or dispute resolution forum, and the credit provider’s contact details for response.

The AI collections platform must:

- Identify the enforcement threshold for each account type under the relevant credit agreement terms

- Generate the notice with all legally required content fields populated correctly from account data

- Dispatch via the channel specified in the credit agreement or, where not specified, in a manner likely to bring it to the consumer’s attention

- Log the dispatch date, channel, and notice reference with a timestamp

- Start the 10 business day response window from the confirmed dispatch date

- Monitor the response window daily and flag when it closes without consumer response

- Route any consumer response received within the window to the credit provider’s resolution team and pause enforcement activity on the account

The response handling step is where many AI collections platforms create a gap. The notice generation and dispatch are typically well-automated. But if the consumer responds and the response is not detected and acted on within the window, the platform may proceed to enforcement on an account where the consumer exercised their NCA rights. The response monitoring must be as automated and as real-time as the notice generation itself.

Debt Review: Why Real-Time Status Checking Is Non-Negotiable

Section 88(3) of the NCA is precise and unambiguous: once a consumer has filed a Section 86 debt review application, enforcement action is prohibited. The prohibition does not wait for the credit provider to be notified. It begins at the moment of filing.

This creates a compliance architecture requirement that has no workaround other than real-time registry access. Consider the practical scenario. A credit provider runs a collections campaign across 50,000 accounts daily. The NCR debt review registry is refreshed via a nightly batch integration at 11 PM. Between 11 PM and the following 11 PM, any consumer in that portfolio who files for debt review is effectively invisible to the AI system. If 200 consumers file debt review applications on a given day, and the AI contacts each of them before the next batch refresh, that is 200 Section 88(3) violations in a single day’s operations.

The only compliant solution is a live API connection to the NCR debt review registry, queried at the account level before every individual contact attempt is authorised. This is not an optimisation. It is the technical minimum required to satisfy the Act.

When debt review status is confirmed, the AI system must immediately:

- Flag the account as debt review protected

- Remove it from all active outreach queues across all channels

- Generate an internal alert for the credit provider’s debt counsellor coordination team

- Log the status change with timestamp and data source reference

POPIA Compliance for AI Collections

The Protection of Personal Information Act came into full effect in July 2021. For AI collections operations, POPIA operates alongside the NCA as a parallel compliance framework that governs how consumer data is collected, processed, stored, and used at every stage of the collections workflow.

Lawful basis for data processing

Every category of consumer data used by the AI collections system must have a documented lawful processing condition under POPIA’s Section 11. For core collections activity, the credit agreement typically provides the contractual necessity basis: processing is necessary to perform the agreement. For behavioral data, third-party data, or any category not directly required by the credit agreement, explicit consent or another Section 11 condition must be documented and maintained.

Purpose limitation

POPIA’s purpose specification condition requires that data is processed only for the purpose for which it was collected or for a compatible purpose. Consumer data collected during credit origination cannot be automatically repurposed for AI-driven propensity-to-pay scoring in collections without a separately documented basis. The purpose for which data was originally processed constrains every downstream use. For AI collections models that ingest data from multiple origination-era sources, this requires field-level documentation of the lawful basis for each data category.

Data subject rights

Under POPIA, consumers are data subjects with specific, enforceable rights. For AI collections operations, three rights create direct operational requirements:

- Right of access: A consumer can request a summary of the personal data being processed about them, including the data being used in their collections scoring. The AI platform must support this request technically.

- Right to correction: If a consumer disputes the accuracy of data the AI system is using, the platform must support a correction workflow. A system that continues scoring on contested data without a correction process in place is creating dual exposure under POPIA and the NCA’s data accuracy obligations.

- Right to object: A consumer can object to processing on legitimate grounds. For collections AI, an objection to automated scoring does not automatically remove the credit agreement obligation, but it does require the credit provider to consider the objection and respond substantively.

POPIA Section 71: Automated Decision-Making

Section 71 of POPIA creates specific obligations when decisions are made about a data subject solely by automated means and those decisions have legal or similarly significant consequences. A collections contact strategy decision sits within this scope. Being placed in a high-intensity collections contact sequence, being referred to an external debt collector, or being recommended for legal action are all decisions with material consequences for the consumer.

Section 71(3)(b) requires that the responsible party provide the consumer with sufficient information about the underlying logic of the automated decision to allow them to make representations. In practical terms, every AI-generated collections prioritisation decision that could materially affect the consumer must be explainable on request, in language the consumer can understand.fairbridges

For AI collections platforms, this means explainability is not a governance nicety. It is a legal obligation that activates each time a consequential automated decision is made.

Operator agreements

Where an AI collections platform is operated by a third party, POPIA classifies that third party as an “operator.” The Act requires a formal written agreement between the responsible party (the credit provider) and the operator specifying the operator’s data processing obligations and the responsible party’s oversight rights. This agreement must be in place before the AI platform processes any consumer data.

NCR Registration and the Credit Provider Accountability Principle

The NCA requires credit providers operating in South Africa to be registered with the National Credit Regulator. This registration covers the credit provider’s full operating perimeter, including collections activity conducted on its behalf by third parties or AI platforms.

