TL;DR

- Debt review under Section 86 stops all collections contact immediately

- AI can identify debt review candidates 60 to 90 days early

- Live NCR registry checks must gate every outbound contact attempt

- Early identification reduces legal exposure and improves customer outcomes

- Manual batch checks create unlawful contact gaps AI eliminates

A collections agent pulls up an account on a Monday morning. The consumer has missed two payments, the balance is overdue, and the system flags it for outbound contact. The agent makes the call. What the system did not show is that the consumer applied for debt review the previous Thursday, the debt counsellor issued a Section 86(4)(b)(ii) notice on Friday, and the registry was updated over the weekend. The batch sync runs on Wednesday. Until then, every contact attempt the system generates on that account is unlawful.

Now scale that scenario to an AI collections platform running tens of thousands of contact attempts per day, on a portfolio where new debt review applications come in continuously. The batch gap is not an edge case. It is a structural compliance failure built into every system that does not check debt review status in real time before every contact.

This blog covers two things: how to stop generating unlawful contact with consumers already in debt review, and how to identify consumers heading toward debt review early enough to intervene before the formal application is filed.

What NCA Section 86 Actually Requires

Section 86 of the National Credit Act 34 of 2005 gives an over-indebted consumer the right to apply to a registered debt counsellor for a debt review. The debt counsellor assesses the consumer’s financial position and, if the consumer is found to be over-indebted, proposes a restructured repayment plan to the credit providers involved.

Once the application is accepted and the debt counsellor issues a Section 86(4)(b)(ii) notice to the credit provider, the credit provider must cease all collections activity on the affected accounts. This means:

- No further outbound contact attempts by any channel

- No issuing of summons or demand letters

- No enforcement of existing judgments

- No referral of the account to a third-party collection agency

The legal obligation takes effect from the moment the notice is issued, not from the moment the credit provider’s system is updated. A credit provider whose batch sync runs on Wednesday is still legally required to have stopped contact from the moment the Friday notice was issued. The system’s update schedule is not a legal defence.

Debt review does not extinguish the debt. The consumer remains obligated to repay under the restructured plan supervised by the debt counsellor and, where a court order is obtained under Section 87, by the terms of that order. What it removes from the credit provider is the ability to conduct standard collections activity until the debt review process concludes.

Where AI Collections Systems Fail on Debt Review

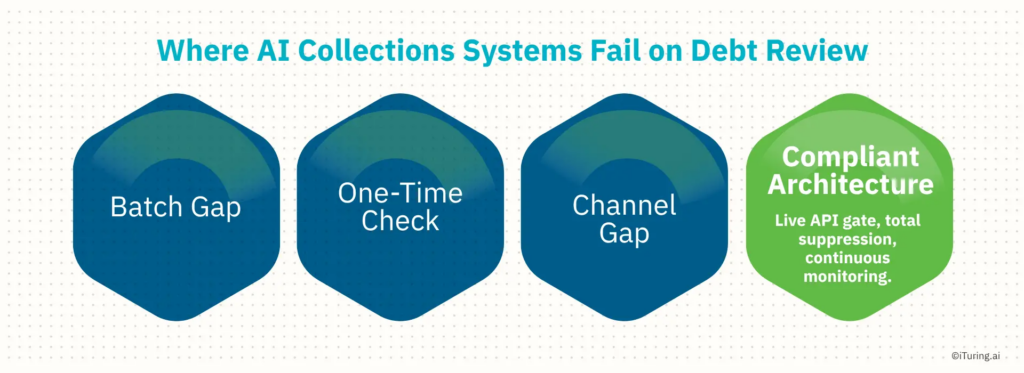

Three failure modes account for the majority of unlawful debt review contact in AI collections operations. Each is a system design problem, not a human error.

Failure Mode 1: Batch Registry Updates

The system pulls NCR debt review registry data on a weekly or fortnightly cycle. A consumer applies for debt review on a Tuesday. The batch runs the following Sunday. The AI contacts that consumer on Wednesday, Thursday, Friday, and Saturday before the batch corrects the record.

At portfolio scale this compounds quickly. A 50,000-account portfolio with a 0.5% monthly debt review entry rate produces approximately 250 new debt review accounts per month. A weekly batch gap means roughly 125 unlawful contact events occur per week on average before the batch update catches up.

Failure Mode 2: Single Onboarding Check

The system checks debt review status once at account onboarding and never again. The consumer books a loan in January and enters debt review in July. No subsequent check exists to catch the change. The account remains in the active contact queue indefinitely.

This is the most common failure mode in legacy collections platforms that predate real-time API availability.

Failure Mode 3: Channel-Specific Suppression

The system suppresses outbound voice calls for debt review accounts but continues to generate SMS and WhatsApp contacts. The NCA does not distinguish between channels. Any contact intended to recover a debt from a consumer in debt review is unlawful, regardless of the channel used. Partial suppression is not compliant.

What AI Can See Before the Application Is Filed

The more valuable capability is upstream. Consumers who are heading toward a formal Section 86 debt review application show clear behavioural signals in their account data 60 to 90 days before the application is filed. An AI model trained on payment behaviour and contact response patterns can surface these signals with enough lead time to change the outcome.

