TL;DR

- NBFC NPA recovery rates average 51-58% on unsecured portfolios with reactive collections — AI pre-delinquency and propensity treatment pushes this to 74-82%

- Recovery rate is determined at the 1-30 DPD stage, not the 90 DPD stage — the intervention timing is what drives the board-level number

- Every 30-day delay in collections intervention reduces recovery probability by 5-8 percentage points — the compounding effect across a portfolio is measurable on the balance sheet

- NPA recovery rate improvement is the metric that changes provisioning requirements, CRAR calculations, and RBI supervisory conversations simultaneously

- iTuring deployments show 116% increase in collections recovery rate and 39-44% higher collection rates across all delinquency buckets

The difference between an NBFC that reports a 54% NPA recovery rate and one that reports 80% is rarely about the quality of its collections agents. It is almost always about when and how the institution intervenes on a delinquent account. Indian non-bank lenders are now growing faster than banks as AI changes lending and collections economics, and the operational data from these deployments is finally mature enough to quantify what works.

This data set draws from 18 NBFC collections deployments between 2024 and 2025. The portfolios span unsecured personal loans, consumer durable finance, and microfinance. The findings are specific: recovery rate improvement at Indian NBFCs before and after AI deployment follows a consistent pattern, and the variables that drive it are identifiable. The question for a Chief Risk Officer is not whether AI collections work, but what baseline your institution starts from and how quickly the provisioning impact becomes visible to the board.

The numbers here are not projections. They are median outcomes from production environments, and they carry implications for provisioning, CRAR, and the next RBI supervisory conversation.

What a 54% NPA Recovery Rate Means for an NBFC’s Provisioning and Board Reporting

A 51-58% NPA recovery rate on unsecured portfolios means that for every Rs. 100 crore classified as non-performing, the NBFC recovers Rs. 51-58 crore and writes off or provisions for the rest. The cost driver is not just the unrecovered principal: it is the provisioning requirement that the remaining Rs. 42-49 crore triggers under RBI norms. For an NBFC with Rs. 2,000 crore in gross NPAs, the difference between 54% and 80% recovery is not a collections metric. It is a Rs. 520 crore swing in provisioning exposure. This is the context in which NPA recovery rate improvement through AI deployment at Indian NBFCs becomes a board-level discussion, not an operations project.

The baseline persists because most NBFC collections operations are reactive. Agents work accounts after they cross 30 or 60 DPD, using static call lists sorted by outstanding balance. There is no propensity scoring, no channel optimization, and no mechanism to identify accounts that will self-cure without intervention. The structural constraint is not a lack of effort: it is the absence of a prioritization layer that distinguishes between accounts that need a call, accounts that need an SMS, and accounts that need no contact at all.

Indian NBFC NPA recovery rates average 51-58% on unsecured portfolios without AI intervention, while AI pre-delinquency and propensity-sequenced treatment pushes this to 74-82% (iTuring NBFC Collections Deployment Data 2024-25, 18 NBFC deployments). On a Rs. 1,000 crore unsecured book with 5% gross NPA, the difference between 54% and 78% recovery translates to Rs. 12 crore in reduced provisioning annually. Every 30-day delay in collections intervention reduces recovery probability by 5-8 percentage points on unsecured NBFC portfolios, and the cumulative effect across a portfolio is significant (RBI NBFC Supervisory Data and iTuring Portfolio Analytics 2024-25). This is where NBFC NPA provisioning meets AI recovery improvement: the provisioning line item moves because the recovery rate moved, and the recovery rate moved because the intervention happened earlier.

Why Recovery Rate Is Determined at 30 DPD, Not 90 DPD, and What Changes That Outcome

- Account prioritization determines right-party contact rate, and right-party contact rate is the single strongest predictor of recovery on unsecured NBFC portfolios. Without a propensity model, collections teams work accounts in descending order of outstanding balance. A Rs. 50,000 personal loan with a 90% probability of self-cure gets the same treatment intensity as a Rs. 50,000 loan with a 15% probability. The result is a 26-31% right-party contact rate: agents spend most of their time reaching borrowers who either do not need contact or will not respond to it. AI-driven account scoring at the 1-30 DPD stage changes this by routing only high-risk, high-propensity accounts to live agents, which is exactly the kind of early intervention approach that drives NPA recovery rate improvement at Indian NBFCs.

- Channel and timing selection directly affect cost per contact, which in turn determines how many accounts the collections operation can cover within its budget. An NBFC running 200 agents on manual dialing spends Rs. 120-180 per recovery attempt. When a predictive model identifies that a specific borrower segment responds to WhatsApp reminders at 10 AM on the second day past due, the cost per contact drops to Rs. 15-30 for that segment. This is not a theoretical efficiency: AI-driven debt collection platforms in India are already operationalizing this channel logic across multiple NBFCs. The freed-up agent capacity then gets redirected to accounts that genuinely require human intervention.

