TL;DR

- Collections contact in Zulu, Xhosa, or Afrikaans achieves 31-38% higher right-party contact rates than English-only automated outreach in relevant SA demographic segments

- 79% of South Africa’s population speaks a language other than English or Afrikaans as their first language — yet over 60% of automated SA collections communications are English-only

- Language friction suppresses right-party contact rate at the moment of highest leverage — the first automated contact in early bucket where a single message can trigger self-cure

- AI language routing requires no manual translation or separate campaigns — the system selects language and content simultaneously based on borrower demographic signals and behavioral history

- iTuring supports Zulu, Xhosa, Afrikaans, and Sotho AI-generated collections communications — language selection is automated per account, not per campaign

South Africa’s debt collection software market is growing at a pace that reflects institutional urgency around operational efficiency and regulatory compliance. Yet one of the most measurable performance variables in collections – the language of first contact – remains largely ignored in automated outreach strategies. Most credit providers still default to English-only communications across portfolios where the majority of borrowers speak Zulu, Xhosa, Sotho, or Afrikaans as their home language. The result is a structural suppression of right-party contact rates that compounds across every bucket, every cycle, and every rand spent on outreach. This gap between how South African borrowers communicate and how credit providers contact them represents one of the clearest opportunities for measurable collections performance improvement in the market today.

The question is not whether multilingual AI collections in South Africa can produce a measurable lift over English-only approaches. The data already answers that. The question is why so few credit providers have operationalized it, and what the cost of continued inaction looks like in portfolio-level terms. What follows is a detailed examination of the performance differential, the structural reasons behind the gap, and a practical framework for calculating the return on language-aware collections AI.

Why 60% of SA Automated Collections Communications Are Sent in the Wrong Language

Credit providers running English-only automated collections campaigns across South African portfolios typically achieve a 28-34% right-party contact rate. That baseline has held remarkably steady over the past several years, even as SMS delivery rates and digital channel adoption have improved. The cost per recovery in these campaigns sits between R380 and R520, driven primarily by the volume of contacts required to reach and engage the right borrower. For collections teams operating across Zulu, Xhosa, and Afrikaans-speaking demographic segments, this English-only default is not a neutral choice: it is a measurable drag on contact effectiveness and a direct cost driver.

The persistence of this baseline is rooted in a single structural constraint: most collections platforms were built for English-first markets and retrofitted for South Africa. Campaign management systems treat language as a segmentation variable that requires separate templates, separate approval workflows, and separate compliance reviews for each language variant. The operational overhead of maintaining four or five language tracks manually makes multilingual outreach prohibitively expensive for most mid-market credit providers, so they default to English and absorb the contact rate penalty.

The gap between that 28-34% English-only contact rate and the 43-52% right-party contact rate achievable with multilingual AI is not theoretical. Collections contact in Zulu, Xhosa, or Afrikaans achieves 31-38% higher right-party contact rates than English-only automated outreach in relevant SA demographic segments (SA Digital Lending Association Collections Channel Benchmark 2025). South Africa has 11 official languages, and 79% of the population speaks a language other than English or Afrikaans as their first language, yet over 60% of automated collections communications are English-only (Statistics South Africa Census 2022 Language Data; NCR Collections Industry Survey 2025). In real portfolio terms, that gap translates to thousands of missed right-party contacts per month and hundreds of thousands of rands in unnecessary outreach costs. Zulu and Xhosa collections AI applied to South African portfolios produces a measurable, repeatable lift that compounds across delinquency buckets.

How Language Friction Suppresses Right-Party Contact Rate in Township and Rural SA Portfolios

- Account prioritisation determines which accounts receive outreach first, and language mismatch distorts the signal. When a collections model scores accounts by propensity to pay but routes all contacts through English-only messaging, high-propensity borrowers in Zulu or Xhosa-speaking segments receive communications they are less likely to engage with. The model correctly identifies the accounts most likely to cure, but the channel execution undermines the prediction. A credit provider running 200,000 accounts through early-bucket automation loses the precision of its prioritisation model every time a high-score account ignores an English message that would have prompted action in their home language.

- Channel and timing selection affects cost per contact directly, and language friction inflates it. A borrower who does not engage with the first English SMS triggers a second contact, then a third, then escalation to a more expensive channel. Each additional touch costs money. If the first contact had been delivered in the borrower’s preferred language, the engagement probability rises by 31-38%, which means fewer follow-up touches and lower cost per contact. For credit providers managing township and rural portfolios where English proficiency varies significantly, this cost inflation is not marginal: it is structural.