Deteriorating Payment Behaviour

The clearest early signal is a shift in how the consumer is paying, not whether they are paying. Watch for:

- Partial payments replacing full payments over two to three consecutive cycles

- Payment dates shifting progressively later within the payment window each month

- A pattern of minimum payments immediately before the first full missed payment

- Lump sum payments after periods of silence, suggesting the consumer is juggling multiple obligations

Contact Response Changes

A consumer who has historically been responsive and then becomes consistently unreachable is showing a distinct signal. Specific patterns to monitor:

- Answer rate on outbound calls declining over four to six weeks after a stable period

- Promise-to-pay commitments made but not fulfilled across two or more consecutive cycles

- Response time to SMS or WhatsApp messages increasing week on week

Multi-Credit Stress Indicators

Where credit bureau data is refreshed regularly, simultaneous deterioration across multiple credit products is one of the strongest predictors of formal debt review entry. A consumer managing stress on a single account may recover. A consumer showing stress across a personal loan, credit card, and retail account simultaneously is in a different risk category.

The purpose of early identification is not to intensify collections pressure on a struggling consumer. The intervention for an account flagged by the early identification model is a structured financial hardship conversation: an affordability review, a payment arrangement offer, or a referral to the credit provider’s own debt counselling service where one exists. The goal is to find a sustainable repayment path before the consumer reaches the point of filing a formal debt review application.

For the credit provider, the outcome of successful early intervention is a debt that remains in a managed arrangement under the credit provider’s control, rather than moving into a formal debt review process where the repayment structure and timeline are determined by a debt counsellor and potentially a court order.

Technical Requirements for Section 86 Compliance in AI Systems

Four specific system configurations translate the Section 86 obligation into compliant AI operations.

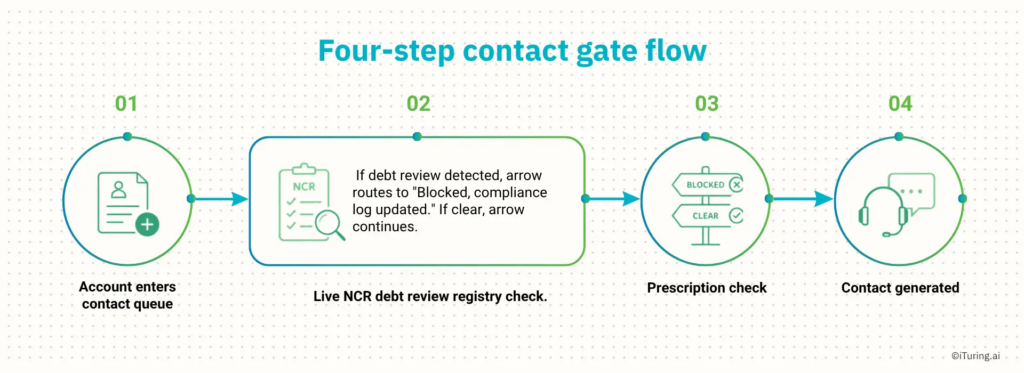

1. Live API Pre-Contact Gate

Every outbound contact attempt must clear a live NCR debt review registry check before the contact is generated. The check must be synchronous with the contact event. The system does not proceed to generate the contact until the registry returns a clear status. No caching, no queuing, no batching at this step.

2. Total Cross-Channel Suppression

When an account returns a debt review status, suppression must apply simultaneously across every contact channel the platform operates: voice, SMS, WhatsApp, email, and in-app push. A single suppression flag must propagate to all channels within the same contact event. Separate suppression lists maintained per channel and reconciled periodically are not compliant.

3. Section 86(4)(b)(ii) Notice Ingestion

The platform must have a documented, tested process for receiving formal Section 86 notices from debt counsellors. On receipt of a valid notice, the account must be suppressed from all AI contact immediately, before the next scheduled contact event. The notice receipt date and time must be logged as part of the account’s compliance record.

4. Timestamped Compliance Audit Log

Every account suppressed due to debt review status must have a complete compliance record showing:

- The date and time the debt review status was first detected

- The contact event that was blocked and the channel it would have used

- The registry status returned at every subsequent contact attempt

- The date and time any formal Section 86 notice was received

This record supports Section 63 annual compliance reporting and any National Consumer Tribunal or court proceeding where unlawful contact is alleged.

Pre-Deployment Checklist

Before deploying AI collections in South Africa, confirm each of the following on debt review compliance specifically:

- Live API connection to NCR debt review registry configured as a hard pre-contact gate

- Gate is synchronous with contact generation, not cached or batched

- Total cross-channel suppression propagates simultaneously across all channels on debt review flag

- Documented process exists for ingesting Section 86(4)(b)(ii) notices with immediate account suppression

- Timestamped compliance log generated for every blocked contact event

- Early identification model trained on payment behaviour and contact response signals

- Intervention workflow defined and active for accounts flagged as early-stage debt review risk

- Section 63 annual compliance reporting mapped to the platform’s suppression and audit log output

Stop the Contact Before the Notice Arrives

The Section 86 compliance obligation has two layers. The first is operational: stop all contact the moment a debt review notice is issued. The second is strategic: identify the consumers heading toward debt review early enough that a different kind of intervention becomes possible.

Getting the first layer right requires live API architecture, not batch processing. Getting the second layer right requires a model that reads payment behaviour and contact response signals continuously, not one that flags accounts only after they have already missed payments and entered formal proceedings.

Both capabilities are available. The collections operations that build them reduce their legal exposure on debt review contact and improve outcomes for consumers who are financially stressed but not yet formally over-indebted.

iTuring’s AI collections platform includes live NCR debt review registry integration as a native pre-contact gate, total cross-channel suppression on debt review detection, and early-stage risk identification models trained on South African portfolio behaviour. [See how it works for SA credit providers.]