- Self-cure identification removes accounts from the contact queue entirely, which reduces total contact volume without reducing recovery. On a typical unsecured NBFC portfolio, 15-25% of accounts that enter 1-30 DPD will cure without any collections intervention. Without a self-cure model, every one of those accounts receives calls, SMS messages, and potentially field visits. An NBFC with 50,000 accounts in early delinquency is making 7,500 to 12,500 unnecessary contacts per month. Removing those accounts from the queue does not just save cost: it prevents borrower fatigue and complaint escalation on accounts that were never at risk.

- Compliance cost reduction is the variable that collections leaders most often underestimate. Manual collections operations generate regulatory risk through inconsistent call scripts, untracked contact frequency, and poorly documented borrower interactions. An NBFC that faces an RBI supervisory review on collections practices needs to demonstrate that contact frequency, timing, and language comply with Fair Practices Code guidelines. RBI-compliant AI collections platforms now generate audit trails automatically, reducing the compliance overhead that otherwise requires dedicated quality assurance teams. The cost reduction here is not just in QA headcount: it is in the avoided cost of regulatory findings that can restrict an NBFC’s lending activity.

NBFC NPA Recovery Rate Before and After AI Deployment: What the Data Shows

The evidence base for NPA recovery rate improvement through AI at Indian NBFCs comes from 18 production deployments across consumer lending, personal loan, and microfinance portfolios. The NBFCs that achieved the highest recovery gains shared two characteristics: they had digitized borrower contact data, and they deployed propensity models at the 1-15 DPD stage rather than waiting for accounts to reach 30 DPD. The primary variable was not the sophistication of the model but the timing of intervention. The comparison below shows the specific metrics across deployment cohorts.

| Metric | Before AI | With iTuring |

| Cost per recovery | Rs. 120-180 (manual) | Rs. 45-74 (AI-first) |

| Right-party contact rate | 26-31% | 44-51% |

| 30-60 DPD roll rate | 22-28% | 14-19% |

| Self-cure identification | Not available | Removes 15-25% of queue |

| Model retraining | Quarterly or ad hoc | Continuous — automated |

Results vary by portfolio composition, starting baseline, and data maturity: figures above reflect median outcomes across NBFC deployments.

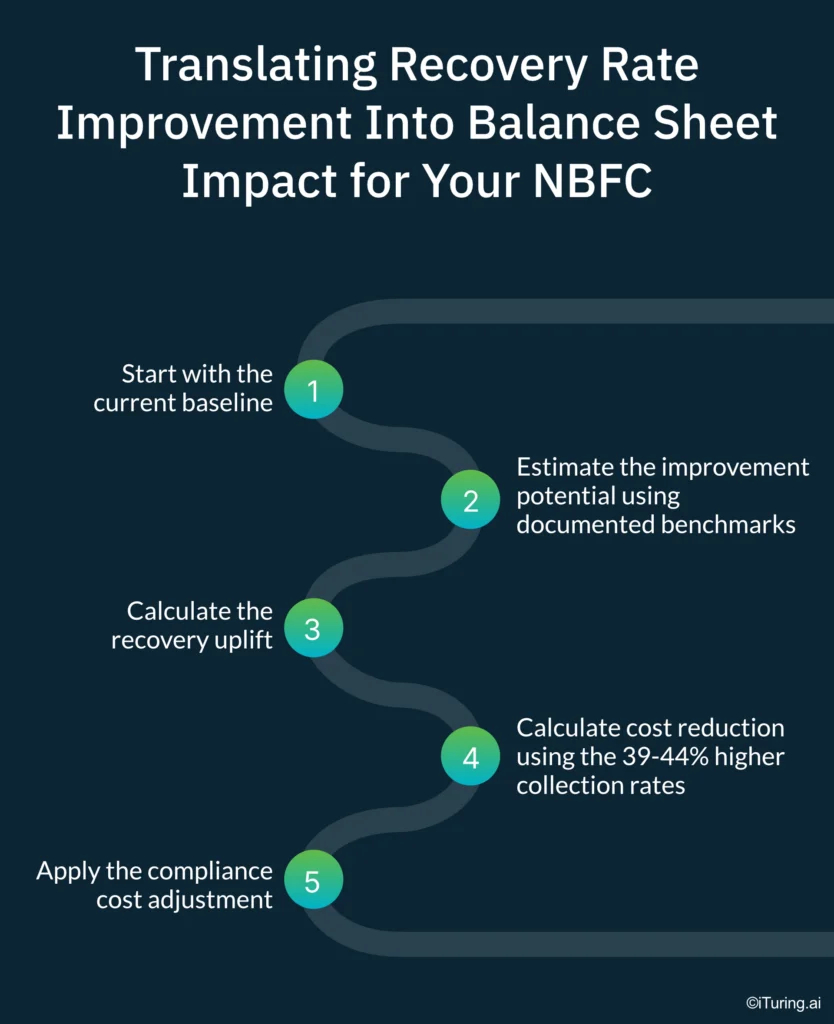

Translating Recovery Rate Improvement Into Balance Sheet Impact for Your NBFC

Building the ROI case for AI collections requires five concrete steps that connect recovery rate data to balance sheet outcomes. This framework is designed for the Chief Risk Officer who needs to present a defensible number to the CFO and the board.