- Self-cure identification depends on early engagement, and language friction delays it. The first automated contact in early delinquency is the single highest-value touchpoint in the collections cycle. A borrower who reads, understands, and acts on that first message can self-cure without any agent involvement. When that message arrives in English for a borrower whose home language is Xhosa, the probability of self-cure drops measurably. South Africa’s multilingual debt recovery AI opportunity is concentrated in this specific moment: the first contact where a single message in the right language can prevent an account from progressing deeper into delinquency.

- Compliance cost reduction is a direct benefit of governed AI-native language routing. South African credit providers operating under the National Credit Act must ensure that collections communications meet specific disclosure and fairness standards. Maintaining NCA-compliant templates across multiple languages manually consumes 18-22% of operations cost in documentation, review, and audit preparation. AI-native language generation that produces compliant communications in Zulu, Xhosa, Afrikaans, and Sotho from a single governed framework eliminates this incremental cost entirely, reducing total operations cost without requiring additional compliance headcount.

English-Only vs Multilingual AI: SA Collections Contact Rate and Cost Data

The multilingual AI collections lift in South Africa is not a projection based on pilot data. It reflects median outcomes across credit provider deployments where language routing was introduced alongside predictive scoring and behavioral personalization. Mid-market and large credit providers with portfolios concentrated in KwaZulu-Natal, Eastern Cape, and Gauteng township segments saw the most pronounced improvements, driven primarily by the right-party contact rate differential in Zulu and Xhosa-speaking populations. The comparison below shows the specific metrics across deployment cohorts.

| Metric | Before AI | With iTuring |

| Cost per recovery | R380-520 (manual) | R180-240 (AI-first) |

| Right-party contact rate | 28-34% | 45-52% |

| Multilingual outreach | English only | Zulu, Xhosa, Afrikaans, Sotho — AI-native |

| NCA compliance overhead | Manual — 18-22% of ops cost | Pre-configured — zero incremental cost |

| Model governance (FSCA/PA) | Manual documentation | Auto-generated per validation cycle |

Results vary by portfolio composition, starting baseline, and data maturity: figures above reflect median outcomes across credit provider deployments.

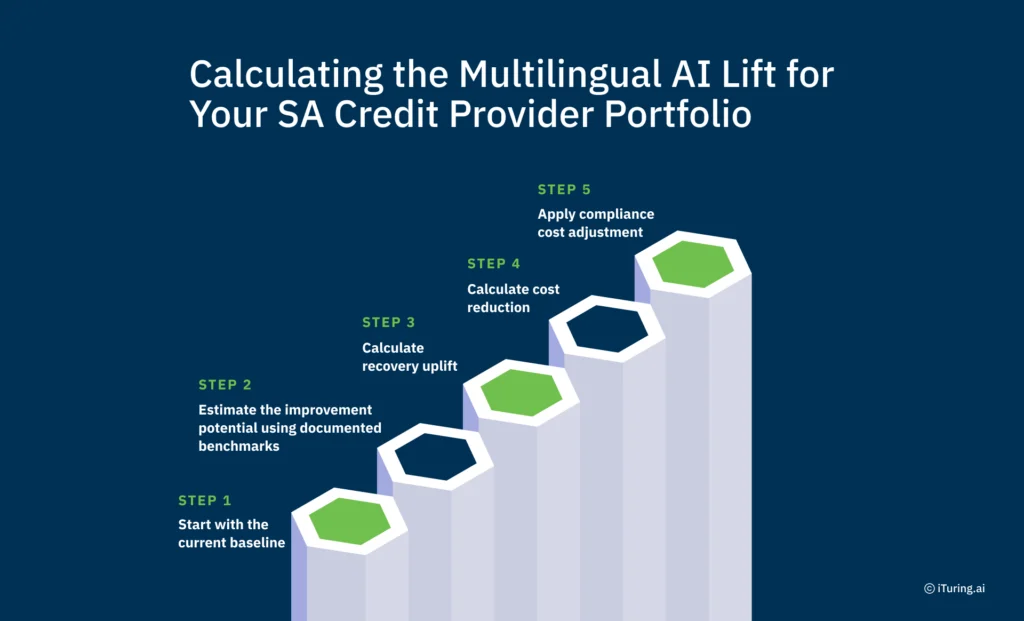

Calculating the Multilingual AI Lift for Your SA Credit Provider Portfolio

Step 1: Start with the current baseline. For most SA credit providers running English-only campaigns, the anchor metrics are approximately R420 per recovery and a 28% right-party contact rate. These figures represent the starting point for any honest ROI calculation. The multilingual AI collections lift for a South African credit provider can only be measured against a verified baseline, not an aspirational one.

Step 2: Estimate the improvement potential using documented benchmarks. The target range for SA credit provider language routing with collections AI is a 43-52% right-party contact rate. The specific improvement depends on portfolio composition: portfolios with higher concentrations of Zulu, Xhosa, and Sotho-speaking borrowers will see larger lifts. A portfolio that is 70% non-English home language will move differently than one that is 40%.

