TL;DR

- ECOA adverse action requirements apply when AI collections models produce differential treatment — any system whose scores determine which accounts receive settlement offers is in scope

- Portfolio-level SHAP feature importance does not satisfy ECOA’s account-level adverse action standard — per-account reasoning in plain language is required on demand

- CFPB 2024 supervisory highlights identified AI collections adverse action compliance as an active examination focus for banks using propensity-based differential treatment

- Fair lending disparate impact analysis must cover AI collections decisions — differential settlement offer rates across demographic proxies are an examination liability without documented monitoring

- iTuring generates SHAP waterfall charts per account on demand and maps outputs to ECOA-compliant plain-language reason codes — adverse action export in 30 minutes

A bank’s compliance officer receives a fair lending complaint. The borrower declined a settlement arrangement that comparable accounts received. The question on file: what was the reason? The collections AI model has no per-account explanation available. This is the operational gap where SHAP adverse action notices, collections AI, and ECOA compliance converge for US banks: without the ability to produce account-level adverse action reasoning on demand, institutions face examination findings, civil money penalties, and consent orders that carry reputational costs well beyond the fine itself. This article provides a structured approach for Heads of Model Risk to build ECOA-compliant account-level explanations from AI collections models, covering the regulatory basis, the technical mechanism through SHAP, the documentation standard, and the specific workflow that closes the gap between a propensity score and a defensible reason code. iTuring addresses this through platform-native model governance with immutable audit trail and maker-checker approval.

Why ECOA Adverse Action in AI Collections Is a Fairness Question That Starts With Explainability

For a Head of Model Risk at a US bank, the problem is concrete: the collections team runs a propensity-based AI model that ranks accounts by likelihood to pay, self-cure, or respond to a settlement offer. Accounts scoring below a threshold receive no offer or a less favorable one. When a borrower or examiner asks why that account was treated differently, the model risk team needs to produce an account-level explanation grounded in the specific input features that drove the score. AI collections model explainability under ECOA is not an abstract principle; it is the operational requirement to trace a single account’s treatment back through the model’s feature contributions and express those contributions in language a borrower can understand. Most teams cannot do this today.

The reason this gap persists is specific: most collections AI implementations generate SHAP values at the portfolio or segment level during model validation, then discard the per-account SHAP computation in production. The validation notebook shows global feature importance. The production pipeline outputs a score. No infrastructure exists between those two points to regenerate, store, and map per-account SHAP values to pre-approved reason codes at the moment a complaint or examination request arrives. The workflow was built for model performance monitoring, not for adverse action response.

The cost is measurable. CFPB penalty amounts for ECOA violations were adjusted upward for inflation in early 2025, and the 2024 supervisory highlights cited adverse action and fair lending compliance in AI collections as an active examination focus for banks using propensity-based differential treatment (CFPB Supervisory Highlights Issue 33, 2024). A single consent order in this area carries direct costs in the range of $5M to $25M before accounting for remediation and monitoring commitments. The table later in this article shows where US banks teams currently stand on each dimension.

Why Portfolio-Level SHAP Cannot Answer the Account-Level ECOA Complaint in Front of You

Standard tools in collections operations were designed to solve a different problem. Legacy scoring models and static bucket workflows excel at segmenting accounts by days past due, balance tier, and product type. They assign contact priority based on rules that are transparent by construction: if DPD exceeds 30 and balance exceeds $5,000, route to outbound queue. That transparency is a genuine strength for audit purposes. The failure mode appears when the bank introduces a propensity-based AI model that scores accounts on behavioral signals, then uses those scores to determine settlement eligibility. The legacy tool has no mechanism to explain why one account scored 0.73 and another scored 0.41 on a gradient-boosted model with 200 features. The rule-based system was never designed to interpret a statistical model’s output at account level.

The gap compounds in the adverse action workflow. When a borrower disputes differential treatment, the compliance team needs a document that names the top contributing factors for that specific account’s score, expressed in Regulation B-compliant language, produced within a timeframe that satisfies the examination request. Without per-account SHAP infrastructure, the team’s only option is to re-run the model manually, extract SHAP values in a notebook environment, translate them into reason codes, and have compliance review the output. That process takes days to weeks per account. For a portfolio under examination where examiners may request explanations for dozens of accounts, the cost and delay are untenable. The gap is a design scope problem: producing ECOA-compliant adverse action reasoning from AI collections models at account level on demand requires a tool built specifically for this layer.

