TL;DR

- Propensity scoring ranks accounts by actual payment likelihood today

- Three separate scores serve three distinct collections routing decisions

- SA-specific signals include month-end salary cycles and debt review status

- Self-cure identification reduces unnecessary contact cost across the portfolio

- NCA and POPIA compliance shape which signals can be used and how

A collections manager at a South African retailer credit provider works a 30-60 DPD portfolio of roughly 8,000 accounts every month. Her current system ranks them by outstanding balance. Her team contacts the highest balances first and works down the list. By month end they have reached about 60% of the accounts. The rest carry over.

Inside that 8,000-account portfolio are three distinct groups of borrower. One group will pay within a few days of month-end salary credit regardless of whether anyone contacts them. One group needs a conversation about a payment arrangement before they will commit to anything. One group has stopped engaging entirely and the account is heading toward the Section 129 process.

Working the portfolio in balance order means the self-cure group receives contact it does not need, consuming budget that produces no additional payment outcome. The arrangement group may or may not be reached before the month runs out, depending on where their balances sit in the queue. The legal-track group receives the same digital outreach as everyone else, producing no outcome and consuming contact resources that could have been directed elsewhere.

Propensity scoring separates these three groups before the first contact is made. This blog covers what propensity scoring is, what signals drive accuracy in South African portfolios, how scoring changes collections economics, and what NCA and POPIA require in the model design.

What Propensity Scoring Is

Propensity scoring assigns each account in a delinquency portfolio a probability estimate for a specific outcome within a defined time window. The score reflects how likely this specific borrower is to produce that outcome given everything the model knows about their behaviour and account state.

Three scores drive collections routing decisions.

Propensity to pay estimates the likelihood of payment within a defined number of days following a specific type of contact. This score determines which accounts should receive active outreach and what treatment intensity is appropriate given the probability of recovery.

Propensity to respond estimates the likelihood that a borrower will answer a call, reply to a message, or engage with outbound contact. This score determines channel selection and contact timing. A borrower with high pay propensity and low response propensity has a channel and timing problem. The willingness to pay is likely present. The ability to be reached is the constraint. The treatment strategy addresses the constraint, not the propensity.

Propensity to self-cure estimates the likelihood of payment without any outbound contact from the collections team. This score determines whether any contact should be made at all in the current cycle. Accounts above the self-cure threshold are removed from the active outreach queue. The payment outcome is maintained at zero contact cost.

These three scores must be maintained separately because each drives a different decision. Collapsing them into a single composite score loses the routing information that makes each one useful. A borrower who scores high on all three needs a simple, well-timed digital payment reminder. A borrower who scores high on pay propensity, low on response propensity, and low on self-cure propensity needs a contact strategy that works around their low reachability. A borrower who scores low on all three needs a specialist referral, not another digital message.

What propensity scoring replaces is the implicit strategy embedded in balance rank, DPD rank, or system export order. All of these apply no information about the borrower’s actual likelihood of paying, responding, or self-curing. They are queue management approaches, not prioritisation strategies. Propensity scoring makes the prioritisation strategy explicit, measurable, and based on the signals that actually predict recovery outcomes.

Balance rank and DPD rank are implicit prioritisation strategies. They apply no information about the borrower’s actual likelihood of paying, responding, or self-curing in the current cycle.

Signals That Drive Propensity in SA Portfolios

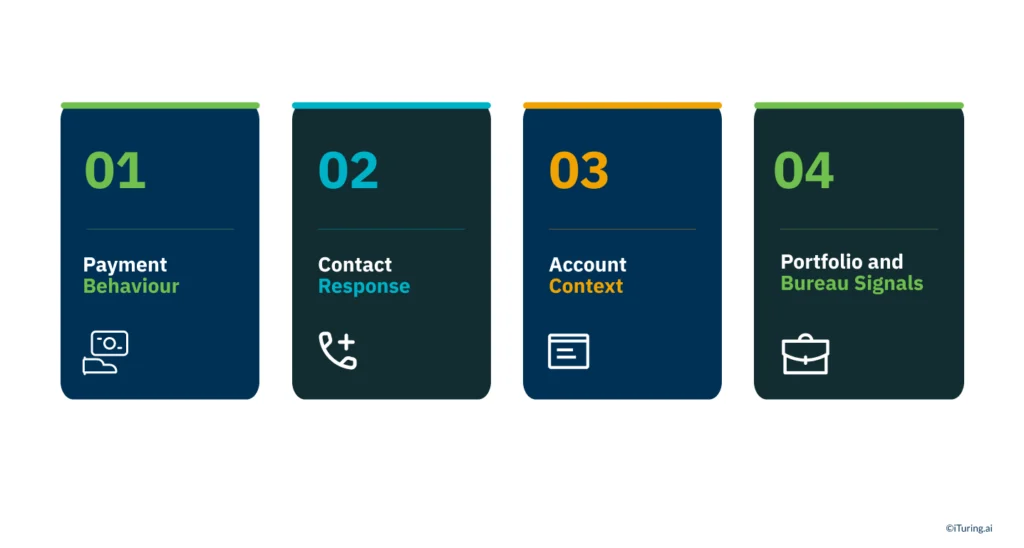

Model accuracy depends on the quality and relevance of the signals used to build it. Four signal categories are most predictive for South African collections portfolios.

