TL;DR

- US bank collections right-party contact rates average 26-28% with manual dialler operations — AI propensity timing improves this to 43-47% at identical call volume

- A 20 percentage point right-party contact improvement at equal call volume reduces cost per recovery by 43% — the relationship is mathematically direct

- Right-party contact rate improvement has a compounding effect on Regulation F compliance — more recoveries per attempt means fewer total attempts needed to meet recovery targets

- The primary driver of improvement is per-account contact timing based on behavioral signals — not better scripts, higher call volume, or more agents

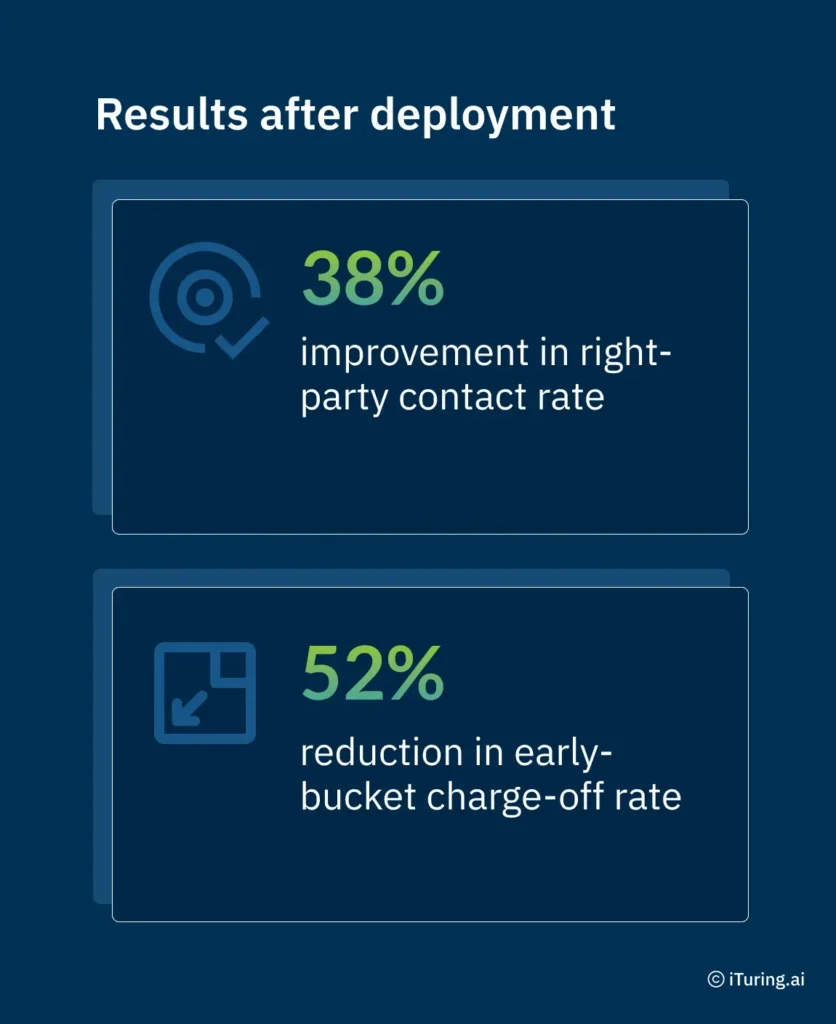

- iTuring US bank deployments: 38% right-party contact improvement, 52% early-bucket charge-off reduction, documented in SR 11-7 examination evidence

What 26% Right-Party Contact Rate Costs a US Bank in Wasted Regulation F Frequency Budget Per Week

A 26% right-party contact rate means that for every 100 outbound collection attempts, a bank reaches the actual account holder only 26 times. The remaining 74 attempts hit voicemail, wrong numbers, disconnected lines, or household members who cannot authorize payment. Each of those failed attempts still costs money: agent time, telephony charges, compliance logging, and most critically, a deduction from the finite number of contact attempts permitted under Regulation F’s 7-in-7 frequency cap. For a bank running 50,000 outbound attempts per week, roughly 37,000 of those attempts produce zero recovery opportunity while consuming both operational budget and regulatory headroom.

