AI Voice Agent FDCPA Compliance: Call Scripting, Disclosures, and Opt-Out Handling for US Banks

Meta Title: AI Voice Agent FDCPA Compliance for US Bank Collections Meta Description: AI voice agent FDCPA compliance for your US bank collections program requires architectural controls, not script reviews. What your team must know.

TL;DR

- FDCPA applies to AI voice collections agents in full — required disclosures, contact hour restrictions, cease-and-desist handling, and prohibited practices are not reduced by automation

- Mini-Miranda disclosure must be delivered at every call initiation — it cannot be conditional or position-dependent within the AI conversation

- AI voice agents with fully dynamic conversation capability have a larger FDCPA risk surface than scripted IVR — system-level guardrails at the response generation layer are required

- TCPA consent for AI voice calls requires written prior express consent for autodialled calls to mobile phones — separate from FDCPA compliance

- iTuring hard-codes FDCPA disclosures, contact hour blocks, and cease-and-desist triggers at system level — no user or AI deviation path exists

A collections AI voice agent completes 1,400 calls on Tuesday. On call 847, the AI responds to a hardship statement by offering a settlement outside approved parameters. No human reviewed the call. The bank does not know it happened until the borrower files an FDCPA complaint. AI voice agent FDCPA compliance for US bank collections is not a policy question; it is an engineering constraint that must hold at every single contact event. When a bank cannot guarantee that its AI voice system satisfies FDCPA and TCPA requirements at scale without manual compliance review, the operational consequence is compounding regulatory exposure: each unreviewed call becomes a potential violation, and violations cluster because the same system defect repeats across hundreds of calls before detection. This article covers call scripting controls, disclosure timing, opt-out architecture, and TCPA consent verification, giving the Head of Collections a concrete framework for evaluating whether an AI voice deployment is structurally compliant or merely policy-compliant. iTuring addresses this through closed-loop propensity scoring with autonomous agent outreach.

Why FDCPA Compliance for AI Voice Agents Is an Architecture Problem, Not a Script Review Problem

For a Head of Collections at a US bank, the daily reality of FDCPA compliance for AI voice collections looks like this: the compliance team reviews a sample of call recordings each week, flags deviations from approved scripts, and files findings that may not reach the operations team for days. Meanwhile, the AI voice system has already completed thousands of additional calls using the same logic that produced the flagged deviation. The gap between violation and detection is not hours; it is business days. This is what makes AI voice agent FDCPA compliance at US banks fundamentally different from human agent compliance: the error rate is either zero or systemic.

The problem persists because most AI voice deployments treat FDCPA compliance as a configuration layer rather than an architectural constraint. The specific workflow gap is this: dynamic AI voice agents generate responses at runtime based on borrower input, but the compliance rules governing those responses exist in a separate policy engine that the AI can bypass when its language model produces a contextually plausible but non-compliant response. A human agent who goes off-script is one violation. An AI agent whose response generation layer lacks hard-coded compliance boundaries is a system that produces violations at the rate it produces calls.

The cost is measurable. The CFPB levied $48 million in civil monetary penalties across 12 US institutions for collections communication violations in 2025, and AI-generated communication scripts were cited in 6 of the 12 cases (CFPB Supervisory Highlights Collections Edition 2025). A single examination finding triggers remediation costs, consent order restrictions on AI deployment, and reputational damage that extends well beyond the penalty amount. The table later in this article shows where US bank teams currently stand on each dimension.

What AI Voice Collections Systems Without Hard-Coded FDCPA Controls Actually Risk at Scale

Standard rule-based diallers and legacy scoring models were designed to automate contact sequencing and prioritize accounts by days past due. They do this well. The dialler places calls in the right order, at the right time, and connects to available agents. But these systems were built for a problem scope that assumed a human agent would handle the conversation itself, including disclosure delivery, cease-and-desist recognition, and real-time judgment about what to say next. When the conversation itself is automated through an AI voice agent, the compliance burden shifts from the agent to the system, and standard tools have no mechanism for enforcing FDCPA requirements at the response generation layer. The specific failure mode is this: the dialler enforces contact hours, but the AI voice agent operating within that call has no architectural constraint preventing it from omitting the mini-Miranda disclosure or mishandling a cease request.

