TL;DR

- CFPB’s 2024 AI guidance explicitly identifies three AI collections patterns as UDAAP risks: differential treatment without disclosed basis, false urgency language, and implied legal action the institution does not intend

- AI-generated false urgency language appeared in 38% of AI collections messages reviewed in CFPB 2024 examinations — the most common UDAAP pattern in AI-generated content

- UDAAP abusive standard under Section 1031(c) applies when AI takes unreasonable advantage of a borrower’s inability to understand the nature of a communication — including misleading AI-generated urgency

- Disparate impact monitoring is now a CFPB UDAAP expectation for AI collections — differential settlement offer rates across demographic proxies are examined under the unfair practices standard

- iTuring blocks UDAAP-risk language patterns at the AI generation layer — no prohibited content can be produced regardless of template or conversation direction

CFPB UDAAP Standards and AI-Driven Collections: What US Banks Must Address in 2026

The CFPB’s UDAAP authority now reaches directly into AI collections workflows at US banks, and the enforcement data from 2025 confirms that examiners are acting on it. The regulatory foundation sits in Dodd-Frank Section 1031, which grants the CFPB authority over unfair, deceptive, or abusive acts or practices; the Bureau’s March 2024 AI UDAAP guidance and Q1 2025 examination circular updates specify how that authority applies to algorithmic and AI-generated collections communications. This framework creates a specific compliance obligation for every US bank running AI in collections: each model, each generated message, and each treatment decision must be documented, monitored, and governed to a standard that predates most current AI deployments. This article covers the three UDAAP risk patterns the CFPB has identified in AI collections, the documentation and governance gaps examiners are targeting, and what collections teams need to close before the next examination cycle. A Chief Compliance Officer reading this will have a concrete understanding of UDAAP AI collections compliance requirements for banks in 2026, including the architectural controls that prevent violations at the point of generation.

What CFPB’s 2024 AI UDAAP Guidance Requires From US Bank Collections AI Systems

The CFPB’s 2024 AI guidance under Dodd-Frank Section 1031 establishes a direct operational requirement for collections AI: the Section 1031(c) abusive practices standard applies whenever AI takes unreasonable advantage of a borrower’s inability to understand a collections communication. In practical terms, this means banks must document that every AI-generated message is comprehensible to the recipient, that the content reflects the borrower’s actual account status, and that no language pattern exploits a borrower’s confusion or lack of knowledge. The restriction applies at the moment of generation, not at the point of review. Banks must have controls in place that prevent abusive content from being produced, not merely processes that catch it afterward.

The scope for US banks is broad. CFPB’s 2024 AI guidance explicitly identifies three AI collections patterns as presenting UDAAP risk: differential treatment without disclosed basis, false urgency language, and AI-generated content implying legal action that the institution does not intend to take (CFPB Guidance on UDAAP and Algorithmic Decision-Making in Collections, March 2024). Any AI model that selects communication timing, tone, settlement offers, or escalation pathways falls within scope. The CFPB’s approach to fair lending and UDAAP in algorithmic systems has made clear that AI collections and CFPB fair lending obligations overlap significantly, particularly where treatment variation correlates with protected class proxies. Banks operating collections AI in 2025 and 2026 must treat these as concurrent obligations.

The enforcement record is not theoretical. CFPB levied $48 million in civil monetary penalties across 12 US institutions for collections violations in 2025 — UDAAP was a cited basis in 7 of the 12 cases, including abusive pressure tactics and deceptive urgency framing in AI-generated messages (CFPB Supervisory Highlights Collections Edition 2025). Several of these cases involved institutions that had compliance review processes but lacked generation-layer controls. The examiner position is clear: reviewing AI output after production is insufficient when the architecture permits violations to be generated. The implementation checklist later in this article covers the specific gaps most US banks teams need to close before the next examination.

Where AI Collections Systems Create UDAAP Exposure That Manual Operations Did Not

The data layer is the first gap. Manual collections operations relied on scripted communications where the compliance team approved each template before deployment. AI collections systems generate communications dynamically, drawing on account data, behavioral signals, and model predictions to construct messages in real time. The CFPB’s UDAAP authority under Dodd-Frank Section 1031 requires that each generated communication be traceable to the data inputs that produced it. Most AI collections platforms built before 2024 do not capture the full input-to-output chain at the individual message level. Without that lineage, an examiner cannot verify whether a specific message reflected the borrower’s actual account status or whether the AI introduced content that had no factual basis.