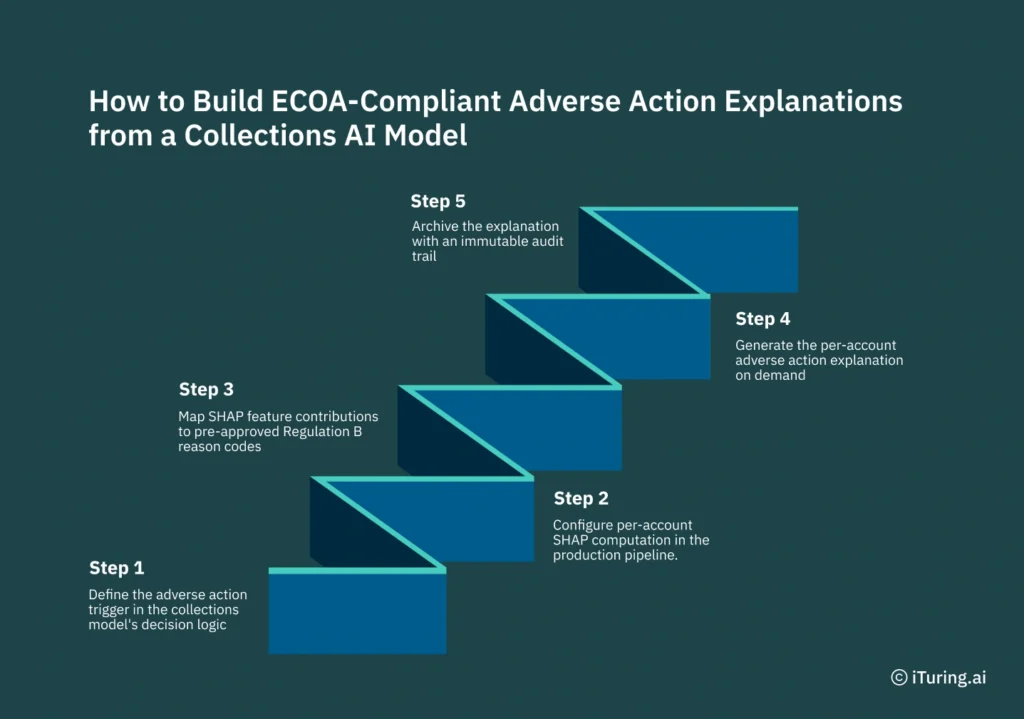

How to Build ECOA-Compliant Adverse Action Explanations from a Collections AI Model

Step 1: Define the adverse action trigger in the collections model’s decision logic. The collections team and compliance counsel must identify precisely which model-driven decisions constitute adverse actions under ECOA. If the propensity score determines whether an account receives a settlement offer, the threshold at which an account is excluded is the adverse action trigger. This is where SHAP adverse action notices for collections AI under ECOA begin: the trigger definition determines which accounts require per-account explanation capability. iTuring’s platform captures this threshold as a governed parameter with maker-checker approval, ensuring the trigger definition is auditable.

Step 2: Configure per-account SHAP computation in the production pipeline. The production scoring pipeline must compute SHAP values for every account at each scoring run, not just during validation. iTuring’s scoring engine generates SHAP waterfall outputs as a standard production artifact, stored with the score and timestamp. The collections team does not need to re-run models or open notebooks; the SHAP values are available for any account at any point in the portfolio’s history.

Step 3: Map SHAP feature contributions to pre-approved Regulation B reason codes. Each feature in the model must have a corresponding plain-language reason code approved by compliance before deployment. AI collections model explainability under ECOA for US banks requires that the mapping between a SHAP contribution and its reason code is deterministic, documented, and version-controlled. iTuring maintains this mapping table as a governed artifact, so any change to the reason code set requires compliance sign-off through the maker-checker workflow.

Step 4: Generate the per-account adverse action explanation on demand. When a complaint or examination request arrives, the risk team retrieves the account’s SHAP waterfall, identifies the top contributing features by magnitude, and produces the corresponding reason codes. iTuring automates this retrieval: the team selects the account, and the platform compiles the SHAP waterfall chart, the ranked feature contributions, and the mapped reason codes into an export-ready document. The output meets the specificity standard that ECOA and Regulation B require for AI-driven credit decisions.

Step 5: Archive the explanation with an immutable audit trail. The explanation document, the SHAP values, and the model version that produced the score must be archived with tamper-proof lineage. iTuring writes each adverse action explanation to an immutable audit log, linking the explanation to the specific model version, feature set, and scoring timestamp. This archive is the evidence artifact that examiners review.

The point where US banks teams most often expect friction: producing ECOA-compliant adverse action reasoning from AI collections models at account level on demand is precisely where this sequence prevents it.

