TL;DR

- FDCPA applies fully to every AI-generated collections touchpoint

- Regulation F’s 7-in-7 rule must be enforced at the model level

- CFPB requires specific, accurate reasons for every adverse decision

- Audit trails and consent logs are now a baseline expectation

- Compliance embedded in the model beats bolt-on compliance tools

Picture a self-driving car with a perfect GPS system. It knows the fastest route, avoids traffic, and never misses a turn. But it has no knowledge of traffic laws. It runs red lights, exceeds speed limits, and the passengers have no idea anything is wrong. When the violations stack up, the car manufacturer walks away clean. The person who deployed it does not.

That is the situation many collections teams are walking into with AI in 2026. The model optimizes. The dials go out. The recovery numbers look good. And somewhere in the background, FDCPA violations are accumulating at $500 to $1,500 per contact. The AI does not know it broke the law. The institution still pays the fine.

This blog is a practical guide for collections leaders, compliance officers, and technology teams who want to understand exactly where FDCPA obligations land when AI is doing the outreach, and what a genuinely compliant AI collections setup looks like.

What the FDCPA Actually Governs

The Fair Debt Collection Practices Act has been federal law since 1977. Regulation F, implemented by the CFPB in November 2021, updated it for modern communication channels. Together they govern the following areas that directly affect AI collections systems:

- Who can be contacted: Only the consumer, their attorney, or authorized third parties

- When contact is allowed: Not before 8 a.m. or after 9 p.m. in the consumer’s local time zone

- How often contact can occur: No more than 7 call attempts within any 7 consecutive days per debt (the 7-in-7 rule)

- What constitutes harassment: Repeated calls designed to annoy, repeated use of obscene language, or false representations

- Consumer rights: The right to dispute a debt, request debt validation, and opt out of further contact

The CFPB has been explicit: AI does not create an exemption. Institutions remain fully responsible for the outcomes their AI systems produce, regardless of how automated the process is.

Where AI Collections Models Break FDCPA Rules

Most FDCPA violations from AI systems are not intentional. They are architectural. The model was built to maximize contact and recovery. Nobody wired the compliance rules into it.

Here are the four most common failure modes:

- Over-contacting consumers: An AI dialer that tracks call volume at the campaign level, rather than per debt per consumer, can easily exceed the 7-in-7 limit without flagging a single alert. If a consumer holds three separate debts, each allows 7 attempts, but a poorly configured system can treat them as one pool and blast far beyond the safe harbor threshold.

- Wrong-party contact: AI systems that pull contact data from stale or unverified sources and dial without identity confirmation at the point of contact expose the institution to wrong-party violations. Once the wrong person has been contacted about someone else’s debt, the harm under FDCPA is already done.

- Opaque scoring decisions: When an AI model flags an account for escalated collections activity, and the consumer disputes it, the institution must be able to explain why that decision was made. A black-box score is not an explanation.

- Bias embedded in historical data: Models trained on past collections outcomes can learn and reinforce patterns that disproportionately target certain demographic groups. This creates fair lending exposure that sits directly alongside FDCPA obligations.