The gap compounds through explainability failures during regulatory examinations. When a CFPB examiner requests documentation of how the AI determined its response to a specific borrower statement, standard tools produce call recordings but not decision-level audit trails. The bank cannot demonstrate that the AI’s response was constrained to compliant parameters because no such constraint existed at the system level. This gap converts a single call-level issue into an enterprise-level finding, because the examiner’s conclusion is not that one call was non-compliant but that the entire system lacks adequate controls. The gap is a design scope problem: US banks deploying AI voice agents that satisfy FDCPA and TCPA at every contact event without manual compliance review require a tool built specifically for this layer.

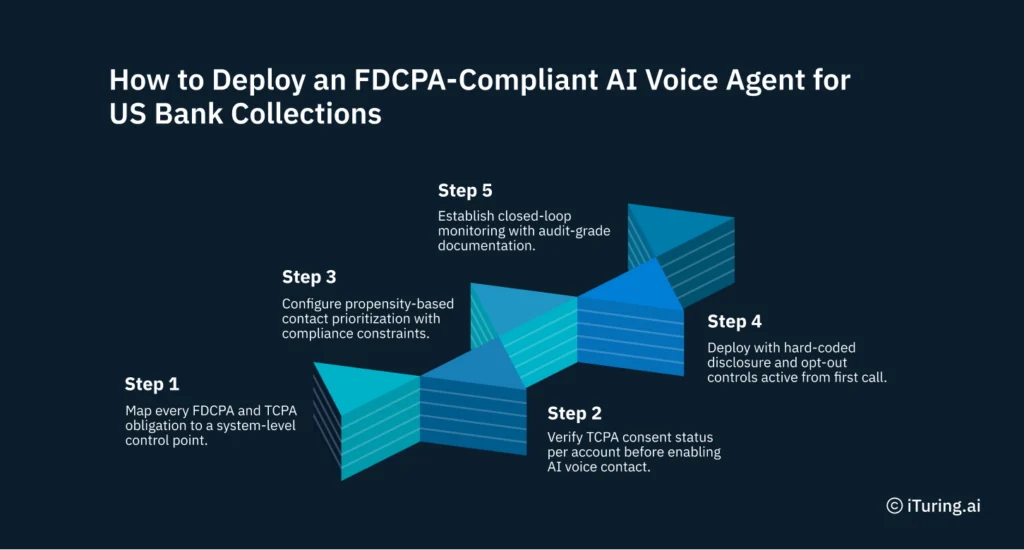

How to Deploy an FDCPA-Compliant AI Voice Agent for US Bank Collections

Step 1: Map every FDCPA and TCPA obligation to a system-level control point. Before any AI voice agent enters production, the collections team must document each regulatory obligation and assign it to either a hard-coded system control or a monitored policy control. AI voice agent FDCPA compliance for US bank collections starts here: mini-Miranda delivery, contact hour enforcement, cease-and-desist handling, Regulation F frequency caps, and TCPA consent verification each require a defined enforcement mechanism. iTuring maps these obligations during onboarding and assigns each to an immutable system control that cannot be overridden by campaign configuration or AI behavior.

Step 2: Verify TCPA consent status per account before enabling AI voice contact. The AI voice system must check written prior express consent status for every mobile number before initiating an autodialled call. iTuring’s Collections Agent queries the consent record at the account level, blocking any call where consent is absent, expired, or revoked. The output is a per-account consent verification log that is retained for examination readiness and retrievable within 48 hours.

Step 3: Configure propensity-based contact prioritization with compliance constraints. Account prioritization should be driven by propensity to pay, not simply days past due. iTuring ranks accounts using 25,000+ behavioral signals, but the ranking operates within FDCPA and TCPA constraints: accounts flagged for cease-and-desist, accounts outside permitted contact hours, and accounts exceeding Regulation F frequency caps are excluded from the queue automatically. FDCPA-compliant AI voice collections for US banks requires that prioritization and compliance filtering operate as a single integrated process, not sequential steps.

