TL;DR

- MLOps is the operational discipline of running AI models in production

- SA credit providers need governance frameworks before going live

- Model monitoring must be continuous, not limited to annual review cycles

- SARB and NCA compliance requirements shape every stage of implementation

- Vendor-supplied models still require full in-house governance ownership

Building an AI collections model and running one are two different disciplines. A model that performs well in development can fail in production for reasons that have nothing to do with the quality of the underlying algorithm. The training data becomes stale as the portfolio evolves. The portfolio composition shifts toward product types the model was not trained on. A regulatory change alters which contact types are permissible at a given DPD stage. The vendor updates the model parameters on a release cycle without the credit provider’s full visibility. A feature that was highly predictive during training stops being available because the data feed it depended on changed.

None of these failures are algorithmic. All of them are operational. And all of them are preventable with the right governance infrastructure in place before the model goes live.

MLOps, machine learning operations, is the discipline that governs how AI models move from development into production, how they are monitored once live, how changes are managed and documented, and how the governance trail is maintained for regulatory examination. For South African credit providers operating under SARB model risk guidance and NCA consumer protection requirements, MLOps is the operational infrastructure that makes AI collections compliance achievable in practice. Without it, a credit provider may be running models in production that lack current inventory entries, continuous monitoring records, or change documentation, all of which are governance gaps under SARB’s framework.

This blog covers what MLOps means for SA credit providers, the five stages of AI collections implementation, what production monitoring requires, what SARB demands in practice, and what a well-governed programme looks like.

What MLOps Means for SA Credit Providers

MLOps is the set of practices, processes, and infrastructure that govern how machine learning models are deployed, monitored, updated, and retired in a production environment. It is not a technology product. It is a set of practices that technology tools support. The practices themselves must be owned and operated by the credit provider, not delegated to a vendor platform.

Three reasons MLOps is specifically relevant for South African credit providers shape the implementation approach.

Regulatory accountability under SARB. SARB’s model risk management guidance requires that every production model has a documented owner, a pre-deployment validation record, a continuous monitoring programme, and a governance trail for every material change. These requirements do not resolve themselves through good model development. They require operational processes: model inventory maintenance, monitoring log generation, change documentation workflow, and governance committee oversight. MLOps is the framework that makes these processes systematic rather than ad hoc.

Portfolio volatility. South African consumer credit portfolios are sensitive to macroeconomic conditions, rand exchange rate movements, fuel price changes, and administered price increases in ways that can shift payment behaviour faster than annual model review cycles can detect. A collections model deployed during a period of relative economic stability can degrade meaningfully within two quarters if conditions shift. MLOps monitoring detects this degradation through continuous metric tracking rather than waiting for recovery rate deterioration to surface in management reporting.

Vendor model risk. Many South African credit providers use vendor-supplied AI collections models. MLOps governance clarifies where vendor responsibility ends and credit provider responsibility begins. SARB holds the credit provider accountable for all production models regardless of their origin. A vendor that provides a model, monitoring infrastructure, and documentation support is contributing to the credit provider’s MLOps programme. The governance obligation itself, validation ownership, monitoring record retention, change sign-off, cannot be contracted away.

MLOps is not a technology product. It is the set of practices that govern how AI models run in production. Technology tools support those practices. The practices must be owned by the credit provider.

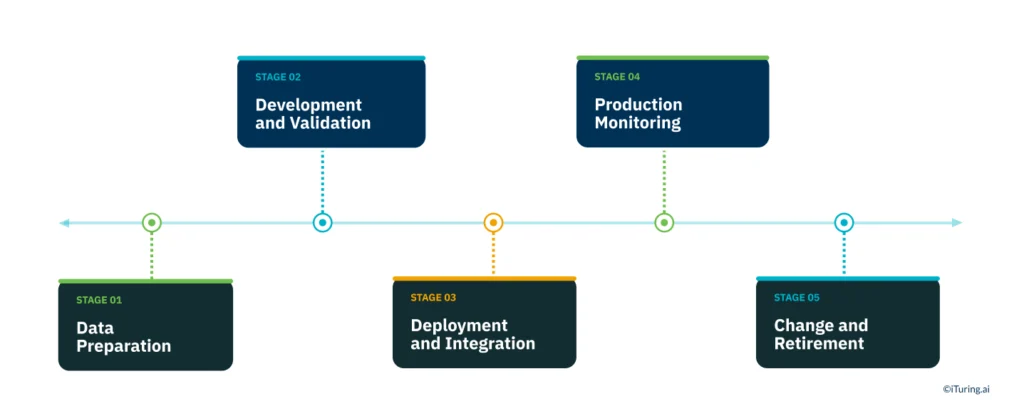

The Five Stages of AI Collections Implementation

AI collections implementation for a South African credit provider follows five stages, each with specific governance actions required before the next stage begins.

Stage 1: Data Preparation and Governance

The foundation of a reliable collections model is data that reflects the actual population being scored. Before any model training begins, all data sources must be identified and documented: internal payment history, contact response history, credit bureau data, account origination data, and any third-party enrichment sources.