The Explainability Obligation the CFPB Made Official

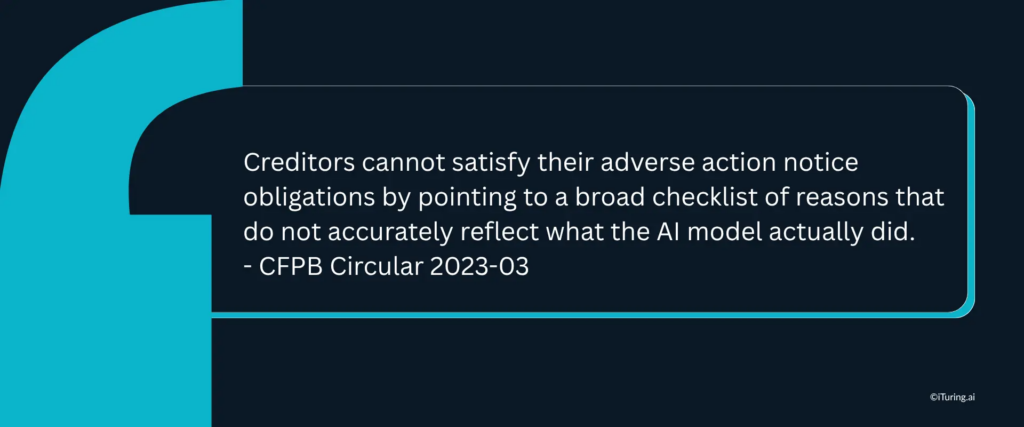

In September 2023, the CFPB issued Circular 2023-03 addressing a specific question: when a lender uses an AI model to make a credit or collections decision, can they satisfy their adverse action notice obligation by using a generic checklist of reasons?

The answer was no.

The CFPB confirmed that creditors must provide specific, accurate reasons that actually reflect why the AI made the decision it made. Generic bucket reasons like “unsatisfactory credit history” are not sufficient if the model was actually driven by payment timing patterns, bureau tradeline velocity, or behavioral signals. The circular built on earlier 2022 guidance and was reinforced again in Skadden’s analysis of CFPB enforcement expectations.

For collections teams, this has a direct operational implication. Every AI model that scores accounts, segments portfolios, or triggers escalated outreach must be able to produce a human-readable explanation of what drove that outcome. Techniques like SHAP (SHapley Additive exPlanations) and LIME (Local Interpretable Model-agnostic Explanations) make this possible at the individual prediction level, not just at the aggregate model level.

Bolt-On Compliance vs. Embedded Compliance

There are two ways to approach FDCPA compliance in an AI collections environment. One is significantly more dangerous than the other.

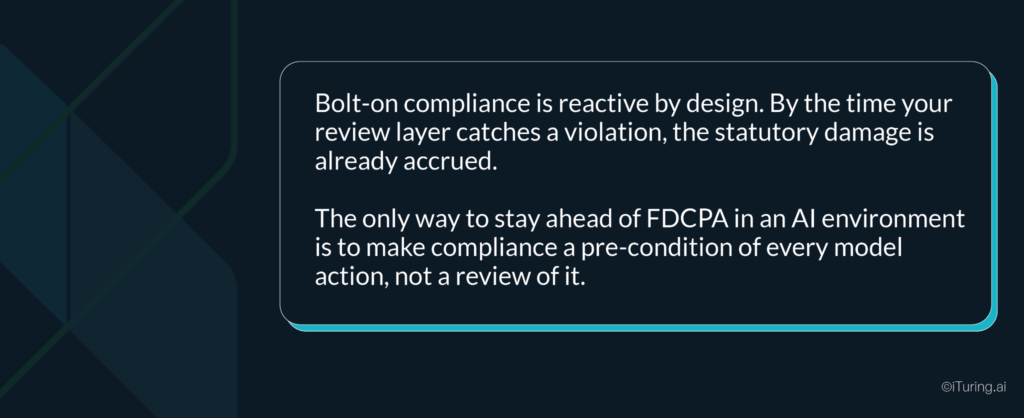

Bolt-on compliance means the AI model runs freely, and a separate compliance layer checks the outputs after the fact. Human reviewers audit call logs. Violation alerts fire after the contact has already been made. This approach is reactive by design, and by the time a violation is caught, the statutory damage is already accrued.

Embedded compliance means the regulatory rules are constraints built into the model itself, enforced before any outreach action is taken. The 7-in-7 counter is checked in real time before every dial attempt. Opt-out signals are registered and respected at the channel level immediately. Contact time windows are enforced by the platform, not by an agent manually checking a clock.