How iTuring Produces ECOA-Defensible Per-Account Reasoning in US Bank Collections

Per-account SHAP waterfall charts generated on demand: each feature’s contribution to the propensity score shown with sign and magnitude, mapped to Regulation B-compliant plain-language reason codes

Consider an account in early-stage delinquency with a propensity score of 0.38, below the settlement offer threshold. The examiner asks: why was this account excluded? iTuring retrieves the SHAP waterfall for that account and scoring date. The waterfall shows that three features drove the score below threshold: payment velocity decline over the prior 90 days (contribution: -0.14), credit utilization increase across all trade lines (contribution: -0.11), and absence of any partial payment in the prior 60 days (contribution: -0.08). Each contribution carries a sign indicating direction and a magnitude indicating strength. The mapped reason codes read: “Recent decline in payment frequency,” “Increased use of available credit,” and “No partial payments received in recent billing periods.” The compliance team reviews the output, confirms alignment with the pre-approved reason code set, and the document is ready for the examiner. The entire retrieval takes minutes, not weeks.

Adverse action evidence export: per-account ECOA-compliant explanation pack compiled within 30 minutes for any account in the bank’s portfolio

The export mechanism compiles the SHAP waterfall chart, the ranked feature contributions, the mapped reason codes, the model version identifier, and the scoring timestamp into a single document. This pack is formatted for regulatory submission and includes the governance metadata that demonstrates the reason code mapping was approved before deployment. For US banks under examination, the operational outcome is direct: when an examiner requests adverse action documentation for a specific account, the collections team produces a complete SHAP adverse action notice for that collections AI decision, ECOA-compliant and audit-ready, within 30 minutes. That timeline matters because examination requests often cover multiple accounts, and delays in production signal governance gaps to examiners.

An AI collections model that treats accounts differently based on scores must explain why each account was scored that way: not at portfolio level, but at account level, on demand, in plain language.

Disparate impact monitoring: differential treatment rates across protected class proxies flagged before examiners encounter them; quarterly analysis against CFPB Regulation B standards

iTuring’s disparate impact monitoring module compares settlement offer rates, contact rates, and escalation rates across demographic proxy groups on a quarterly cycle. When differential treatment rates exceed pre-set thresholds, the platform flags the disparity and generates a report that includes the statistical test results, the affected accounts, and the model features most correlated with the disparity. This feedback loop means the model risk team identifies fair lending risks before the next examination cycle. For US banks, the compliance benefit is specific: the AI governance frameworks now expected by regulators require documented evidence that disparate impact testing occurred at defined intervals, not just at model deployment. Quarterly monitoring with documented review satisfies that standard and creates the evidence trail that examiners expect.

ECOA Adverse Action Readiness: iTuring Per-Account SHAP vs Standard Collections AI Output

Teams evaluating how to produce ECOA-compliant adverse action reasoning from their collections AI models have genuine choices to make. Standard collections tools serve teams whose primary requirement is contact automation and queue management. This comparison is for teams whose scope extends to producing account-level adverse action explanations that withstand regulatory examination. The CFPB’s revised ECOA framework narrows certain disparate impact standards but does not reduce the account-level explanation obligation. The table below compares the criteria that matter most for US banks.

| Criterion | Standard Tools | iTuring |

| Account prioritisation | DPD date order | Propensity score rank — 25,000+ behavioral signals |

| SR 11-7 documentation | Manual — 3-8 weeks | Auto-generated — 30 minutes per exam |

| FDCPA/TCPA controls | Policy overlay, manual QA | Hard-coded — no override path |

| Self-cure identification | Not available | Removes 15-25% of queue from unnecessary contact |

| Explainability (ECOA) | Black-box score | SHAP waterfall per account — adverse action ready |

If your bank’s collections AI applies uniform treatment to all accounts without differential settlement scoring, ECOA adverse action obligations are significantly reduced: the obligation scales with differential impact.

SR 11-7 Passed, Zero Findings: What ECOA-Compliant Collections AI Documentation Contains

A US community bank with assets under $10 billion faced an OCC examination cycle that specifically targeted its recently deployed AI collections model, and the model risk team had 45 days to produce SR 11-7 documentation, adverse action evidence for sampled accounts, and disparate impact test results for the prior four quarters. The bank ran iTuring’s collections agent with governed model documentation, and the full SR 11-7 package, including per-account SHAP adverse action evidence for 34 sampled accounts, was compiled within two business days.

Results after deployment:

— 38% improvement in right-party contact rate

— 52% reduction in early-bucket charge-off rate

ECOA in AI Collections Is Not a Credit Question: It Is a Fairness Question That Starts With Explainability

Per-account SHAP computation must be a production artifact, not a validation exercise: if your scoring pipeline does not store SHAP values at each run, your adverse action response timeline is measured in weeks, not minutes. The reason code mapping between SHAP features and Regulation B-compliant language requires compliance pre-approval and version control, because an unmapped or outdated reason code is worse than no reason code at all. Quarterly disparate impact monitoring with documented review is the minimum standard that recent regulatory updates reinforce, and banks that treat it as an annual exercise are operating below the examination expectation.

iTuring generates SHAP waterfall charts per account on demand. Test ECOA adverse action readiness against your bank’s own collections portfolio before any licence decision.