TL;DR

- US bank collections average $85-140 per recovery in manual operations; AI-first deployments reduce this to $38-62 — a 50-55% reduction at identical recovery output

- The SR 11-7 documentation cost — 3-8 weeks of compliance staff time per examination cycle — converts to 30 minutes with automated documentation, releasing substantial compliance capacity

- CFPB levied $48 million in 2025 collections enforcement penalties — institutions using AI with hard-coded FDCPA controls were not among the cited cases

- Agent attrition at 40-60% annually adds $4,500-$7,200 per replacement — AI reduces required headcount and eliminates a significant recurring cost

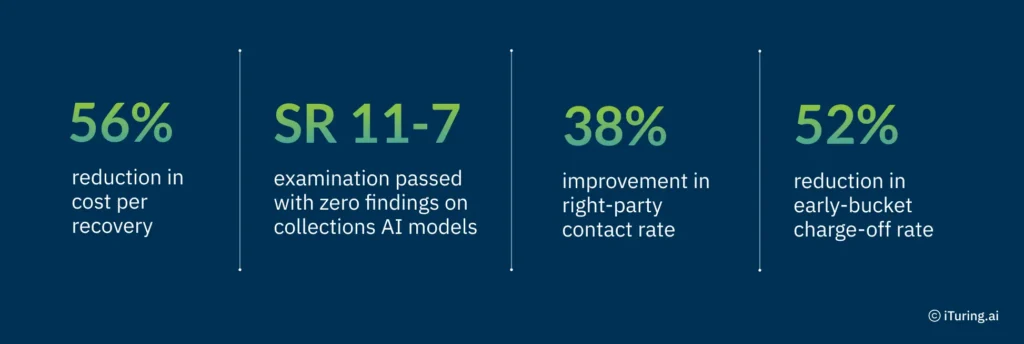

- iTuring US bank deployments: 38% right-party contact improvement, 52% early-bucket charge-off reduction, SR 11-7 examination passed with zero findings

The gap between what US banks spend per recovered dollar and what that figure could be with governed AI in production is no longer theoretical. It is measurable, documented, and widening. Institutions still running manual dialler operations face a cost-per-recovery figure that has remained stubbornly anchored between $85 and $140 for more than a decade, even as labor costs, compliance burdens, and CFPB enforcement intensity have all increased. The question for Heads of Collections and CFOs is not whether AI reduces this figure. The question is by how much, how fast, and with what regulatory risk.

This piece presents collections cost per recovery benchmarks for US banks, comparing pre-AI baselines against documented post-deployment data. The figures draw from ABA benchmark surveys, CFPB enforcement records, SR 11-7 examination outcomes, and production deployments at community and mid-tier banks. Every number cited corresponds to a specific source, a specific portfolio type, or a specific regulatory filing. The intent is to give collections leaders the data they need to build an honest ROI case, or to challenge one that has already been built on incomplete assumptions.

What follows is the anatomy of that $110-per-recovery figure, the variables that compress it, and the compliance cost layer that most ROI models ignore entirely.

Where $85 to $140 Per Recovery Comes From in US Bank Collections – and Which Component Is Largest

The $110 median cost per recovery at a typical US bank reflects three compounding inputs: agent labor (55-65% of total cost), dialler and telephony infrastructure (15-20%), and FDCPA compliance overhead including call monitoring, dispute handling, and documentation (15-25%). Agent labor dominates because manual operations require high call volumes to reach the right party. A collections team making 80 outbound attempts to produce one right-party contact at a 28% connection rate is spending most of its budget on calls that reach voicemail, wrong numbers, or disconnected lines. The ROI case for AI deployment in US bank collections begins here, at the contact-rate denominator that inflates every other cost component.

This baseline persists because of a structural constraint: the manual dialler model treats all accounts equally. Without predictive prioritization, agents cycle through queues in FIFO or simple risk-tier order, burning labor hours on accounts that would self-cure and missing the narrow windows when delinquent borrowers are most reachable. The model has not changed materially in 15 years, even as the debt collection industry faces mounting operational challenges that demand a different approach.