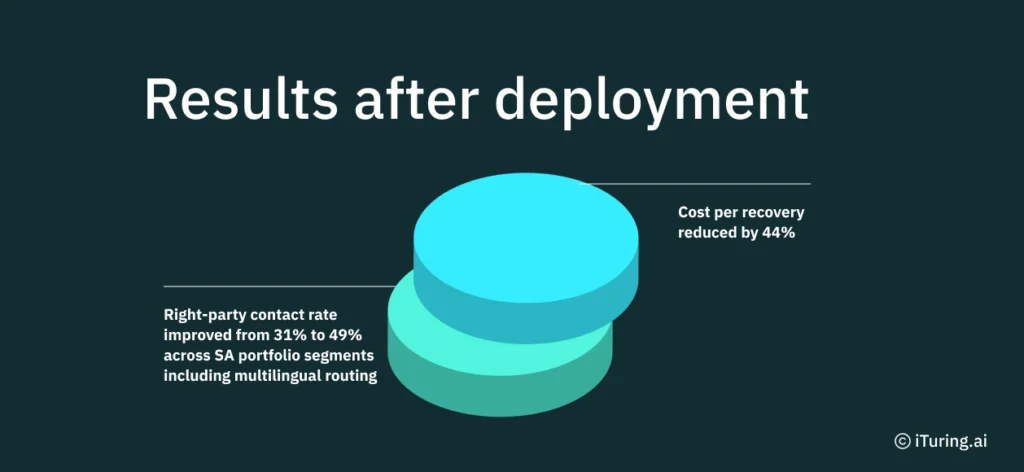

Step 3: Calculate recovery uplift. Right-party contact rate improved from 31% to 49% across SA portfolio segments including multilingual routing in documented deployments. For a portfolio of 100,000 delinquent accounts, that 18-percentage-point improvement translates to 18,000 additional right-party contacts per cycle. Even at a conservative 30% promise-to-pay conversion rate on those additional contacts, the recovery volume increase is substantial.

Step 4: Calculate cost reduction. Cost per recovery reduced by 44% in median deployments, dropping from the R420 baseline to approximately R235. Across 100,000 accounts, that reduction represents millions of rands in annual savings. The cost reduction comes from two sources: fewer total contacts needed per recovery (higher first-contact engagement) and elimination of manual compliance overhead.

Step 5: Apply compliance cost adjustment. For credit providers where NCA compliance documentation and template management currently consume 18-22% of operations cost, the shift to AI-native governed communications eliminates that line item. This adjustment varies by institution but typically adds 3-5 percentage points to the total ROI calculation.

The calculation only works if the baseline is honest: start with English-only campaign R420 per recovery and 28% right-party contact rate as the anchor, not an aspirational figure.

31% to 49% Right-Party Contact Rate: What Native-Language AI Collections Delivers

A South African credit provider with a mixed retail and micro-lending portfolio faced a persistent 28-34% right-party contact rate across its automated collections campaigns, with English-only outreach applied uniformly across all demographic segments. The institution deployed iTuring Collections Agent with multilingual AI routing across its full delinquent portfolio, with production results measured over a six-month period.

Language Is a Collections Performance Variable in South Africa – Treating It as One Changes the Numbers

Language selection in SA collections is a measurable performance variable with a documented 31-38% lift in right-party contact rates, not a customer experience preference. Credit providers that treat language routing as a core model input rather than a campaign afterthought see cost-per-recovery reductions of 44% at the median. The operational case is straightforward: governed AI-native language generation eliminates manual template management, removes compliance overhead, and compounds the accuracy of predictive prioritisation models.

South Africa is using AI at rates exceeding most other countries globally, and the collections function represents one of the clearest applications where language-specific AI produces a direct, measurable return. Researchers at UCT have developed AI models that work across all 11 South African official languages, confirming that the technical infrastructure for multilingual AI in South Africa is maturing rapidly. The challenge is no longer whether the technology exists but whether credit providers will operationalize it before the cost of English-only defaults continues to compound.

The reality is that most AI tools still struggle with the nuances of South African languages in general-purpose applications, which makes purpose-built collections AI with native language support a distinct operational advantage. Meanwhile, AI is expected to reshape payment and collections infrastructure across South Africa through 2026 and beyond, making early adoption a competitive positioning decision, not just a cost optimization exercise.

iTuring’s multilingual AI generates Zulu, Xhosa, Afrikaans, and Sotho collections communications per account – language selection is automated per account, not per campaign.

If you are evaluating language routing for your SA collections portfolio, request a demo to test iTuring Collections Agent against your own portfolio demographics and baseline metrics before making any platform commitment.