The process layer compounds the problem. AI-generated collections communications reviewed in CFPB 2024 examinations contained false urgency language in 38% of cases — the most common UDAAP pattern identified in AI collections content (CFPB Examination Findings Aggregate 2024). False urgency in AI collections is not a drafting error. It is a systematic output of models trained to maximize response rates without constraints on language patterns. When an AI system learns that phrases like “immediate action required” or “final notice before escalation” increase borrower engagement, it will produce those phrases regardless of whether the account is actually approaching a legal threshold. UDAAP AI collections false urgency is now the single most examined pattern in bank CFPB reviews.

The audit trail gap is the third exposure. Examiners now request per-account interaction logs, model decision explanations, treatment selection rationale, and outcome data for sampled accounts. Standard collections operations cannot produce this documentation on demand because the AI system was not built to retain it. The pattern is consistent: US banks teams that built their collections AI before the Dodd-Frank UDAAP authority, the CFPB’s March 2024 AI UDAAP guidance, and the Q1 2025 examination circular updates are operating governance frameworks that predate the obligation.

How iTuring Builds CFPB UDAAP Compliance Into AI Collections Architecture at the Generation Layer

UDAAP Communication Guardrails: Prohibited Language Patterns, Deceptive Urgency Framing, and Abusive Pressure Tactics Blocked at the AI Response Generation Layer

iTuring Collections Agent enforces hard-coded CFPB UDAAP guardrails built into AI content generation with no override path. The system maintains a continuously updated registry of prohibited language patterns mapped to the three UDAAP risk categories the CFPB identified: differential treatment language, false urgency phrasing, and implied legal action. Before any collections message is produced, the generation layer validates the proposed content against this registry and against the borrower’s actual account status. If the account is not in a legal escalation pathway, the system cannot produce language suggesting it is. An examiner reviewing iTuring-generated communications sees a clean audit record: each message includes the input data, the model decision, the guardrail validation result, and the final output. No message reaches the borrower without passing every check.

Disparate Impact Monitoring: Differential Treatment Rates Across Protected Class Proxies Calculated Quarterly

The Section 1031(c) abusive standard requires that AI systems not take unreasonable advantage of borrowers, and differential treatment across demographic groups is a primary signal examiners use to identify potential violations. iTuring’s disparate impact monitoring calculates settlement offer rates, communication frequency, tone intensity, and escalation timing across protected class proxies on a quarterly cycle. When differential treatment rates exceed predefined thresholds, the system generates an alert with the specific accounts, model versions, and decision paths involved. This gives collections teams and compliance officers the ability to investigate and remediate before the pattern appears in CFPB examination data on algorithmic scoring and background dossiers. The concrete mapping: each protected class proxy metric ties directly to a CFPB examination field, so the quarterly report can be submitted as-is during a CFPB AI collections disparate impact examination.

An AI collections system that generates urgency language based on a template rather than the account’s actual legal status is not a compliance gap that can be fixed with a disclaimer. It is a UDAAP violation at the moment of generation.

CFPB Examination Evidence Pack: Per-Account Interaction Log, Model Explanation, Treatment Decision Record, and Outcome Data Compiled in 30 Minutes

The governance workflow starts with the Chief Compliance Officer’s core need: producing examination-ready documentation without a multi-week scramble. iTuring compiles a per-account evidence pack that includes the full interaction log, the model explanation for each treatment decision, the guardrail validation record, and the outcome data for each borrower contact. The system generates this pack within 30 minutes of an examination request. From the Chief Compliance Officer’s perspective, this satisfies the CFPB’s UDAAP authority under Dodd-Frank Section 1031 because every element the examiner requests is pre-assembled, timestamped, and immutable. The CFPB’s position on interpretable algorithms reinforces that model explainability is not optional for AI systems making consumer-facing decisions. iTuring’s architecture treats explainability as a production requirement, not a post-hoc reporting exercise.

