TL;DR

- AI collections inherit every NCA obligation of the deploying entity

- NCR registration is mandatory above 100 agreements or R500,000 outstanding

- Debt review status must be checked live before every contact attempt

- NCA rate caps differ by product type and must validate per account

- Prescribed debt must be flagged before any AI contact is generated

Picture a factory floor where every machine runs at full speed, every shift, without a supervisor watching. Output is high. Errors compound invisibly. By the time an audit catches the problem, thousands of faulty units have already shipped. That is what AI collections looks like when compliance architecture is treated as a secondary concern. The contacts go out at scale. The violations accumulate at scale. And the regulator does not distinguish between a mistake made by a human caller and a mistake made ten thousand times by an automated system.

The National Credit Act and the NCR registration framework were written for human-operated collections. The obligations they impose do not disappear when a contact is made by an AI agent. Every obligation that applies to a registered credit provider or debt collector applies equally to the AI system acting on their behalf. What changes is the speed and volume at which non-compliance can occur.

This guide covers who must be registered, what registration requires, and how NCR and CFDC obligations translate into specific operational requirements for AI collections systems in South Africa.

NCR vs CFDC: Which Registration Governs Your AI System

Two separate regulatory bodies govern debt collection in South Africa. Knowing which one applies to your AI deployment determines which compliance obligations you must build into the system.

The National Credit Regulator (NCR) was established under the National Credit Act 34 of 2005. It registers and regulates credit providers, credit bureaus, and debt counsellors. A bank, NBFC, retailer, or fintech that originates credit agreements and collects its own overdue accounts must hold NCR registration as a credit provider.

The Council for Debt Collectors (CFDC) registers third-party debt collection agencies under the Debt Collectors Act 114 of 1998. An agency collecting debt on behalf of another party must hold CFDC registration and comply with the CFDC Code of Conduct.

The AI platform itself does not register under either framework. It operates as an extension of the registered entity and inherits all of that entity’s regulatory obligations. A bank deploying AI to collect its own overdue loan accounts is deploying it as an NCR-registered credit provider. A collection agency deploying AI to work an assigned portfolio is deploying it as a CFDC-registered entity.

Many organisations hold both types of registration or have subsidiaries that do. Clarifying which registration applies to which AI deployment is the starting point for the entire compliance analysis.

NCR Registration: What It Requires

Registration as a credit provider with the NCR is mandatory under Section 40 of the NCA for any entity entering into 100 or more credit agreements per year, or holding an outstanding loan book exceeding R500,000. Below those thresholds, registration is not required, but all NCA conduct obligations still apply to the credit activity.

A registration application requires:

- CIPC company registration documents

- Proof of physical business address

- Certified identity documents for all directors

- Current SARS tax clearance certificate

- A business plan including the entity’s credit policy and affordability assessment methodology

- Financial statements

- Professional indemnity insurance where applicable

Registration is not a one-time step. Conditions of registration require the credit provider to notify the NCR immediately of any material change in directors, address, or business operations, and to cooperate with NCR monitoring and inspection at all times.

An AI collections deployment that materially changes how the credit provider conducts its collections operations warrants a review of whether NCR notification is required under the existing conditions of registration.

Annual compliance reporting under Section 63 of the NCA requires every registered credit provider to submit a compliance report to the NCR within six months of its financial year-end. For organisations running AI collections at scale, that report depends entirely on the quality of the audit trail the AI system generates. The system requirements section below covers exactly what that trail must contain.

What NCR Registration Obligates in Collections

Registration establishes the authority to operate as a credit provider. The NCA then imposes substantive conduct obligations on how that authority is exercised. Four of those obligations apply directly to AI collections operations.

Prohibited Collection Conduct: NCA Section 126

Section 126 prohibits collecting debt extinguished by prescription, collecting after a court has ordered collection to cease, and using misleading, deceptive, or unfair practices in any collections communication. An AI system operating at scale will generate prohibited contacts if these rules are not enforced as hard constraints in its contact eligibility logic.

NCA Rate Caps: Sections 100 to 105

The NCA prescribes maximum interest rates and fees by credit product type. Mortgage agreements, credit facilities, unsecured credit transactions, short-term credit transactions, and developmental credit agreements each carry different caps on interest, service fees, initiation fees, and default administration charges.

An AI-generated demand must apply only the NCA-permitted amounts for the specific product type on the specific account. A template generating a uniform demand structure across all product types, without product-specific cap validation, will produce non-compliant amounts on part of the portfolio at every contact cycle.

Debt Review: NCA Section 86

When a consumer applies for debt review under Section 86 and the application is accepted, the credit provider must cease standard collections contact. Continuing contact through any channel is an NCA violation on every attempt.

