TL;DR

- AI early warning identifies NBFC borrowers at risk of default 90-120 days before the first missed payment – using behavioral signals that lagging indicators like bureau scores cannot capture

- Recovery probability for accounts contacted at pre-delinquency stage is 2.3x higher than accounts first activated at 30 DPD

- iTuring achieves 83% prediction accuracy at 120 days using 25,000+ signals across transaction, behavioral, and bureau data for NBFC portfolios

- Pre-delinquency AI models are in scope for RBI’s 2024 MRM framework – model inventory, annual validation, and board reporting are required from deployment day one

- Deployment from data connection to live scoring: 3-4 weeks with pre-built Finacle, FinnOne, TCS BaNCS, and Flexcube connectors

Monday at an NBFC’s collections centre. The 30-60 DPD report loads: 3,800 accounts. A second report – the AI early warning feed – shows 2,100 of those accounts flagged their stress signals 100 days earlier. Before a single payment was missed. This gap between pre-delinquency prediction and reactive collections activation is where Indian NBFCs lose recoverable principal every quarter. When at-risk borrowers are not identified 90-120 days before their first missed payment, the collections team inherits accounts where avoidance behaviour has already hardened, contact rates have dropped, and the cost per rupee recovered has doubled. This article provides a deployment-ready guide for heads of collections at NBFCs: the behavioral signals that predict default at 120 days, the step-by-step process for putting an AI early warning system into production, and the RBI compliance requirements that apply from day one. iTuring addresses this through closed-loop propensity scoring with autonomous agent outreach.

The 14 Behavioral Signals Your NBFC Portfolio Showed in August Before the November Default

For a head of collections at an NBFC, the operational reality of pre-delinquency detection is not an abstract analytics concept. It is the difference between a Monday morning queue of 3,800 accounts already in default and a feed of 2,100 accounts showing stress patterns three months before any EMI is missed. NBFC AI default prediction at 120 days means the collections team sees declining transaction frequency, NACH mandate rejections, and salary credit reductions while the account is still technically current. The team acts on signals, not on damage already done.

The reason this capability remains absent from most NBFC operations is specific: core banking systems export DPD flags and bureau scores, but they do not surface behavioral velocity data. Transaction frequency trends, savings balance trajectories, and concurrent EMI load changes sit in raw transaction tables that no standard collections workflow consumes. The data exists. The extraction and scoring pipeline does not.

The cost of this gap is measurable. NBFCs deploying AI early warning intervention achieve 39-44% higher collection rates across delinquency buckets compared to reactive contact strategies (iTuring AI Collections Deployment Data 2024-25 – 12 NBFC deployments). With NBFC balance sheets projected to reach Rs. 93 trillion by FY28, even a single-digit improvement in early-stage recovery rates represents tens of crores in preserved principal annually. The table later in this article shows where NBFC teams currently stand on each dimension.

Why Activating Collections at 30 DPD Means Entering the Recovery Conversation 120 Days Late

Standard rule-based diallers and static bucket workflows were designed for a legitimate purpose: organizing outbound contact for accounts that have already missed payments. They do this well. The dialler sequences accounts by DPD bucket, assigns call priority, and tracks agent productivity. The failure mode is not in execution but in scope. These tools activate only after a payment is missed, which means the earliest possible intervention is 30 days after the borrower’s financial stress began manifesting in behavioral data. For NBFCs where AI is already reshaping credit risk and fraud detection, the absence of pre-delinquency scoring creates a blind spot that no amount of post-default calling efficiency can compensate for.

The gap compounds through cost per contact escalation. Once an account enters 30 DPD, the borrower’s willingness to engage drops measurably. Contact rates fall from above 60% for current accounts to below 35% at 30 DPD, and below 20% at 60 DPD. Each successive bucket requires more attempts, more agent time, and more expensive channels to reach the same borrower. Without propensity data on which accounts will self-cure and which require intervention, the dialler treats every account in the bucket identically, wasting capacity on accounts that would have paid anyway while under-resourcing the accounts accelerating toward write-off. The gap is a design scope problem – identifying at-risk NBFC borrowers 90-120 days before their first missed payment requires a tool built specifically for this layer.