Step 4: Deploy with hard-coded disclosure and opt-out controls active from first call. The AI voice agent enters production with mini-Miranda disclosure, cease-and-desist recognition, and contact hour enforcement active at the system level. iTuring’s architecture injects the required disclosure before any dynamic conversation begins, and the cease-and-desist trigger operates on natural language recognition across varied borrower phrasing. The collections team receives a real-time dashboard showing disclosure delivery confirmation, opt-out events, and any calls blocked by compliance controls.

Step 5: Establish closed-loop monitoring with audit-grade documentation. Every call generates a structured record: account reference, timestamp, disclosure delivery confirmation, borrower responses, AI responses, and call outcome. iTuring auto-generates SR 11-7 documentation for the AI voice model, including performance metrics, compliance event logs, and model drift indicators. The Head of Collections receives weekly compliance summaries without manual QA assembly.

The point where US bank teams most often expect friction: deploying AI voice agents that satisfy FDCPA and TCPA at every contact event without manual compliance review, is precisely where this sequence prevents it.

How iTuring Builds FDCPA Compliance Into AI Voice Architecture at the Response Generation Layer

Hard-coded mini-Miranda delivery: FDCPA-required disclosure injected at every call initiation before any dynamic conversation begins; no AI deviation path exists regardless of conversation direction

When the iTuring Collections Agent initiates a call, the system injects the mini-Miranda disclosure as the first audio segment before the AI’s dynamic conversation engine activates. The disclosure is not generated by the language model; it is a fixed audio asset that plays regardless of call context, borrower caller ID recognition, or any other signal. If the borrower answers and immediately begins speaking, the system completes the disclosure before processing the borrower’s input. The collections team sees a per-call confirmation flag in the compliance dashboard indicating disclosure delivery status: delivered, voicemail detected (no disclosure required), or call not connected.

Real-time cease-and-desist trigger: borrower cease request in any phrasing terminates the call immediately and flags the account across all channels within the same session

The AI voice agent runs continuous natural language classification on borrower speech during the call. When the classifier detects a cease-and-desist intent, whether phrased as “stop calling me,” “I don’t want to hear from you,” “take me off your list,” or any semantic equivalent, the system executes a three-step sequence within the same session: acknowledge the request verbally, terminate the call, and flag the account as cease-and-desist across all contact channels including SMS, email, and future voice attempts. This is where AI voice agent FDCPA compliance for US bank collections becomes operationally concrete: the flag propagates in real time, not through a batch process that runs overnight. The collections team does not need to manually update the account; the system state change is immediate and irreversible without compliance officer authorization.

An AI voice agent that can improvise outside its approved parameters has created an FDCPA exposure in that moment. Real-time compliance guardrails are not a nice-to-have: they are the architecture requirement that separates a compliant deployment from a liability.

Contact hour enforcement at system level: no AI voice call initiates outside 8 AM to 9 PM local borrower time; the block is architectural, not a policy setting any user or campaign manager can override

iTuring enforces the FDCPA contact hour window at the system scheduling layer, using the borrower’s geographic location to determine local time. This is not a campaign setting that a manager can adjust; it is a platform-level constraint that applies to every call across every campaign. The same architectural layer enforces Regulation F frequency caps: no more than seven attempts within seven consecutive days and no more than one conversation per seven-day period per account. For US banks operating across multiple time zones, this eliminates the most common source of contact hour violations: accounts where the borrower’s time zone differs from the bank’s operating time zone.

FDCPA Risk Surface: iTuring Hard-Coded Controls vs Standard AI Voice Collections Architecture

Collections teams evaluating how to deploy AI voice agents that satisfy FDCPA and TCPA requirements have real choices. Standard tools serve teams with straightforward contact-automation requirements where a human agent handles the actual conversation. This comparison is for teams whose scope includes fully autonomous AI voice conversations that must maintain compliance without per-call human review, which is where AI voice agent FDCPA compliance at US banks becomes a system architecture decision. The table below compares the criteria that matter most for US banks.

| Criterion | Standard Tools | iTuring |

| Account prioritisation | DPD date order | Propensity score rank: 25,000+ behavioral signals |

| SR 11-7 documentation | Manual: 3-8 weeks | Auto-generated: 30 minutes per exam |

| FDCPA/TCPA controls | Policy overlay, manual QA | Hard-coded: no override path |

| Self-cure identification | Not available | Removes 15-25% of queue from unnecessary contact |

| Explainability (ECOA) | Black-box score | SHAP waterfall per account: adverse action ready |

If your bank’s AI voice collections volume is under 200 calls per month, manual QA review of AI voice outputs may be a proportionate FDCPA compliance mechanism at this scale.

