TL;DR

- The 1-30 DPD window has the highest recovery probability for US community banks – flat strategies waste Regulation F contact frequency budget on accounts that will self-cure

- Regulation F’s 7-contact-in-7-days limit makes early bucket strategy a frequency budget problem – propensity allocation concentrates the budget on accounts that need intervention

- Self-cure identification removes 15-25% of the early bucket queue before first contact, directly reducing Regulation F frequency cap exposure and improving cost per recovery

- US community banks with AI early bucket sequencing achieve 38-52% reduction in early-stage charge-off rates versus alphabetical or DPD-date-ordered strategies

- iTuring identifies self-cure accounts before dialling begins, sequences the remaining queue by propensity, and enforces Regulation F frequency caps at system level

A $3.2B community bank’s collections team runs Monday’s 1-30 DPD queue: 2,100 accounts, alphabetically. 280 self-cure by 10 AM. 280 contacts that consumed Regulation F frequency budget without generating a recovery conversation. For any Head of Collections at a US community bank, the challenge of early bucket collections in the 1-30 DPD window is fundamentally an allocation problem: how to maximize recovery and prevent roll to 30-60 DPD while spending each of the seven permitted Regulation F contact attempts on accounts that actually need intervention. Without a strategy that distinguishes self-curers from at-risk accounts before dialling begins, community banks burn agent capacity, inflate cost per recovery, and expose themselves to unnecessary FDCPA frequency complaints. This article breaks down a propensity-based AI approach to the 1-30 DPD window, equipping collections leaders with a framework for self-cure identification, frequency budget allocation, and SR 11-7 compliant model governance. iTuring addresses this through closed-loop propensity scoring with autonomous agent outreach.

Why the 1-30 DPD Window Is a Regulation F Frequency Budget – and How Most Banks Spend It Wrong

For a Head of Collections at a US community bank, the 1-30 DPD window is the single highest-yield stage in the recovery lifecycle. Recovery probability exceeds 85% in the earliest delinquency stage and drops sharply with each subsequent bucket. The operational reality: your team has a finite number of Regulation F contact attempts per account per seven-day period, a queue of 1,500 to 3,000 accounts refreshing weekly, and no reliable signal for which accounts will pay on their own. A US bank early-stage collections AI strategy resolves this by scoring every account before the first dial, but most teams still work the queue by DPD date or alphabetical order, treating every account as equally likely to roll.

The problem persists because most community bank collections platforms lack a real-time propensity layer. Core banking systems export a flat file of delinquent accounts each morning. The collections team imports the file, applies a static sort, and begins dialling. There is no behavioral signal: no salary deposit timing, no prior payment pattern analysis, no self-cure probability score. The result is that agents spend 15-25% of their daily contact attempts reaching borrowers who would have paid within 48 hours without any outreach.

That wasted contact volume carries a measurable cost. Each unnecessary attempt consumes one of seven permitted Regulation F contacts, reducing the team’s capacity to reach genuinely at-risk accounts. US community banks deploying propensity-based 1-30 DPD sequencing reduce early-bucket charge-off rates by 38-52% and reduce per-contact FDCPA compliance overhead by 31% (iTuring US Community Bank Collections Deployment Data 2024-25). The table later in this article shows where US community banks teams currently stand on each dimension.

How DPD-Ordered Dialling Wastes Regulation F Contact Attempts on Accounts That Will Self-Cure

Standard rule-based diallers and static bucket workflows were designed to solve a different problem: ensuring that every delinquent account receives at least one contact attempt within a defined timeframe. They do this well. The dialler processes a flat list, enforces call-hour windows, and logs outcomes. But for a community bank managing early bucket collections in the 1-30 DPD window, the failure mode is not missed contacts: it is misallocated contacts. The dialler has no mechanism to distinguish a borrower whose paycheck deposits tomorrow from one who is genuinely unable to pay. It treats both identically, consuming the same Regulation F frequency budget on each.

The gap compounds at the cost-per-contact level. Community banks that view inaction on AI as the greatest risk are recognizing that each wasted early-bucket contact attempt has a downstream cost: one fewer attempt available for a borrower who needs a payment arrangement conversation, one more account rolling to 30-60 DPD where recovery cost triples. Without propensity data feeding back into the queue, the dialler cannot retrain or adjust. Every week looks the same. The gap is a design scope problem: a community bank’s challenge of maximizing recovery and preventing roll in the 1-30 DPD window within Regulation F’s frequency budget requires a tool built specifically for this layer.

How to Build an AI-Driven Early Bucket Strategy for a US Community Bank 1-30 DPD Portfolio

Step 1: Ingest daily delinquency feed and score every 1-30 DPD account for self-cure probability iTuring’s Collections Agent receives the bank’s daily delinquency export and scores each account against 25,000+ behavioral features, including salary deposit cadence, historical cure timing, and balance trajectory. The collections team sees a dashboard split: self-cure accounts (suppressed from dialling) and intervention-required accounts (ranked by propensity). This is the foundational step for early bucket collections at US community banks, applying AI to the 1-30 DPD window before a single call is placed.