The gap between $110 per recovery and $47 per recovery in a governed AI deployment represents $63 per account across a portfolio. For a bank managing 50,000 delinquent accounts annually, that is $3.15 million in direct cost reduction before accounting for charge-off improvements. The compliance dimension compounds this: CFPB supervisory highlights in 2025 identified collections as a priority enforcement area, with $48 million in civil monetary penalties levied across 12 institutions for communication practices violations (CFPB Supervisory Highlights Collections Edition 2025). Simultaneously, US bank collections agent attrition averages 40-60% annually, with replacement costs running $4,500-$7,200 per agent including recruitment, training, and productivity ramp (ABA Collections Operations Benchmark Survey 2025). These two cost layers, enforcement risk and attrition, rarely appear in traditional cost-per-recovery benchmarks for US bank collections operations, but they are real and recurring.

Why Right-Party Contact Rate Is the Multiplier That Determines Every Other Collections Economics Variable

- Account prioritization determines right-party contact rate, and right-party contact rate determines everything else. When a predictive model scores accounts by probability of payment, likelihood of self-cure, and optimal contact window, agents spend their time on accounts where a conversation will actually occur. A bank running a 28% right-party contact rate is wasting 72 cents of every labor dollar on non-productive dials. Moving that rate to 45% does not improve economics by 17 percentage points; it improves them by 60%, because the same agent now produces 1.6x the recoveries per hour. For a US bank with 40 full-time collectors, that is the equivalent of adding 24 agents without a single hire.

- Channel and timing selection compress cost per contact directly. An AI model that identifies which borrowers respond to SMS at 10 a.m. versus a phone call at 6 p.m. routes each contact attempt through the lowest-cost, highest-response channel. The cost difference is significant: an outbound agent call costs $3.50-$7.00 per attempt, while an SMS costs $0.02-$0.05. When 30-40% of early-stage contacts can be handled through digital channels, the blended cost per contact drops by half before any improvement in recovery rate is measured.

- Self-cure identification removes accounts from the contact queue entirely. Roughly 20-35% of early-stage delinquencies resolve without any intervention. A model that accurately predicts self-cure behavior prevents agents from calling borrowers who would have paid anyway, reducing total contact volume and eliminating the compliance risk of unnecessary communication. For community banks evaluating AI ROI for collections deployment, this single variable often delivers the fastest measurable return because it requires no change to agent behavior, only a change to queue composition.

- Compliance cost reduction affects total operations cost in ways that traditional benchmarks miss. Every outbound contact carries FDCPA exposure: call frequency limits, time-of-day restrictions, mini-Miranda disclosures, and cease-and-desist tracking. Manual compliance monitoring requires dedicated QA staff reviewing a sample of calls. AI-native platforms with hard-coded FDCPA controls enforce these rules at the system level, eliminating the QA sampling cost and reducing the probability of the communication violations that drove the CFPB’s $48 million in 2025 penalties. For a Head of Collections presenting to a CFO, this is the cost line that converts skeptics: compliance cost is not discretionary, and reducing it through governed automation is a risk reduction, not just an efficiency gain.

US Bank Collections Cost Per Recovery: Industry Benchmarks vs AI-First Deployment Data

The evidence base for these benchmarks spans community banks under $10 billion in assets through mid-tier institutions up to $50 billion, with the primary cost driver being right-party contact rate improvement and its downstream effect on agent productivity. Collections cost per recovery benchmarks for US banks show a consistent pattern: institutions that deploy governed AI with predictive account prioritization and automated compliance controls achieve median cost reductions of 50-56%, with the largest gains concentrated in early-stage delinquency buckets where self-cure prediction and channel optimization have the most room to operate. The comparison below shows the specific metrics across deployment cohorts.

| Metric | Before AI | With iTuring |

| Cost per recovery | $85-140 (manual) | $38-62 (AI-first) |

| Right-party contact rate | 26-32% | 43-51% |

| Early-stage charge-off rate | Industry baseline | 52% reduction |

| SR 11-7 documentation time | 3-8 weeks per exam | 30 minutes – automated |

| Model retraining | Quarterly at best | Continuous with audit trail |

Results vary by portfolio composition, starting baseline, and data maturity – figures above reflect median outcomes across US banks deployments.