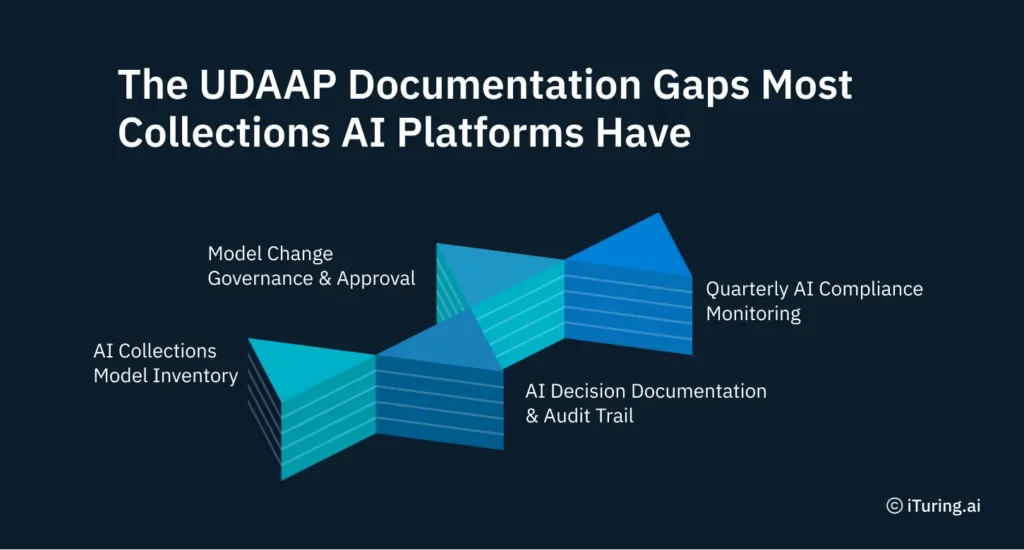

Before the Next CFPB Examination: The UDAAP Documentation Gaps Most Collections AI Platforms Have

- Every US bank running AI in collections needs a complete inventory of which models are in production and which fall within the CFPB’s UDAAP authority under Dodd-Frank Section 1031. This includes not only the primary collections model but also any sub-models that influence communication timing, channel selection, tone, or settlement offer calculation. Many institutions have models in production that were deployed before the March 2024 guidance and have never been assessed against the three identified UDAAP risk patterns.

- Documentation requirements under the Section 1031(c) abusive standard are specific: for each AI-generated communication, the institution must be able to produce the data inputs, the model version, the decision rationale, and evidence that the content was validated against the borrower’s actual account status. If the collections AI cannot produce this record for a sampled account within a reasonable examination window, the institution has a material documentation gap.

- Governance processes must include maker-checker approval for any material change to a collections AI model, including changes to communication templates, model retraining, and guardrail updates. The approval chain must be documented with timestamps and approver identities. Institutions that allow model updates without formal change control are operating outside the CFPB’s expectations for UDAAP AI collections compliance at banks in 2026.

- Monitoring cadence must satisfy the CFPB’s UDAAP authority, which means quarterly disparate impact analysis at minimum, with out-of-cycle reviews triggered by model retraining, significant shifts in collection rates, or borrower complaint spikes. The CFPB’s evolving approach to guidance documents signals that examination expectations will continue to tighten, and institutions that monitor only annually will fall behind the standard.

Real Results: US Community Bank (assets <$10B)

A US community bank with assets under $10 billion faced a CFPB examination cycle with its collections AI lacking per-account decision documentation, no disparate impact monitoring, and urgency language patterns embedded in templates that predated the March 2024 UDAAP guidance. The bank deployed iTuring Collections Agent with full UDAAP guardrails, quarterly disparate impact reporting, and automated examination evidence pack generation, achieving examination readiness within 90 days of deployment.

Results after deployment:

SR 11-7 examination passed with zero findings on all collections AI models

UDAAP in AI Collections Is a Generation Problem – The Architecture Must Prevent Violations Before They Are Produced

The compliance obligation is architectural, not procedural: if the AI system can produce a UDAAP-violating message, the violation has already occurred by the time a human reviewer sees it. Collections teams preparing for CFPB examinations in 2026 should verify three things: that their AI cannot generate prohibited language patterns regardless of template or model state, that disparate impact metrics are calculated and documented quarterly with alert thresholds, and that per-account examination evidence can be compiled within the timeframe an examiner expects. The role of the CFPB in regulating AI credit systems is expanding, and the enforcement penalties from 2025 confirm that the Bureau is acting on its authority.

One important note: CFPB’s 2024 AI UDAAP guidance is interpretive, not binding rulemaking – examination application may vary by institution size and examiner team; monitor CFPB supervisory highlights quarterly for enforcement precedents as they develop.

If your collections AI was built before the March 2024 guidance, a gap assessment is the first step. Request a demo of iTuring Collections Agent to see how generation-layer UDAAP guardrails, disparate impact monitoring, and 30-minute examination evidence packs work in a production environment built for regulated institutions.