Step 2: Remove self-cure accounts from the active contact queue Accounts scoring above the self-cure threshold are held in a monitoring state. iTuring tracks whether each suppressed account cures within the predicted window. If an account does not cure within 72 hours, it is automatically re-scored and re-queued. The collections team configures the self-cure threshold during onboarding, typically calibrated to a 90% confidence interval.

Step 3: Rank remaining accounts by payment propensity and assign contact channel The surviving queue is ordered by predicted payment probability. High-propensity accounts receive digital-first outreach: text with a payment link or email with a portal URL, where TCPA consent exists. Medium-propensity accounts are routed to voice agents. This US bank early-stage collections AI strategy ensures that each contact channel matches the account’s predicted response pattern, not a one-size-fits-all campaign rule.

Step 4: Schedule each contact at the account’s highest-response time window iTuring analyzes historical contact outcomes per account and identifies the time windows with the highest right-party contact rates. Calls and messages are scheduled to those windows rather than batch-dispatched at campaign start. The collections team receives a shift-level forecast showing expected contact volume by hour, enabling staffing alignment.

Step 5: Close the loop with outcome data and retrain weekly Every contact outcome, including payment, promise-to-pay, no answer, and wrong party, feeds back into the propensity model. iTuring retrains on the bank’s own payment data weekly, improving self-cure accuracy and contact-timing predictions with each cycle. SR 11-7 documentation is auto-generated with each retraining event, including data lineage, performance metrics, and model change records.

The point where US community banks teams most often expect friction: maximizing recovery and preventing roll in the 1-30 DPD window within Regulation F’s frequency budget, is precisely where this sequence prevents it.

How iTuring Allocates the 7-in-7 Frequency Budget to Maximum Recovery Yield

Self-cure probability model: scores every 1-30 DPD account for likelihood of payment within 48-72 hours without contact; removes self-curers from the active queue before the first attempt is made

Consider a community bank with 1,800 accounts entering the 1-30 DPD bucket on a Tuesday morning. iTuring’s self-cure model reads each account’s salary deposit history, prior delinquency cure patterns, current account balance relative to payment amount, and recent transaction velocity. Within minutes, 310 accounts score above the self-cure threshold. The collections team sees those 310 accounts flagged as “monitor only” in their queue, with a predicted cure date for each. If 280 of those accounts pay by Thursday, the model’s precision is validated and the team has avoided 280 unnecessary contact attempts, each of which would have consumed Regulation F frequency budget.

Unified Regulation F frequency counter: aggregates AI-initiated and human-agent contacts in one per-account counter; the 7-in-7 limit is enforced across all channels, not per channel separately

The mechanism is straightforward but operationally critical. Every contact attempt, whether initiated by iTuring’s autonomous agent via text, email, or voice, or by a human collector making a manual call, increments a single per-account counter. The counter tracks a rolling seven-day window per account. When an account reaches seven attempts, iTuring hard-blocks all outreach channels for that account until the window resets. There is no override path. For community banks managing early bucket collections in the 1-30 DPD window with AI, this eliminates the compliance risk of channel-siloed counting, where a text campaign and a voice campaign each track their own limits independently. AI-driven collections platforms that enforce compliance at the system level reduce FDCPA complaint rates by removing human discretion from frequency enforcement.

The highest-performing early bucket strategy for a community bank is not the one that contacts every account first: it is the one that identifies which accounts need contact and which will pay without it.

Propensity-ranked queue with per-account contact timing: remaining contacts ordered by payment likelihood, scheduled at each account’s historically highest-response time window, not at fixed campaign hours

The feedback loop operates on a weekly cadence. Each contact outcome updates the propensity model’s weighting of behavioral signals for that account segment. If Thursday-morning text messages to a particular borrower segment consistently produce higher payment rates than Tuesday-afternoon calls, the model shifts outreach timing accordingly. The governance benefit for community banks is that every timing adjustment is logged with full lineage: the signal that triggered the change, the prior and updated weights, and the expected performance impact. This audit trail satisfies SR 11-7 model change documentation requirements without manual effort from the collections or risk team.

Early Bucket Frequency Budget Allocation: AI Propensity Sequencing vs Standard Bank Dialler

Collections teams evaluating how to maximize recovery and prevent roll in the 1-30 DPD window within Regulation F’s frequency budget have real choices. Standard tools serve teams with straightforward contact-automation requirements: ensuring every account gets a call, logging outcomes, and enforcing call-hour rules. The comparison below is for teams whose scope extends to propensity-based allocation of early bucket contact attempts across the AI-driven 1-30 DPD window for US community banks. The table below compares the criteria that matter most for US community banks.

| Criterion | Standard Tools | iTuring |

| Account prioritisation | DPD date order | Propensity score rank – 25,000+ behavioral signals |

| SR 11-7 documentation | Manual – 3-8 weeks | Auto-generated – 30 minutes per exam |

| FDCPA/TCPA controls | Policy overlay, manual QA | Hard-coded – no override path |

| Self-cure identification | Not available | Removes 15-25% of queue from unnecessary contact |

| Explainability (ECOA) | Black-box score | SHAP waterfall per account – adverse action ready |

If your community bank’s early bucket portfolio is under 500 accounts per month, manual scoring with a model export may achieve comparable right-party contact improvement at lower platform cost.