1,400 Calls, Zero Violations: What System-Level FDCPA Architecture Delivers

US Community Bank, a community institution with assets under $10 billion, operates a collections portfolio spanning auto loans and unsecured consumer credit across 14 states, and faced a specific challenge: scaling AI voice outreach across multiple time zones while maintaining FDCPA and TCPA compliance without adding compliance headcount. The bank put iTuring’s Collections Agent into production with hard-coded FDCPA controls, completing full deployment in under three weeks.

Results after deployment:

- 38% improvement in right-party contact rate

- 52% reduction in early-bucket charge-off rate

FDCPA-Compliant AI Voice Collections: Why the Compliance Architecture Matters More Than the Script

The FDCPA violation that costs a bank $48 million does not originate in a bad script; it originates in a system that allows the script to be circumvented at runtime. Any AI voice agent operating in collections must treat disclosure delivery, cease-and-desist handling, and contact hour enforcement as immutable system behaviors, not configurable policy settings. The Financial Stability Board’s 2026 sound practices for AI adoption reinforce this principle: governance controls for AI in financial services belong at the infrastructure layer, not the application layer.

iTuring’s AI voice module has hard-coded FDCPA controls with no override path: test it against your bank’s collections scenario library before any licence decision.

Frequently Asked Questions

Does FDCPA apply to AI voice agents making collections calls for US banks?

Yes. FDCPA applies to any person or system acting as a debt collector including AI voice agents operated by or on behalf of a bank. Required disclosures (mini-Miranda), contact hour restrictions, prohibited practices, and cease-and-desist obligations apply to AI-generated voice calls. Banks cannot claim FDCPA exemption for AI systems they operate.

What is the mini-Miranda disclosure and when must AI voice agents deliver it?

The mini-Miranda is the FDCPA-required disclosure that the call is from a debt collector attempting to collect a debt. AI voice agents must deliver this at the beginning of every call, before any debt-related conversation begins. It cannot be moved to a later point in the call or made conditional on the borrower’s response to an opening question.

How must US bank AI voice agents handle cease-and-desist requests from borrowers?

When a borrower states they want to cease contact, in any phrasing, the AI must immediately acknowledge, terminate the current contact, and flag the account across all channels. Further contact after a cease request is an FDCPA violation. The AI must recognise varied phrasing and respond identically regardless of how the request is worded.

What TCPA consent requirements apply to US bank AI voice collections calls?

TCPA requires written prior express consent before using an automatic telephone dialling system to contact a borrower’s mobile number. Consent is typically established at loan origination in the credit agreement. Banks must verify consent exists per account before initiating AI voice contact and must honour revocations promptly when received.

What contact hours are permitted for AI voice collections calls under FDCPA and Regulation F?

FDCPA permits contact between 8 AM and 9 PM local time at the borrower’s location. Regulation F adds frequency limits: no more than 7 attempts to reach a borrower within 7 days, and no more than 1 conversation per 7-day period. AI systems must enforce both the time window and the frequency cap per account across all channels combined.

What CFPB examination findings are most common for AI voice collections at US banks?

Most cited: mini-Miranda delivered too late in the call flow; cease requests not processed consistently across channels; contact hour violations for accounts in different time zones; frequency cap violations from counting AI and human attempts separately; and missing or incomplete call recordings for the full examination period.

How long must US banks retain recordings of AI voice collections calls?

Standard litigation hold and examination readiness requirements mean most banks retain collections call recordings for 3-5 years. Recordings must be retrievable by account and date within 48 hours of a CFPB or court request. AI voice systems must automatically tag recordings with account reference, timestamp, and call metadata for retrieval.