The POPIA lawful basis for each data source must be confirmed and recorded before training begins. This is not a post-deployment review. A model trained on data without confirmed processing records has a POPIA compliance gap from the first training run. The purpose for which each data source is used must be consistent with the purpose for which it was originally collected.

Data quality standards must be established: missing value thresholds that determine when an account is excluded from scoring, outlier handling rules, recency requirements for training data. For South African portfolios, training data should reflect post-pandemic payment behaviour, month-end salary credit patterns, and multiple credit agreement exposure across providers. Training on pre-2020 data without recency weighting will produce a model calibrated to a credit environment that no longer exists.

Stage 2: Model Development and Pre-Deployment Validation

Model development should use the credit provider’s own portfolio data as the primary training dataset, not solely vendor benchmark datasets representing a different population. Backtesting on a holdout sample drawn from the credit provider’s own accounts confirms that the model’s rank ordering holds on the specific population being scored, not on a generic benchmark.

Pre-deployment validation covers four areas. Rank-order accuracy testing using Gini coefficient and Kolmogorov-Smirnov statistic confirms the model separates paying from non-paying accounts with acceptable discrimination. Score distribution review confirms the proportion of accounts in each score band reflects the expected portfolio distribution. Feature importance documentation confirms which signals are driving scores and whether those signals are operationally stable. Differential outcome testing confirms the model does not produce systematically different treatment recommendations for borrower groups based on characteristics correlated with NCA-protected categories.

For vendor-supplied models, the credit provider must conduct this validation on its own portfolio data. Vendor benchmark validation results do not discharge the credit provider’s validation obligation under SARB’s framework.

Stage 3: Deployment and Integration

Deployment requires three technical integrations before any live account scoring begins.

The triggering event architecture must be defined: what account events fire a decisioning call to the model. Payment posting, PTP window closure, contact response or non-response, and calendar-based triggers must each be wired to the scoring engine with latency measured in seconds for a real-time implementation.

NCA compliance checks must be integrated into the decisioning flow before go-live. Debt review status check under Section 86, Section 129 process status for accounts approaching legal referral, and contact hour restriction enforcement must all run as gates within the decisioning sequence. These checks must be tested end-to-end in the integration environment before any live accounts are processed.

A parallel run is strongly recommended before full cutover: running the new model alongside the existing collections process for a defined period, comparing outputs without applying new treatment assignments to the full portfolio. The parallel run identifies cases where the new model produces treatment recommendations that differ materially from the current process, and gives the governance team an opportunity to review those differences before they affect live accounts.

Stage 4: Production Monitoring

Monitoring begins on day one of live operation and runs continuously. Three monitoring checks form the core programme.

Gini coefficient monitoring tracks whether the model continues to rank-order accounts by payment probability accurately. Score distribution monitoring tracks whether the proportion of accounts in each score band is stable. Feature drift monitoring using Population Stability Index tracks whether the input feature distributions are shifting relative to training.

Monitoring results must be logged at each monitoring interval, not reviewed informally and discarded. The log is the time-series record that SARB examination requires. An examiner asking for evidence of ongoing model monitoring should be able to receive a complete log of Gini, PSI, and score distribution metrics from deployment date to examination date, with documented threshold breaches and the responses they triggered.

Retraining triggers must be documented before go-live. A Gini decline of more than a defined number of percentage points from the deployment baseline triggers a formal review. PSI above 0.2 on a key feature triggers a model review. These thresholds must be set in writing before the model goes live, not determined retrospectively when performance issues surface.

Stage 5: Model Change and Retirement

Every material change to a production model requires model change governance documentation: a description of the change, the rationale, independent review from the model validation function, and sign-off from the model risk committee or equivalent governance body before the change is deployed. This applies to retraining cycles, feature set additions or removals, score band reconfigurations, and treatment matrix updates that constitute collections policy changes.

When a model is retired and replaced, the replacement model must complete full pre-deployment validation before the legacy model is decommissioned. Documentation for the retired model must be retained for the period specified in the credit provider’s data retention policy and any applicable regulatory requirements. The model inventory entry for the retired model should record the decommission date and the validation status of its replacement at the time of handover.

Production Monitoring in Practice

Three monitoring checks constitute the core of a production MLOps programme for SA credit providers. Each check targets a different failure mode and requires a different response when its threshold is breached.

Gini Coefficient Monitoring

The Gini coefficient measures the model’s ability to rank-order accounts by payment probability across the full score distribution. A declining Gini coefficient indicates concept drift: the relationship between the model’s input features and actual payment outcomes has changed since the training period. For South African collections models, concept drift is most commonly triggered by macroeconomic shifts, post-pandemic borrower behaviour changes, or portfolio composition changes that alter the feature-outcome relationships the model was trained on.

Gini monitoring should run monthly at minimum for material collections models. A decline of more than five percentage points from the deployment baseline is a common threshold for triggering a formal model review. The specific threshold should be documented before deployment and reflect the credit provider’s tolerance for scoring inaccuracy in the collections context.

Gini monitoring results must be logged at each monitoring interval and retained in a format that supports a continuous time-series view. A SARB examination will expect to see this record, not a summary of recent results.