38-52% Lower Early-Stage Charge-Off Rate: What Propensity-Sequenced Early Bucket Delivers

A US community bank with $4.8B in assets and a consumer lending portfolio generating 2,200 early-bucket accounts per month faced a specific problem: its collections team was spending 40% of Regulation F contact attempts on accounts that cured without intervention, leaving insufficient frequency budget for borrowers trending toward 30-60 DPD roll. The bank deployed iTuring’s Collections Agent with self-cure suppression and propensity-ranked queuing, completing integration with its core banking system in 11 days.

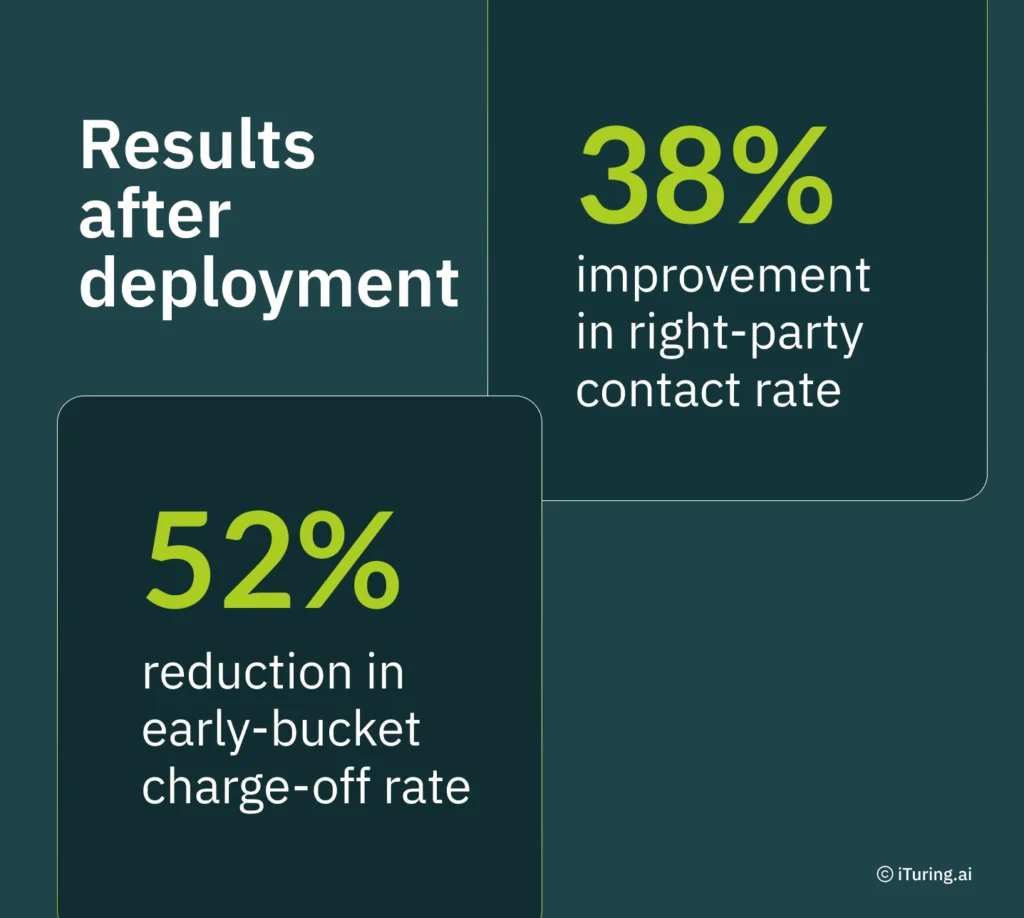

Results after deployment:

- 38% improvement in right-party contact rate

- 52% reduction in early-bucket charge-off rate

The 1-30 DPD Window Is a Frequency Budget Problem – Propensity Sequencing Is How You Spend It Right

Your seven permitted contacts per account per week are not a compliance checkbox: they are a finite resource that determines how many at-risk borrowers your team can actually reach. Self-cure identification is not a nice-to-have feature; it is the mechanism that frees frequency budget for accounts where a conversation changes the outcome. Every community bank collections leader running a flat queue is making an implicit decision to treat all delinquent accounts as equally likely to roll, and that decision has a measurable cost in charge-offs and agent hours.

For the US bank early bucket collections playbook: Regulation F frequency compliance, self-cure benchmarks, and SR 11-7 documentation.

iTuring identifies self-cure accounts before your first dial and enforces Regulation F frequency caps at system level: test it against your bank’s 1-30 DPD queue before any licence decision.