This baseline persists because most US bank collections operations still rely on static dialler strategies. Accounts are prioritized by days past due or balance size, and call times are set by broad demographic segments rather than individual behavioral patterns. The dialler does not know that Account 4471 answers calls at 2:15 PM on Tuesdays or that Account 8832 has historically responded only to SMS. Without per-account timing intelligence, the operation defaults to a spray-and-pray model that burns through Regulation F frequency budget at an alarming rate.

The gap between 26% and 46% right-party contact is not incremental. US bank collections right-party contact rates average 26-32% with manual dialler operations; AI propensity timing improvements to 43-51% are documented across iTuring US bank deployments (iTuring US Bank Collections Deployment Data 2024-25). Improving right-party contact rate from 26% to 46% reduces cost per recovery by 43% at equivalent call volume, a relationship that is mathematically direct and predictable (ABA Collections Analytics Model and iTuring Benchmark Data 2025). For a mid-size bank with $200 million in delinquent balances, that 20-point improvement translates to millions in recovered dollars and a measurable reduction in operational expense. This represents the core US bank collections contact rate benchmark that AI propensity timing is redefining.

Why Contact Timing Is the Highest-Leverage Variable for Right-Party Contact Rate Improvement

- Account prioritization determines which accounts receive contact attempts first, and this sequencing has a disproportionate effect on right-party contact rate. When a dialler works through accounts sorted only by days past due, it treats a 15-day delinquent account with strong self-cure probability the same as a 15-day account showing behavioral signals of extended default. AI-driven prioritization reorders the queue so that accounts most likely to answer and most likely to need intervention receive attempts first. A regional US bank with 30,000 delinquent accounts can see its right-party contact rate climb by 8-12 percentage points simply by reordering the call queue based on predicted answer probability rather than static delinquency buckets.

- Channel and timing selection directly controls cost per contact. Calling an account holder at 10 AM when historical data shows they answer at 6 PM wastes an attempt and a Regulation F contact slot. Per-account propensity models analyze prior answer patterns, payment timing, device usage, and even payroll cycle signals to predict the optimal contact window and channel for each individual account. A community bank right-party contact improvement through AI timing means that the same agent workforce, making the same number of calls, reaches 40-50% more account holders because each attempt lands during a window where the borrower is available and receptive.

- Self-cure identification removes accounts from the contact queue entirely when predictive signals indicate the borrower will pay without intervention. Industry data shows that 15-25% of early-stage delinquent accounts self-cure within 30 days. Every call made to a self-cure account is a wasted attempt that could have been directed toward an account requiring human intervention. By identifying and suppressing self-cure accounts, AI timing models reduce total contact volume while concentrating agent effort on accounts where outreach changes the outcome.

- Compliance cost reduction flows directly from higher right-party contact rates. When a bank needs fewer total attempts to reach the same number of account holders, it generates fewer compliance events to log, fewer potential FDCPA or CFPB violations to monitor, and fewer Regulation F frequency calculations to track. For a Head of Collections presenting to a CFO, this is the multiplier effect: higher right-party contact rates reduce not only direct collection costs but also the indirect compliance overhead that scales with attempt volume.

26% to 47% Right-Party Contact Rate: What Per-Account Propensity Timing Data Shows

The evidence for right-party contact rate improvement through AI propensity timing comes from production deployments across US banks ranging from community institutions under $10 billion in assets to mid-size banks with diversified consumer portfolios. The consistent variable driving improvement is per-account contact timing: predicting when each individual borrower is most likely to answer, on which channel, and whether outreach is necessary at all. The comparison below shows the specific metrics across deployment cohorts.

| Metric | Before AI | With iTuring |

| Cost per recovery | $85-140 (manual) | $38-62 (AI-first) |

| Right-party contact rate | 26-32% | 43-51% |

| Early-stage charge-off rate | Industry baseline | 52% reduction |

| SR 11-7 documentation time | 3-8 weeks per exam | 30 minutes — automated |

| Model retraining | Quarterly at best | Continuous with audit trail |

Results vary by portfolio composition, starting baseline, and data maturity – figures above reflect median outcomes across US banks deployments.