Score Distribution Monitoring

Score distribution monitoring tracks whether the proportion of accounts falling into each score band is shifting over time. A material shift in score distribution, without a corresponding and explained shift in portfolio composition, indicates that the input feature distributions have changed relative to training. The model is applying weights calibrated on one distribution to a different population.

For South African portfolios sensitive to economic conditions, score distribution shifts often appear before Gini declines because they reflect input feature changes before those changes fully translate into outcome rank-order deterioration. Score distribution monitoring serves as an early warning indicator that allows the credit provider to initiate a model review before performance deterioration is visible in recovery rate reporting.

Feature Drift Monitoring Using PSI

Population Stability Index measures the distributional shift of individual input features between the training period and the current monitoring period. PSI below 0.1 indicates a stable distribution. PSI between 0.1 and 0.2 indicates moderate shift that warrants increased monitoring frequency. PSI above 0.2 on a key feature indicates the model’s weight for that input was calibrated on a distribution that no longer reflects the live portfolio, and a formal model review should begin.

For SA credit providers, the features most likely to show meaningful PSI drift include month-end payment timing patterns, contact response rates by channel, multiple credit agreement counts, and geographic income signals. These features are sensitive to the specific macroeconomic and portfolio dynamics of the South African market. Monitoring them at monthly intervals on the top five to ten features by model importance weighting provides early detection of the portfolio shifts most likely to affect collections model accuracy.

Gini monitoring, score distribution tracking, and PSI on key features form the three-check monitoring framework that keeps a production AI collections model within its validated performance range.

SARB Governance Requirements in Practice

Five SARB model risk management requirements directly shape how SA credit providers structure their MLOps programmes.

Model Inventory Currency

Every production model must be registered in a model inventory with documented purpose, owner, data inputs, training date, validation status, last review date, and monitoring frequency. The inventory must reflect the model’s current state. An entry that records the model as it existed at original deployment, without updates for subsequent retraining cycles or material parameter changes, does not meet SARB’s documentation standard. The model inventory is a live record. It requires a process for updating it after every material change, not just at the annual model review.

Pre-Deployment Validation by the Credit Provider

Independent validation by the credit provider’s model validation function is required before any model goes into production. For vendor-supplied models, the credit provider must conduct its own validation on its own portfolio data. Vendor benchmark results and vendor-issued validation reports are supporting evidence. They do not substitute for the credit provider’s own validation documentation. The pre-deployment validation record must be retained and available for SARB examination.

Continuous Monitoring Records

Monitoring results must be recorded continuously and available for SARB examination. Informal monitoring that cannot be evidenced with a time-series record does not satisfy this requirement. The monitoring log must exist as a retrievable document, not as a series of informal discussions or dashboard screenshots that are not retained.

Model Change Governance Documentation

Every material change to a production model requires documentation of the change, the rationale, independent review, and model risk committee sign-off before deployment. This includes retraining cycles where the model structure is unchanged but the training data window has moved. It includes treatment matrix updates that constitute changes to the collections policy the model executes. It includes score band reconfigurations and feature set changes. The documentation must be retained and available for examination including for changes that were reviewed and approved without any modification to the original proposal.

Vendor Accountability Allocation

SARB holds the credit provider accountable for all production models regardless of origin. Vendor contracts should specify what documentation the vendor provides, what infrastructure support they offer, and what the credit provider remains responsible for independently. The credit provider’s internal governance records should reflect this allocation clearly. An examiner asking who is responsible for the model’s ongoing validation, monitoring, and change governance should find a clear answer in the credit provider’s documentation, not a reference to the vendor’s platform terms.

A Model That Cannot Be Examined Is a Model That Cannot Be Trusted

The regulatory examination question for a South African credit provider running AI collections is not whether the model performs well. It is whether the credit provider can demonstrate, with documentation, that the model was validated before deployment, has been monitored continuously since, and has had every material change reviewed and approved through a documented governance process.

A model that performs well but cannot produce that documentation trail is a governance risk. A model that performs adequately but has a complete, current, and accessible governance record is a credit provider that can defend its AI collections programme in a SARB examination, an NCA consumer complaint investigation, or an NCR audit.

MLOps is what creates that trail. Not as a retrospective compliance exercise, but as the operational discipline through which the credit provider runs its AI collections programme from day one.

Five markers of a well-run MLOps programme for South African credit providers:

- Model inventory is current, with each production model’s entry updated after every material change including retraining cycles

- Monitoring runs continuously with automated alerting when Gini, PSI, or score distribution thresholds are breached, and all results are logged in a retrievable time-series format

- All model change governance documentation is retained in a format available for SARB examination, including changes where the decision was to maintain the current model without update

- NCA compliance checks, including debt review suppression and Section 129 alignment, are integrated into the production decisioning flow and tested end-to-end at each deployment cycle

- Vendor responsibility is clearly documented in the contract and the credit provider’s internal governance records explicitly identify what the credit provider owns independently of the vendor

iTuring’s AI collections platform is built with MLOps governance infrastructure for South African credit providers: continuous Gini, PSI, and score distribution monitoring with automated alerting, native model change governance documentation, NCA compliance integration tested at each deployment, and model inventory management with update tracking.