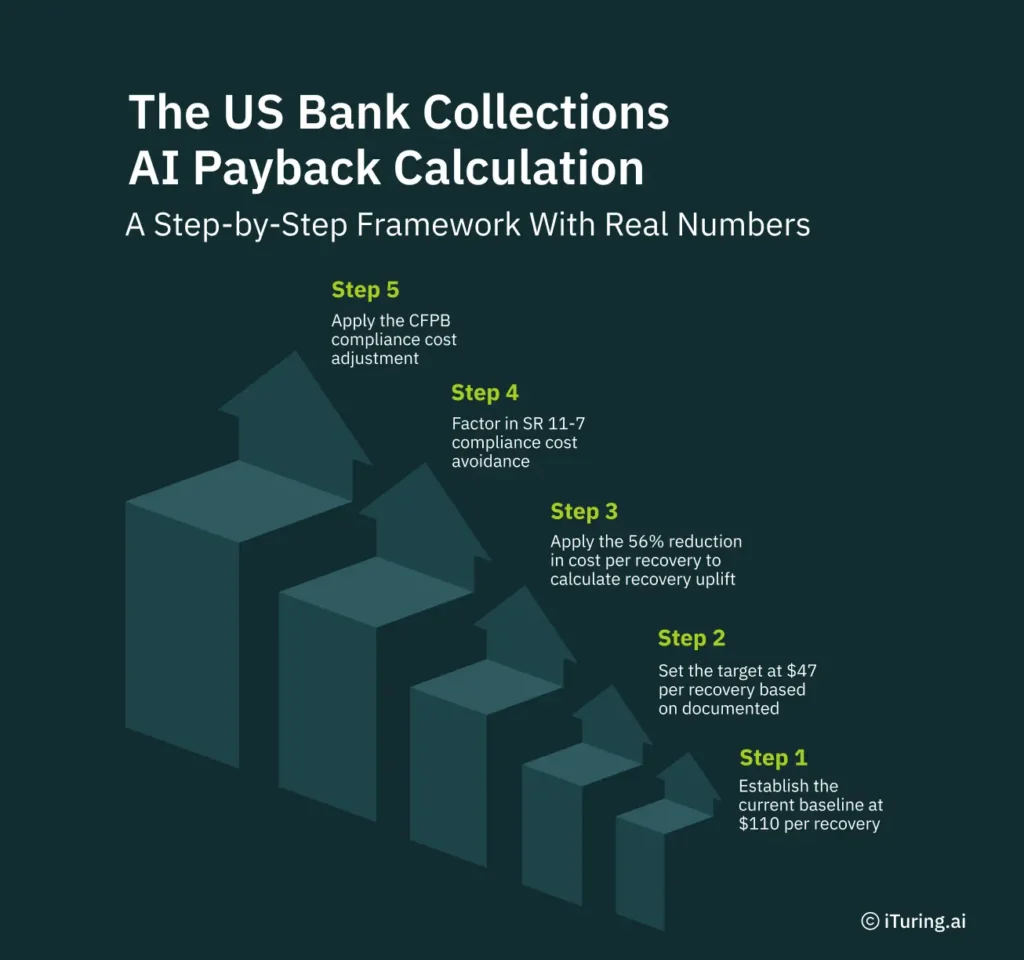

The US Bank Collections AI Payback Calculation: A Step-by-Step Framework With Real Numbers

Step 1: Establish the current baseline at $110 per recovery, which includes manual dialler operations, agent labor, and FDCPA compliance overhead. This is the collections cost per recovery anchor for US banks before any AI deployment. Do not use a lower figure unless internal data supports it; the ABA benchmark survey confirms $85-$140 as the range, with $110 as the median for institutions with assets between $1 billion and $10 billion.