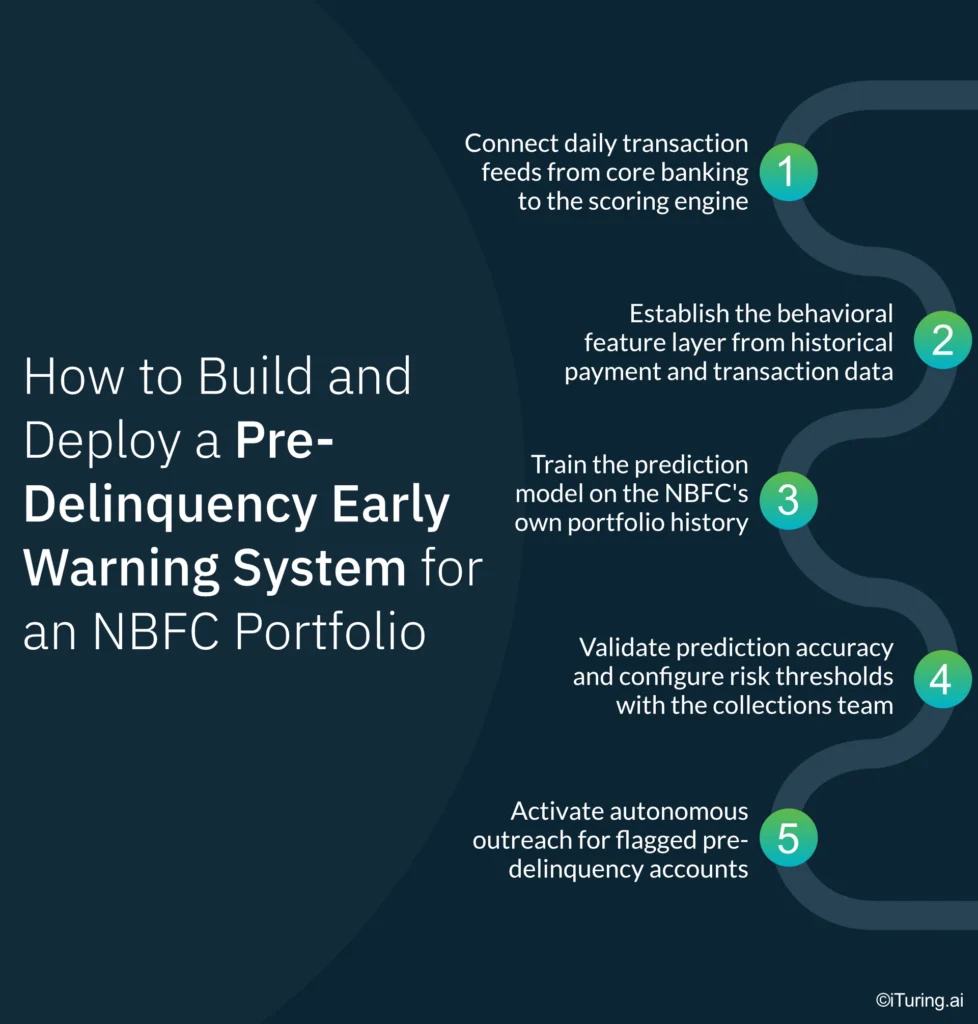

How to Build and Deploy a Pre-Delinquency Early Warning System for an NBFC Portfolio

Step 1: Connect daily transaction feeds from core banking to the scoring engine. The pre-delinquency prediction system for Indian NBFCs requires daily extracts of transaction-level data: credits, debits, NACH mandate status, balance snapshots, and EMI payment confirmations. iTuring’s pre-built connectors for Finacle, FinnOne, TCS BaNCS, and Flexcube pull this data through scheduled API calls without custom integration work. The NBFC’s IT team configures access credentials and field mappings; the connector handles schema normalization.

Step 2: Establish the behavioral feature layer from historical payment and transaction data. iTuring’s Data Accelerator generates 50,000+ pre-built financial features from the raw transaction feeds: 30-day transaction frequency trends, salary credit variability, savings balance velocity, and concurrent EMI obligation changes. The NBFC’s risk or collections team reviews the feature set through a visual interface, confirming which signals are available in their specific core banking export. This step is where pre-delinquency AI early warning capability is built or constrained by data availability.

Step 3: Train the prediction model on the NBFC’s own portfolio history. The model trains on 18-24 months of the NBFC’s historical data, learning which behavioral patterns preceded actual defaults in that specific portfolio. NBFC AI default prediction accuracy at 120 days depends entirely on the institution’s own data, not on generic industry models. iTuring AutoML+ tests multiple model architectures and selects the champion based on prediction accuracy for that portfolio’s risk profile.

Step 4: Validate prediction accuracy and configure risk thresholds with the collections team. The collections team reviews model outputs against known outcomes: which accounts the model would have flagged 120 days before actual default, and which it would have missed. Threshold configuration determines the sensitivity of the early warning feed. A lower threshold catches more at-risk accounts but increases false positives; a higher threshold produces a more precise but smaller intervention queue.

Step 5: Activate autonomous outreach for flagged pre-delinquency accounts. iTuring Collections Agent triggers proactive contact for accounts crossing the risk threshold: channel selection, message tone, and timing are all determined by the borrower’s behavioral profile. The collections team receives a daily dashboard showing flagged accounts, outreach status, and borrower responses. Outcomes feed back into the model for continuous retraining.

The point where NBFC teams most often expect friction – identifying at-risk borrowers before the first missed payment – is precisely where this sequence prevents it.