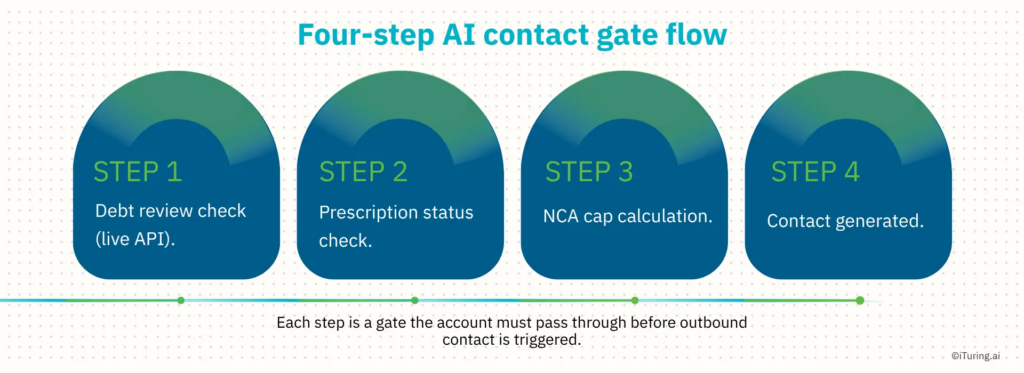

For AI systems, this creates a specific architectural requirement. The system must check each account’s debt review status immediately before every contact attempt. A batch update running weekly or monthly is not sufficient. Debt review applications are filed and accepted continuously. An account that was clear on Monday may be in debt review by Wednesday, and an AI running on a weekly batch will contact that consumer unlawfully until the next update cycle runs.

The only architecture that satisfies this obligation is a live API integration with the NCR debt review registry as a mandatory pre-contact gate, one that the AI must clear before generating any outbound contact for every account on every attempt.

Prescribed Debt

The Prescription Act 68 of 1969 extinguishes most consumer credit obligations three years from the date the debt became due, subject to interruption by a written acknowledgment of liability or by legal process. Contacting a consumer about prescribed debt or issuing a demand for it is an NCA violation.

AI systems must calculate prescription status before generating any contact or demand. The calculation must account for:

- The date the debt first became due

- The date of the last payment

- The date of any written acknowledgment by the consumer

- Whether legal process has interrupted the prescription period

Accounts where the calculation produces a prescription flag must be routed to human legal review rather than the automated contact queue.

The CFDC Layer: Obligations for Collection Agencies Using AI

Third-party agencies operating under CFDC registration are governed by the Debt Collectors Act and the CFDC Code of Conduct. The Code prohibits harassment, threats, contact outside permitted hours, and misrepresentation of the collector’s identity or the debt amount.

The misrepresentation prohibition applies directly to AI agents. An AI voice agent that does not identify itself as automated at the start of a call, or an AI chatbot that allows a consumer to believe they are communicating with a human collector, is generating a Code violation on every such interaction. The prohibition is clear and enforceable today, regardless of whether South Africa has issued specific AI disclosure regulations yet.

CFDC-registered agencies deploying AI must configure their systems to:

- Identify the system as automated at the outset of every contact

- State the name of the registered debt collection agency on whose behalf contact is being made

- Route to a registered human collector immediately when the consumer requests it

- Ensure complaint handling reaches a registered collector and does not remain within an AI queue

Four System Requirements for NCR-Compliant AI Collections

The obligations above translate into four non-negotiable configuration requirements for any AI collections system operating in South Africa.

1. Live Debt Review Registry Integration

The system must connect to the NCR debt review registry via live API and check each account’s status immediately before every outbound contact attempt. This must function as a hard pre-contact gate. No contact is generated until the check returns a clear status. Batch processing does not satisfy this requirement.

2. Product-Type NCA Cap Validation

The demand calculation engine must identify the credit product type for each account and apply the NCA-permitted rate and fee caps for that product type before generating any demand amount. The validation logic must be tested against every product type present in the portfolio.

3. Prescription Date Logic

The contact eligibility engine must calculate prescription status for every account before generating a contact. Accounts where the prescription period has elapsed, or where the calculation is inconclusive, must be flagged and removed from the automated contact queue pending human legal review.

4. Structured Compliance Audit Log

The AI platform must generate a structured, timestamped log for every contact event, recording:

- Account identifier

- Contact date, time, and channel

- Debt review status result from the pre-contact registry check

- Demand amount and NCA product-type cap applied

- Prescription status at time of contact

- Outcome of the interaction

This log is the evidence base for the Section 63 annual compliance report. It must be a native output of the platform on every contact event, not something assembled after the fact from disconnected call recordings and message exports.

Pre-Deployment Compliance Checklist

Before going live with AI collections in South Africa, confirm each of the following:

- NCR registration (credit provider) or CFDC registration (debt collector) is current with all conditions met

- Live API integration with NCR debt review registry is configured as a mandatory pre-contact gate

- NCA rate cap validation is enforced by product type in every AI-generated demand calculation

- Prescription date logic is built into the contact eligibility engine with flagged accounts routed to human legal review

- AI agent identification is configured to disclose automated status at the start of every contact

- Human escalation path is active and routes to a registered human collector on consumer request

- Structured audit log is generated per contact event capturing all fields required for Section 63 reporting

- Annual compliance report process is mapped to the AI platform’s log output

Build Compliance Into the Architecture, Not the Afterthought

NCR registration grants the authority to operate as a credit provider in South Africa. The NCA then governs how that authority is exercised at every step of the collections process. An AI system operating on behalf of a registered entity exercises that authority at a scale and speed that makes compliant architecture a legal requirement, not a configuration preference.

The four system requirements above are the minimum necessary to operate an AI collections platform in South Africa within the bounds of the NCA and the CFDC Code of Conduct.

iTuring’s AI collections platform is built with South African compliance requirements as native architecture. Live debt review detection, product-type NCA cap validation, prescription logic, CFDC-compliant agent identification, and Section 63 audit-ready logging are built in, not bolted on. [See how it works for SA credit providers.]