The practical difference between these two approaches:

- Per-debt contact counters that track every attempt, answered or not, in a rolling 7-day window before the next dial is initiated

- Real-time consent tracking that blocks any outreach to a consumer who has opted out, across every channel simultaneously

- Immutable audit logs with timestamps for every automated action, every decision, and every communication attempt

- Maker-checker approval workflows that require human sign-off before a new AI model or updated scoring logic goes into production

- Continuous bias monitoring that runs post-deployment to catch distributional shifts before they become regulatory findings

What Audit-Ready AI Collections Looks Like in Practice

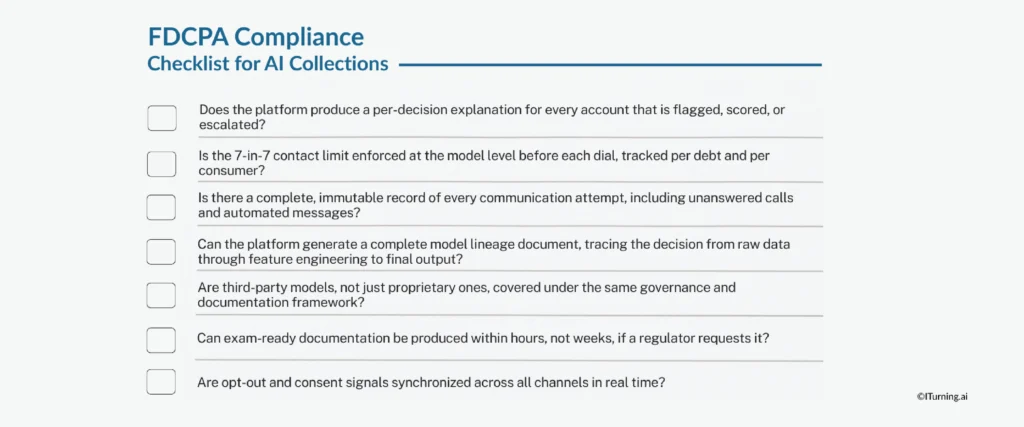

Regulators and examiners are not asking for reassurances that an institution takes compliance seriously. They are asking for documentation that proves it. Here is the practical checklist for collections teams evaluating whether their AI infrastructure can withstand scrutiny:

- Does the platform produce a per-decision explanation for every account that is flagged, scored, or escalated?

- Is the 7-in-7 contact limit enforced at the model level before each dial, tracked per debt and per consumer?

- Is there a complete, immutable record of every communication attempt, including unanswered calls and automated messages?

- Can the platform generate a complete model lineage document, tracing the decision from raw data through feature engineering to final output?

- Are third-party models, not just proprietary ones, covered under the same governance and documentation framework?

- Can exam-ready documentation be produced within hours, not weeks, if a regulator requests it?

- Are opt-out and consent signals synchronized across all channels in real time?

If any of these answers is no or unclear, the institution is carrying FDCPA exposure it may not have quantified yet.

Why This Matters More in 2026 Than It Did in 2021

Regulation F came into effect in November 2021. In its first two years, enforcement focused primarily on obvious manual violations. But as AI adoption in collections has accelerated, regulatory attention has shifted toward the systems producing the outreach, not just the outreach itself.

The CFPB has made its supervisory priorities clear: AI governance, explainability, and bias are all active areas of examination focus. Institutions that cannot demonstrate documented, governed, explainable AI processes are increasingly at risk, not just of individual violation penalties, but of supervisory action that constrains operational capacity.

The $500 to $1,500 per-violation penalty that the TCPA and FDCPA carry does not scale gracefully when AI systems are making thousands of contact decisions per day. A single misconfigured contact counter, running for 30 days before it is caught, can produce a liability exposure that no recovery performance number offsets.

How iTuring Approaches This Problem

iTuring was built for regulated industries, which means compliance is not a feature added to the platform. It is a structural property of how the platform works.

Every AI collections model deployed through iTuring carries:

- SHAP and LIME explainability built in at the prediction level, not just the aggregate model

- Immutable audit trails with timestamps for every model action and communication trigger

- Maker-checker approval workflows that require documented human sign-off before any model goes live

- Continuous monitoring across 60 parameters, including drift and bias, with alerts generated before a problem reaches the regulator

- One-click exam documentation that compiles full model lineage, approval history, and explainability evidence into a reviewable package

For collections teams, this means the governance layer is not a separate project that runs alongside the AI project. It runs inside it.

If your institution is building or scaling AI collections capability and wants to understand what a fully governed, FDCPA-compliant deployment looks like in practice,