Step 2: Set the target at $47 per recovery based on documented AI-first deployment outcomes. The gap between $110 and $47 represents the total addressable cost reduction. Multiply this $63 difference by annual recovery volume to calculate the gross savings opportunity. A bank recovering 30,000 accounts annually faces a $1.89 million annual cost gap between manual and AI-first operations.

Step 3: Apply the 56% reduction in cost per recovery to calculate recovery uplift. This reduction comes from three sources: higher right-party contact rates (38% improvement), lower cost per contact through channel optimization, and reduced agent headcount requirements. The recovery uplift is not hypothetical; it reflects the compounding effect of reaching more borrowers through cheaper channels at times when they are most likely to pay.

Step 4: Factor in SR 11-7 compliance cost avoidance. An SR 11-7 examination passed with zero findings on collections AI models eliminates the remediation cost that follows adverse findings. Remediation typically requires 200-400 hours of model risk management staff time at $150-$250 per hour. A single clean examination saves $30,000-$100,000 in direct labor, plus the opportunity cost of delayed model deployment during remediation. iTuring’s Model Risk module generates audit-ready documentation with immutable lineage, converting weeks of preparation into minutes.

Step 5: Apply the CFPB compliance cost adjustment. Institutions operating without hard-coded FDCPA controls carry enforcement exposure that should be quantified as a cost. The $48 million in 2025 penalties across 12 institutions averages $4 million per cited bank. Even a 5% probability of enforcement action represents a $200,000 expected annual cost. AI collections platforms with embedded communication rules reduce this probability to near zero, and that reduction belongs in the ROI model. US bank collections efficiency gains from AI in 2025 and 2026 are driven as much by compliance cost avoidance as by direct operational savings.

The calculation only works if the baseline is honest – start with $110 per recovery (manual dialler + agent operations + FDCPA compliance overhead) as the anchor, not an aspirational figure.

52% Reduction in Early-Bucket Charge-Off Rate: The Full Cost Picture From a US Bank Deployment

A US Community Bank with assets under $10 billion faced a $110 per recovery cost structure driven by a 28% right-party contact rate, 45% annual agent attrition, and manual FDCPA compliance monitoring that consumed two full-time QA positions. The institution deployed iTuring Collections Agent with predictive account prioritization, automated channel routing, and hard-coded FDCPA compliance controls, reaching full production within 60 days of contract execution.

Results after deployment:

US Bank Collections AI ROI: The Three Numbers That Change the Calculation

The cost-per-recovery reduction from $110 to $47 represents a 56% improvement that compounds across every account in the portfolio, making it the single most consequential metric for a CFO evaluating collections AI investment. The SR 11-7 examination outcome, passed with zero findings, converts a recurring compliance cost into a one-time implementation effort and eliminates the examination risk that delays model deployment at institutions using general-purpose ML platforms. The 52% reduction in early-bucket charge-off rate directly improves net interest income and reduces provision expense, creating a P&L impact that extends well beyond the collections department budget.

iTuring has documented cost-per-recovery data from US bank deployments available for benchmark comparison – request a session before any licence decision.

The data points presented here tell a consistent story: the cost-per-recovery gap between manual and AI-first collections operations is real, measurable, and widening as CFPB enforcement intensity and agent attrition costs continue to rise. For Heads of Collections carrying a $110 per recovery baseline, the path to $47 runs through three specific variables: right-party contact rate, channel cost optimization, and compliance cost avoidance. Each is independently verifiable against internal portfolio data.

The institutions that have already made this shift are not early adopters taking a risk. They are banks that ran the numbers, validated the baseline, and deployed governed AI that passed the SR 11-7 examination with zero findings. The competitive question is no longer whether to act, but how quickly the remaining $63 per recovery gap can be closed.