Payment Behaviour Signals

Recency, frequency, and trajectory of payments over the last three to six cycles provide the baseline. Within this category, month-end salary credit alignment is a critical signal for South African personal loan and retail credit portfolios. Many borrowers are paid on the last working day of the month. A borrower who has paid within 48 to 72 hours of month-end salary credit for eleven consecutive months and is now ten days into the new month without payment is more likely experiencing a short-term cash flow timing issue than entering a default trajectory. A model that recognises this pattern scores the account differently from one that treats any missed payment date as an equivalent risk signal regardless of the borrower’s salary timing profile.

Self-cure history adds precision. A borrower who has paid at DPD 15 to 20 without any contact in two prior cycles carries a materially higher self-cure propensity than a borrower with no such history. The pattern is the signal.

Partial payment behaviour also carries information. Consistent partial payments indicate financial stress combined with continued intent to service the debt. These accounts are strong candidates for a payment arrangement conversation rather than a standard payment demand.

Contact Response Signals

Historical answer and response rates by channel reflect how this specific borrower engages with outreach. Voice call answer rates, SMS response rates, and WhatsApp response rates are each tracked separately because the relationship between these rates differs substantially across borrower segments in South Africa.

Language preference signals from prior interactions are particularly relevant in the South African context. A borrower whose prior interactions have been in isiZulu, Afrikaans, or Sesotho shows measurably different response rates to contact in those languages compared to English-language contact. Language preference is a response propensity signal, not just a service quality consideration.

Time-of-day and day-of-week patterns from historical successful contacts inform the timing dimension of contact optimisation. PTP fulfilment history is one of the strongest forward-looking signals available: a borrower with a high historical PTP fulfilment rate carries a materially different payment propensity profile from one with repeated unfulfilled commitments, even if their DPD and balance are identical.

Account Context Signals

Credit product type carries its own payment behaviour norms. Personal loans, vehicle finance, retail credit agreements, and home loans each have different payment behaviour profiles, different NCA escalation timelines, and different treatment intensity norms. A model trained across product types without product-type controls will produce less accurate scores for any individual product.

Loan-to-income ratio at origination provides a proxy for underlying repayment capacity that payment history alone does not capture. Geographic location serves as a signal for regional economic conditions, load-shedding impact on digital connectivity, and income seasonality in agricultural regions where payment patterns differ from urban salaried borrowers.

Portfolio and Bureau Signals

Multiple credit agreement exposure is one of the most distinctive signal categories in the South African context. Borrowers frequently carry credit across banks, clothing retailers, furniture retailers, and micro-lenders simultaneously. Simultaneous deterioration across two or more agreements is a materially stronger NPA prediction signal than single-account deterioration. A borrower who is 30 DPD on one account while current on four others presents a different risk profile from a borrower who is 30 DPD on one account and showing early stress signals across three others.

Debt review status from the NCR registry or bureau is a suppression signal rather than a propensity input. Accounts identified as being in debt review under NCA Section 86 are ineligible for outbound contact regardless of their propensity scores. Recent credit enquiries and new account openings serve as signals for cash flow stress or credit-seeking behaviour that may indicate deteriorating financial position ahead of visible DPD changes.

How Propensity Scoring Changes SA Collections Economics

Propensity scoring changes collections economics through three mechanisms: self-cure suppression, treatment differentiation, and legal and specialist referral optimisation.

Self-Cure Suppression

Removing high self-cure accounts from the active contact queue reduces the cost per recovery on those accounts to near zero, because no contact cost is incurred and the payment outcome is maintained. For a South African credit provider with an 8,000-account 30-60 DPD portfolio where 15% carry high self-cure propensity, that is 1,200 accounts that do not need a contact attempt in the current cycle.

At a conservative digital contact cost of R8 to R15 per WhatsApp or SMS attempt, removing 1,200 accounts from the queue over a single cycle saves meaningful contact budget while the payment rate on those accounts is unchanged. Over twelve months, the compounding effect of this saving across every cycle is a material reduction in cost per recovery across the portfolio.

Self-cure suppression also has a borrower experience benefit. A borrower who was going to pay independently and receives three contact attempts before their salary clears is receiving unnecessary friction. That friction carries a relationship cost that is not captured in the contact budget calculation but shows up in customer satisfaction and complaint data.