How iTuring Reads Pre-Delinquency Stress Before the First Payment Is Missed

Pre-delinquency stress scoring using 25,000+ behavioral signals

Transaction frequency changes, NACH mandate failures, salary credit patterns, updated daily for every active account, not just DPD accounts

Consider a borrower with a Rs. 15,000 monthly personal loan EMI. Over three weeks, their savings account balance drops 40% below its 90-day average, two small NACH mandates for utility payments bounce, and their salary credit arrives eight days later than the previous six-month pattern. No EMI has been missed. The bureau score has not moved. iTuring’s scoring engine reads these signals in combination, assigns a stress probability score of 0.78, and routes the account into the pre-delinquency intervention queue. The collections team sees this account on Tuesday morning alongside 340 others showing similar patterns – each with a specific stress signal breakdown and recommended contact timing.

Pre-delinquency treatment routing

Distinct message, channel, and tone for accounts showing stress signals versus healthy payment trajectory, triggered before any payment is missed

The routing mechanism separates accounts into treatment paths based on stress score severity and signal composition. An account showing salary delay but stable balance receives a different message – a payment reminder with a one-tap link – than an account showing both balance decline and concurrent EMI increases, which receives a proactive restructuring offer. Pre-delinquency prediction for Indian NBFCs requires this signal-specific routing because a generic “your EMI is due” message performs no better than the standard dialler for accounts under genuine financial stress. The operational outcome: AI-driven early delinquency prediction enables lenders to reduce defaults through intervention calibrated to the borrower’s actual situation, not their bucket position.

The borrower who missed a payment in November showed 14 behavioral stress signals in August. The NBFC that saw those signals in August has a fundamentally different conversation than the one that calls in November.

Closed-loop prediction improvement

Early intervention outcomes feed back into the prediction model, improving 120-day accuracy progressively with each deployment cycle

Every outreach action and borrower response becomes training data for the next model iteration. When a borrower flagged at stress score 0.72 receives a proactive payment link and pays on time, the model learns that this signal combination at this score level responds to low-intensity intervention. When a borrower at 0.85 ignores three contact attempts and defaults at 45 DPD, the model recalibrates its threshold recommendations. This closed loop is not optional for RBI compliance: the 2024 MRM framework requires NBFCs to document model performance drift and retraining methodology. Predictive risk analytics in banking now demands continuous validation rather than point-in-time assessments. iTuring Model Risk generates the required documentation automatically with each retraining cycle, including performance metrics, data drift reports, and validation summaries ready for board attestation.

120-Day Early Warning vs 30-DPD Activation: Recovery Rate and Cost Comparison

Teams evaluating pre-delinquency AI early warning systems for their NBFC portfolios face a genuine decision between upgrading existing tools and deploying a purpose-built prediction layer. Standard rule-based diallers and manual contact strategies serve teams whose primary need is outbound call automation for accounts already in default. This comparison is for teams whose scope includes identifying at-risk borrowers 90-120 days before the first missed payment, where the operational requirements extend well beyond contact sequencing. The table below compares the criteria that matter most for NBFCs.

| Criterion | Standard Tools | iTuring |

| Account prioritisation | DPD bucket order | Daily propensity score – 25,000+ signals |

| Self-cure identification | Not available | Withholds self-cure accounts before queue loads |

| Contact timing | Fixed campaign schedule | Per-account optimal timing from behavioral signals |

| Model retraining | Quarterly or ad hoc | Continuous – outcomes retrain model automatically |

| Audit trail (RBI) | Contact logs only | Immutable per-account decision log – examination-ready |

If your NBFC lacks 18+ months of transaction-level behavioral data from core banking, pre-delinquency AI will underperform standard DPD-based scoring until the training dataset is established.

83% Prediction Accuracy Before a Single Payment Is Missed: A Deployment Example

A housing finance company with a Rs. 21 billion portfolio was losing recoverable accounts to late-stage collections activation: by the time the team contacted borrowers at 30 DPD, contact rates had fallen below 30% and restructuring acceptance was declining quarter over quarter. The company deployed iTuring’s pre-delinquency scoring engine with daily transaction feeds from its core banking platform, with the full system operational within four weeks using pre-built connectors.

Results after deployment:

- 83% prediction accuracy for accounts entering 30+ DPD within 120 days

- Deployed in 4 weeks with pre-built core banking connectors

The 120-Day Window: How NBFCs That Act Before Default Recover Accounts Others Wait to Write Off

The 120-day prediction window is not a theoretical improvement over 30-DPD activation: it is a structural change in which accounts are recoverable and which are not. Every week of delay after behavioral stress signals appear reduces the probability of successful intervention, and the compounding effect across a portfolio of thousands of accounts translates directly into write-off volume. The microfinance sector’s recent portfolio recovery demonstrates that early identification of stress, combined with calibrated outreach, produces measurably different outcomes than waiting for delinquency to appear in DPD reports.

iTuring’s pre-delinquency engine trains on your NBFC’s own historical payment and transaction data – test prediction accuracy against your portfolio before any licence decision. Request a portfolio assessment to see how 120-day prediction accuracy performs against your current collections activation benchmarks.