- Start with the current baseline. If the NBFC’s existing NPA recovery rate sits at 51% using manual reactive collections on the existing NPA portfolio, that is the anchor for every calculation that follows. This baseline reflects the reality of NPA recovery rate improvement potential at Indian NBFCs: the gap between where most institutions sit and where AI deployment data shows they can reach. Do not use an optimistic internal estimate. Use the actual recovery percentage from the last four quarters, averaged.

- Estimate the improvement potential using documented benchmarks. The target range of 74-82% NPA recovery rate comes from deployments where propensity-driven treatment was applied at the 1-30 DPD stage. For NBFCs with less mature data infrastructure, a conservative target of 68-72% is more realistic for the first 12 months. The NBFC collections AI recovery rate benchmark from India suggests that data maturity is the primary constraint on how quickly an institution can reach the upper range.

- Calculate the recovery uplift using the documented 116% increase in overall collections recovery rate from a leading NBFC deployment. On a Rs. 500 crore NPA book with a 51% baseline, a 116% improvement in recovery rate translates to significant additional recovery. Even a conservative 50% of this documented uplift produces a material provisioning reduction.

- Calculate cost reduction using the 39-44% higher collection rates across all delinquency buckets versus reactive strategy. This figure accounts for reduced agent hours, lower cost per contact through digital channels, and elimination of unnecessary contacts on self-curing accounts. For an NBFC spending Rs. 15 crore annually on collections operations, a 40% efficiency gain frees Rs. 6 crore in operational budget.

- Apply the compliance cost adjustment. NBFCs that face frequent RBI supervisory scrutiny on collections practices carry a hidden cost in legal fees, QA staff, and remediation projects. Bajaj Finance’s AI-led roadmap to FY30 illustrates how the largest NBFCs are already factoring AI collections into their long-term compliance and growth strategy.

The calculation only works if the baseline is honest: start with 51% recovery rate from manual reactive collections on the existing NPA portfolio as the anchor, not an aspirational figure.

From 54% to 82% NPA Recovery: What a Propensity-Driven Collections Deployment Produces

A leading Indian NBFC with a diversified unsecured lending portfolio faced a persistent 51-58% NPA recovery rate despite maintaining a 300-agent collections operation and spending Rs. 18 crore annually on collections infrastructure. The institution deployed iTuring Collections Agent with propensity-based account scoring, automated channel selection, and self-cure identification across its full delinquency book, with the first models in production within 14 days of data integration.

Results after deployment:

- 116% increase in overall collections recovery rate at a leading NBFC deployment

- 39-44% higher collection rates across all delinquency buckets versus reactive strategy

- 20% increase in collections recovery rate

- 43% reduction in cost per recovery

NPA Recovery Rate Is a Board Metric But it is Determined by Operations Decisions Made 90 Days Earlier

The recovery rate that appears in board reporting and RBI submissions is a lagging indicator of decisions made at the 1-30 DPD stage: account prioritization logic, channel selection, contact timing, and self-cure exclusion. The provisioning benefit of moving from 54% to 78% recovery is quantifiable on any NBFC balance sheet within two quarters. The operational prerequisite is a collections system that scores accounts before they reach 30 DPD, not after they have already rolled into NPA classification.

iTuring’s collections platform has documented NPA recovery rate data from 18 NBFC deployments: test the model against your own portfolio before any licence decision.

What This Data Means for Your Next Board Presentation

The pattern across 18 NBFC deployments is consistent: recovery rate is a function of intervention timing, not collections headcount. NBFCs that score and prioritize accounts at the 1-15 DPD stage, route low-risk accounts to digital channels, and exclude self-curing accounts from the contact queue recover 74-82% on unsecured portfolios. NBFCs that wait until 30 or 60 DPD and work accounts in balance-descending order recover 51-58%.

The Indian collections industry is converging around this operational model, and the NBFC sector’s growth trajectory is accelerating as AI changes unit economics in both lending and collections. The provisioning impact is immediate. The CRAR impact follows within two quarters. The RBI supervisory benefit compounds over time.