Treatment Differentiation

Propensity scores allow the collections policy to assign specific treatment types to specific score bands. High propensity accounts receive a digital reminder with a payment link: lowest cost contact, high likelihood of completion without further intervention. Mid propensity accounts receive structured outreach with a payment arrangement offer, with agent-assisted contact where response propensity supports a live conversation. Low propensity accounts are referred to a specialist team or pre-legal process.

The economic gain from treatment differentiation is clearest at the boundaries. High-cost agent contact directed at accounts that would have resolved with a digital reminder wastes both the contact budget and the agent’s capacity. Low-cost digital contact directed at accounts that need a negotiated arrangement produces a contact cost without a recovery outcome. Propensity scoring prevents both of these by directing each treatment type to the accounts where it produces the most value.

Legal and Specialist Referral Optimisation

Legal referral is the highest-cost action in the South African credit provider collections stack. NCA Section 129 notice requirements mean that initiating the legal process involves material process cost before any recovery action can proceed. Propensity scoring directs this cost at accounts where the probability of recovery through legal process exceeds the cost of that process, rather than triggering legal referral by DPD threshold alone.

A DPD-threshold approach to legal referral sends every account that reaches a defined number of days past due into the legal process, regardless of payment propensity, self-cure probability, or debt review status. Propensity scoring filters this population to accounts where legal action is the most productive available intervention, reducing the per-recovery cost of the legal process across the portfolio.

Legal referral is the highest-cost action in the SA credit provider collections stack. Propensity scoring ensures that cost is directed at accounts where legal process produces recovery value, not simply those past a DPD threshold.

NCA and POPIA Constraints on Propensity Model Design

Two regulatory frameworks directly shape how South African propensity models are built, what signals they can use, and how their outputs drive treatment decisions.

NCA Constraints

Debt review status under NCA Section 86 is a hard suppression signal. Accounts identified as being in debt review are excluded from all outbound contact regardless of their propensity scores. The scoring system must check debt review status at the point of scoring, not at the last bureau refresh. Status can change between bureau update cycles. An account that enters debt review between refreshes must be suppressed before the next contact attempt, not at the next batch update.

NCA Section 129 process alignment means the legal referral treatment in the scoring system must respect the mandatory notice and waiting period requirements before any enforcement action can proceed. A propensity score that routes an account to immediate legal referral without confirming Section 129 compliance creates a regulatory breach. The referral logic must be built to check and document compliance at the point of routing.

NCA’s plain language requirement for consumer credit communications applies to all automated messages generated in response to a propensity score-driven treatment. Message templates used in digital outreach workflows must be reviewed against the plain language standard before deployment and version-controlled so that any content change goes through an approval process.

POPIA Constraints

Every data input used to train or score the propensity model must be sourced and processed with a documented lawful basis under POPIA. This applies to credit bureau data, internal payment history, contact response data, and any third-party data sources incorporated into the model. The purpose for which each input is used must be consistent with the purpose for which the data was originally collected and consented to.

The information officer must be able to produce data processing records for any input feature on request from a borrower or supervisory authority. An NBFC or credit provider that cannot produce this documentation for a deployed propensity model has a POPIA compliance gap that will surface during a regulatory review or a borrower data access request.

Propensity model outputs used to make automated collections decisions may engage POPIA’s provisions on automated decision-making depending on the nature of the decision and its impact on the borrower. Legal advice specific to the credit provider’s operating model should confirm the applicable obligations before deployment.

The Priority Order Is a Strategy. Propensity Scoring Makes It the Right One.

Every collections operation prioritises its portfolio in some order. Balance rank is a strategy. DPD rank is a strategy. System export order is a strategy. All of them are implicit. None of them uses the information that actually predicts which accounts will pay, respond, and self-cure in the current cycle.

Propensity scoring makes the prioritisation strategy explicit, measurable, and grounded in the signals that reflect how South African borrowers in this specific portfolio actually behave. Month-end salary cycles, multiple credit agreement exposure, language preference, and debt review pipeline signals are all available in the data. The question is whether the collections system is organised to use them.

Five markers of a well-designed propensity scoring programme for South African credit providers:

- Separate scores for pay, respond, and self-cure propensity, each driving a distinct routing decision

- Training data drawn from South African portfolio behaviour, including month-end salary patterns, multiple credit agreement exposure, and product-type norms specific to the credit provider’s portfolio

- Explicit score-to-treatment mapping documented in collections policy: each score band maps to a defined treatment, not a general priority tier

- Score distribution stability and feature drift monitored continuously, with a documented retraining trigger when drift exceeds a defined threshold

- Full NCA and POPIA compliance built into the model design: debt review suppression at the point of scoring, Section 129 alignment in legal referral routing, plain language compliance in message templates, and documented data processing records for all model inputs

iTuring’s AI collections platform deploys separate propensity scores for pay, respond, and self-cure behaviour, trained on South African portfolio data, with native NCA and POPIA compliance documentation built into the deployment framework.