The NCA does not create an AI-specific registration category. An AI collections platform operating as an agent for a registered credit provider does not need its own separate NCA registration. What the NCA does require is that the credit provider maintains full accountability for every NCA conduct obligation, regardless of whether the activity is conducted directly or through a third-party platform.

This principle mirrors the LSP accountability framework under India’s RBI Digital Lending Directions: the regulated entity is responsible, the agent is accountable to the regulated entity, and the regulatory consequence lands with the registered credit provider if the AI system violates the Act.

For NCR examination purposes, this means:

- The credit provider must be able to produce evidence of oversight over the AI platform’s NCA compliance

- The agreement with the AI collections vendor must include the credit provider’s audit rights over the platform’s conduct

- The credit provider must maintain documentation of how the AI platform’s compliance with NCA conduct standards is monitored

- Any NCA violation by the AI system is a violation by the credit provider

The NCR’s Annual Performance Plan 2025-28 identifies technology-driven collections and affordability assessment practices as areas of increasing supervisory focus. Credit providers deploying AI collections platforms should expect that NCR examinations will increasingly assess not just outcomes but the governance infrastructure surrounding AI-driven collections activity.thedtic

The FSCA Treating Customers Fairly Overlay

For credit providers who are also licensed by the Financial Sector Conduct Authority, the FSCA’s Treating Customers Fairly (TCF) framework operates alongside the NCA and POPIA as a third compliance layer on AI collections operations.

TCF is outcomes-based. It requires that credit providers demonstrate fair treatment is delivered to customers throughout the product lifecycle, including post-sale servicing and collections. Three of TCF’s six outcomes apply directly to AI collections:

- Outcome 1: Fair treatment must be central to the firm’s culture. The AI collections system must be designed and governed to deliver fair treatment by architecture, not just by policy statement.

- Outcome 4: Products and services must perform as credit providers have led consumers to expect. Collections approaches that deviate materially from the terms disclosed in the credit agreement create TCF Outcome 4 exposure.

- Outcome 6: There must be no post-sale barriers to making a complaint. AI collections systems must surface grievance mechanisms at every consumer touchpoint and must not create friction in the complaint pathway.

TCF requires demonstrability. An AI system that produces reasonable average outcomes does not satisfy TCF if the credit provider cannot show, at the individual account level, how it continuously monitors the system to confirm fair treatment is being delivered. For FSCA-licensed credit providers, this means TCF monitoring is not a separate governance project from AI collections governance. It is the same governance infrastructure applied to TCF’s measurement framework.

The FSCA’s Regulatory Strategy 2025-2028 identifies AI governance as an emerging supervisory priority, with specific focus on institutions’ ability to demonstrate ongoing, evidence-based compliance rather than policy-level compliance assertions.

What an NCA and POPIA Compliant AI Collections Platform Requires

For credit providers assessing their current infrastructure, the following checklist represents the minimum operational standard for NCA and POPIA compliant AI collections in 2026:

- Real-time NCR debt review registry integration, queried via live API before every individual contact attempt, with status changes acted on within minutes not batch cycles

- Section 129(1)(a) notice generation with all legally required content fields, correct dispatch channel logic, 10 business day response window tracking, and consumer response routing capability

- Reckless credit flagging for accounts with potential Section 80 exposure, routed to credit risk review before collections escalation

- Documented lawful processing condition under POPIA Section 11 for every category of consumer data used as a model input

- Purpose limitation controls preventing data reuse beyond the documented processing purpose

- Data subject rights workflows for access, correction, and objection requests, with defined response timelines

- POPIA operator agreement in place with any third-party AI collections vendor, specifying processing obligations and credit provider audit rights

- Section 71 automated decision explainability: every consequential AI collections decision must be explainable in plain language on consumer request

- Bureau data quality monitoring against the August 2025 proposed NCA regulatory amendment standards

- Immutable audit trail for every collections interaction at the account and interaction level, covering all compliance checkpoints and producible for NCR examination without manual reconstruction

How iTuring Approaches This

iTuring is built for the multi-regulatory environment South African credit providers operate in. The platform’s governance architecture addresses the NCA, POPIA, and FSCA TCF obligations described in this blog as integrated infrastructure requirements, not separate compliance modules.

Real-time debt review status checking operates as a mandatory pre-contact gate, integrated via live NCR registry API. Section 129 notice workflow automation includes content validation, dispatch logging, response window tracking, and consumer response routing. Every AI collections model deployed through iTuring carries SHAP and LIME explainability at the individual decision level, satisfying POPIA Section 71(3)(b) without requiring a separate explanation layer.

Continuous monitoring across 60 parameters covers data drift, model performance, output distribution, and compliance guardrail adherence. Disparate impact monitoring across demographic segments is built in as a standard parameter, addressing the South Africa-specific equity obligation that has no equivalent in US or European collections governance frameworks.

One-click examination readiness documentation compiles model governance records, interaction audit trails, and monitoring logs into a package formatted for NCR and FSCA review, producible within hours rather than assembled under examination pressure.

Book a discovery session with iTuring to see how the platform’s compliance infrastructure maps to the NCA and POPIA requirements for your credit provider tier.