Translating 20 Percentage Points of Right-Party Contact Improvement Into Recovery Dollars

Building the ROI case for AI propensity timing requires five concrete steps that a Head of Collections can present with confidence to finance leadership.

Step 1: Establish the current baseline honestly. A 26% right-party contact rate with a manual dialler running at $110 per recovery is the anchor for this calculation. This baseline reflects the typical US bank collections contact rate before AI improvement, and it is the number that makes the business case credible. Pull this from your dialler reporting, not from vendor benchmarks or aspirational targets.

Step 2: Estimate the improvement potential using a 46% right-party contact rate as the target. This figure sits in the middle of the 43-51% range documented across iTuring deployments and represents a conservative projection for most US bank portfolios. The improvement potential depends on data maturity: banks with 12+ months of detailed call-level data will reach the upper end of the range faster. US bank collections propensity timing through AI improvement is most predictable when historical answer-rate data exists at the account level.

Step 3: Calculate recovery uplift using the 38% improvement in right-party contact rate. If your current operation recovers $4.2 million per month at 26% right-party contact, a 38% improvement in contact rate does not produce a 38% increase in recoveries, but the relationship is strong. Each additional right-party contact represents a new recovery opportunity. Conversion rates on right-party contacts typically range from 18-35% depending on delinquency stage, so the recovery uplift calculation multiplies additional contacts by your existing conversion rate.

Step 4: Calculate cost reduction using the 52% reduction in early-bucket charge-off rate. Early-bucket charge-offs are the most expensive failures in a collections operation because they represent accounts that moved from 30-day delinquency to charge-off without meaningful intervention. A 52% reduction in this metric means that more than half of accounts previously lost to charge-off are now being contacted, worked, and resolved in early stages where cure rates are highest and recovery amounts are largest.

Step 5: Apply the compliance cost adjustment. For banks under active CFPB or state AG scrutiny, the compliance cost of each outbound attempt includes not just telephony and agent time but also monitoring, documentation, and potential enforcement exposure. Reducing total attempt volume by 30-40% while increasing right-party contacts produces a compliance cost reduction that can exceed the direct operational savings.

The calculation only works if the baseline is honest – start with 26% right-party contact – manual dialler at $110 per recovery as the anchor, not an aspirational figure.

38% Right-Party Contact Rate Improvement at a US Community Bank: The Evidence

A US community bank with assets under $10 billion faced a persistent 26% right-party contact rate across its consumer lending portfolio, resulting in escalating early-bucket charge-offs and a cost per recovery that exceeded $120 per account. The institution deployed iTuring Collections Agent with per-account propensity timing models, reaching full production within 14 days using the iTuring Data Accelerator’s pre-built financial features to eliminate the typical months-long data engineering phase.

Results after deployment:

Right-Party Contact Rate Is the Multiplier: What Moving From 26% to 46% Does to US Bank Collections Economics

Right-party contact rate is the single metric that most directly predicts collections P&L performance, and a 20-point improvement compresses cost per recovery, extends Regulation F frequency budget, and reduces charge-off volume simultaneously. For a CFO evaluating AI investment in collections, the question is not whether the math works but whether the baseline measurement is accurate enough to project returns with confidence. Banks that have deployed per-account timing models report that the improvement holds across delinquency stages, portfolio types, and seasonal variation, making it one of the most stable performance gains available in consumer collections operations.

The difference between a 26% and a 46% right-party contact rate is not a marginal operational improvement. It is a structural change in collections economics that affects cost per recovery, charge-off rates, Regulation F compliance exposure, and agent productivity simultaneously. The math is direct: more right-party contacts at the same call volume means more recovery opportunities, lower cost per dollar collected, and fewer wasted regulatory frequency slots.

For banks still operating with static dialler strategies, the first step is measuring the current right-party contact rate accurately at the account level, not the campaign level. The second step is testing whether per-account propensity timing can move that number using your own historical data.

iTuring’s per-account contact timing optimization is testable against your bank’s historical answer rate data before full deployment – request a proof of concept before any licence decision.